- Joined

- Aug 19, 2017

- Messages

- 2,758 (1.01/day)

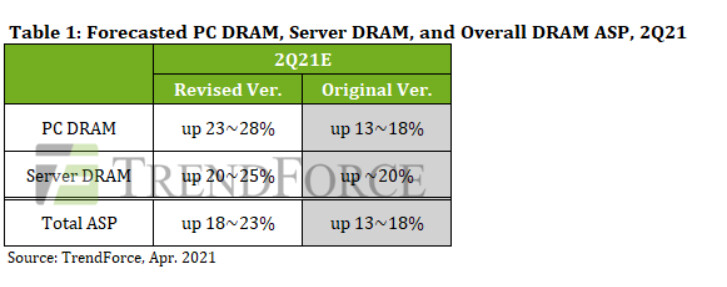

TrendForce's investigations find that DRAM suppliers and major PC OEMs are currently participating in the critical period of negotiating with each other over contract prices for 2Q21. Although these negotiations have yet to be finalized, the ASP of mainstream DDR4 1G*8 2666 Mbps modules has already increased by nearly 25% QoQ as of now, according to data on ongoing transactions. This represents a higher price hike than TrendForce's prior forecast of "nearly 20%". On the other hand, prices are likewise rising across various DRAM product categories in 2Q21, including DDR3/4 specialty DRAM, mobile DRAM, graphics DRAM, and in particular server DRAM, which is highly related to PC DRAM and is therefore also undergoing a higher price hike than previously expected. TrendForce is therefore revising up its forecast of overall DRAM price hike for 2Q21 from 13-18% QoQ to 18-23% QoQ instead. However, the actual increase in prices of various DRAM product categories will depend on the production capacities allocated to the respective products by DRAM suppliers.

PC DRAM prices are now expected to undergo a 23-28% QoQ growth in 2Q21 due to the increased production of notebook computers

PC DRAM contract prices are rising by a higher margin than previously expected for 2Q21 primarily because major PC OEMs are now aggressively expanding their production targets. Furthermore, as second quarters are generally peak seasons for notebook production, PC ODMs are now estimated to increase their quarterly production of notebook computers by about 7.9% QoQ in 2Q21. Finally, with regards to the COVID-19 pandemic, vaccination rates remain relatively low across the globe, meaning WFH and distance education are likely to persist and create continued demand for notebook computers, thereby further expanding the hike in PC DRAM prices.

DRAM Suppliers will enjoy increased bargaining power in price negotiations as server DRAM prices are expected to increase by 20-25% QoQ in 2Q21

Apart from the issue of short DRAM supply, server DRAM procurement in 2Q21 has benefitted from the positive turn in the view of enterprises toward IT investments as well as the stronger-than-expected demand related to cloud migration. There was already a supply gap in 1Q21, and these developments will further drive up demand in 2Q21. Hence, difficulty has increased for buyers and suppliers in reaching an agreement on price. Suppliers are in a more advantageous position in contract negotiations since the DRAM market is an oligopoly. Therefore, compared to the previous forecast of nearly 20%, TrendForce is now expecting server DRAM contract prices to increase by 20-25% QoQ in 2Q21.

View at TechPowerUp Main Site

PC DRAM prices are now expected to undergo a 23-28% QoQ growth in 2Q21 due to the increased production of notebook computers

PC DRAM contract prices are rising by a higher margin than previously expected for 2Q21 primarily because major PC OEMs are now aggressively expanding their production targets. Furthermore, as second quarters are generally peak seasons for notebook production, PC ODMs are now estimated to increase their quarterly production of notebook computers by about 7.9% QoQ in 2Q21. Finally, with regards to the COVID-19 pandemic, vaccination rates remain relatively low across the globe, meaning WFH and distance education are likely to persist and create continued demand for notebook computers, thereby further expanding the hike in PC DRAM prices.

DRAM Suppliers will enjoy increased bargaining power in price negotiations as server DRAM prices are expected to increase by 20-25% QoQ in 2Q21

Apart from the issue of short DRAM supply, server DRAM procurement in 2Q21 has benefitted from the positive turn in the view of enterprises toward IT investments as well as the stronger-than-expected demand related to cloud migration. There was already a supply gap in 1Q21, and these developments will further drive up demand in 2Q21. Hence, difficulty has increased for buyers and suppliers in reaching an agreement on price. Suppliers are in a more advantageous position in contract negotiations since the DRAM market is an oligopoly. Therefore, compared to the previous forecast of nearly 20%, TrendForce is now expecting server DRAM contract prices to increase by 20-25% QoQ in 2Q21.

View at TechPowerUp Main Site