TheLostSwede

News Editor

- Joined

- Nov 11, 2004

- Messages

- 17,769 (2.42/day)

- Location

- Sweden

| System Name | Overlord Mk MLI |

|---|---|

| Processor | AMD Ryzen 7 7800X3D |

| Motherboard | Gigabyte X670E Aorus Master |

| Cooling | Noctua NH-D15 SE with offsets |

| Memory | 32GB Team T-Create Expert DDR5 6000 MHz @ CL30-34-34-68 |

| Video Card(s) | Gainward GeForce RTX 4080 Phantom GS |

| Storage | 1TB Solidigm P44 Pro, 2 TB Corsair MP600 Pro, 2TB Kingston KC3000 |

| Display(s) | Acer XV272K LVbmiipruzx 4K@160Hz |

| Case | Fractal Design Torrent Compact |

| Audio Device(s) | Corsair Virtuoso SE |

| Power Supply | be quiet! Pure Power 12 M 850 W |

| Mouse | Logitech G502 Lightspeed |

| Keyboard | Corsair K70 Max |

| Software | Windows 10 Pro |

| Benchmark Scores | https://valid.x86.fr/yfsd9w |

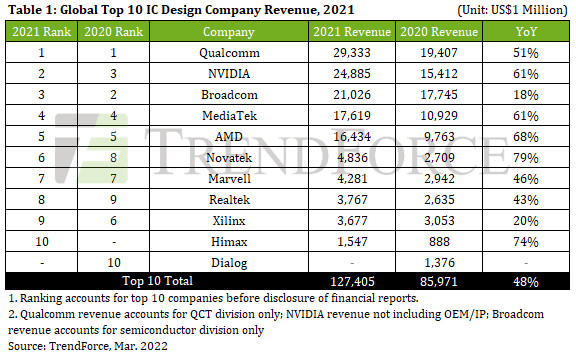

According to TrendForce research, due to vigorous stocking of various terminal applications causing a shortage of wafers in 2021, the global IC industry was severely undersupplied. This, coupled with spiking chip prices, boosted 2021 revenue of the global top ten IC design companies to US$127.4 billion, or 48% YoY. TrendForce further indicates three major disparities from the 2020 ranking. First, NVIDIA surpassed Broadcom to take the second position. Second, Taiwanese companies Novatek and Realtek rose to sixth and eighth place, respectively. Originally ranked tenth, Dialog was replaced at this position by Himax after Dialog was acquired by IDM giant Renesas.

Qualcomm continues its reign as number one in the world, primarily due to 51% and 63% growth YoY in sales of mobile phone SoC (System on Chip) and IoT chips, respectively. The addition of diversified development in its RF and automotive chip businesses were key to a 51% increase in revenue. NVIDIA implemented an integration of software and hardware, demonstrating its ambitions in creating a "comprehensive computing platform." Driven by annual growth of gaming graphics card and data center revenue at 64% and 59%, respectively, NVIDIA successfully climbed to second place. Broadcom benefited from the stable sales performance of network chips, broadband communication chips, and storage and bridging chips, with revenue growing 18% YoY. AMD's computer and graphics revenue grew by 45% YoY due to strong sales of the Ryzen CPU and Radeon GPU and rising average selling price. Coupled with accelerating demand from cloud companies, the annual revenue of AMD's enterprise, embedded, and semi-customized divisions increased by 113%, driving annual growth of total revenue to 68%.

In terms of Taiwanese firms, MediaTek's strategy of focusing on mobile phone SoC has produced miraculous results. Benefiting from an increase in 5G penetration, sales performance of MediaTek's mobile phone product portfolio surged by 93% and the company has committed to increasing the proportion of high-end product portfolios, resulting in 61% annual revenue growth. Novatek's two major product lines of SoC and display driver IC have both grown significantly. Due to improved product specifications, increased shipments, and beneficial pricing gains, revenue grew by 79% YoY, highest among the top ten. Realtek has been driven by strong demand for Netcom and commercial notebook products, while the performance of audio and Bluetooth chips remains quite stable, conferring an annual revenue growth of 43%. Himax joins the top ten ranking for the first time in 2021. Due to significant annual revenue growth in large-sized and medium/small-sized driver IC of 65% and 87%, respectively, and the successful introduction of driver IC into automotive panels, total revenue exceeded US$1.5 billion, or 74% YoY.

Looking forward to 2022, after AMD completes the acquisition of Xilinx, other players will fill out the rankings. In the broader picture, intensifying demand for high-specification products such as high-performance computing, Netcom, high-speed transmission, servers, automotive, and industrial applications will create good business opportunities for IC design companies and drive overall revenue growth. However, terminal system manufacturers face the correction of component mismatch issues. In addition, growing foundry costs, intensifying geopolitical conflicts, and rising inflation will all be detrimental to global economic growth and may impact an already weakened consumer electronics market. These are the challenges IC design companies face in 2022 and by what means can product sales momentum be maintained within existing production capacity, R&D efficacy strengthened, and chip specifications upgraded, will become the primary focus of development in 2022.

View at TechPowerUp Main Site | Source

Qualcomm continues its reign as number one in the world, primarily due to 51% and 63% growth YoY in sales of mobile phone SoC (System on Chip) and IoT chips, respectively. The addition of diversified development in its RF and automotive chip businesses were key to a 51% increase in revenue. NVIDIA implemented an integration of software and hardware, demonstrating its ambitions in creating a "comprehensive computing platform." Driven by annual growth of gaming graphics card and data center revenue at 64% and 59%, respectively, NVIDIA successfully climbed to second place. Broadcom benefited from the stable sales performance of network chips, broadband communication chips, and storage and bridging chips, with revenue growing 18% YoY. AMD's computer and graphics revenue grew by 45% YoY due to strong sales of the Ryzen CPU and Radeon GPU and rising average selling price. Coupled with accelerating demand from cloud companies, the annual revenue of AMD's enterprise, embedded, and semi-customized divisions increased by 113%, driving annual growth of total revenue to 68%.

In terms of Taiwanese firms, MediaTek's strategy of focusing on mobile phone SoC has produced miraculous results. Benefiting from an increase in 5G penetration, sales performance of MediaTek's mobile phone product portfolio surged by 93% and the company has committed to increasing the proportion of high-end product portfolios, resulting in 61% annual revenue growth. Novatek's two major product lines of SoC and display driver IC have both grown significantly. Due to improved product specifications, increased shipments, and beneficial pricing gains, revenue grew by 79% YoY, highest among the top ten. Realtek has been driven by strong demand for Netcom and commercial notebook products, while the performance of audio and Bluetooth chips remains quite stable, conferring an annual revenue growth of 43%. Himax joins the top ten ranking for the first time in 2021. Due to significant annual revenue growth in large-sized and medium/small-sized driver IC of 65% and 87%, respectively, and the successful introduction of driver IC into automotive panels, total revenue exceeded US$1.5 billion, or 74% YoY.

Looking forward to 2022, after AMD completes the acquisition of Xilinx, other players will fill out the rankings. In the broader picture, intensifying demand for high-specification products such as high-performance computing, Netcom, high-speed transmission, servers, automotive, and industrial applications will create good business opportunities for IC design companies and drive overall revenue growth. However, terminal system manufacturers face the correction of component mismatch issues. In addition, growing foundry costs, intensifying geopolitical conflicts, and rising inflation will all be detrimental to global economic growth and may impact an already weakened consumer electronics market. These are the challenges IC design companies face in 2022 and by what means can product sales momentum be maintained within existing production capacity, R&D efficacy strengthened, and chip specifications upgraded, will become the primary focus of development in 2022.

View at TechPowerUp Main Site | Source