TheLostSwede

News Editor

- Joined

- Nov 11, 2004

- Messages

- 18,140 (2.45/day)

- Location

- Sweden

| System Name | Overlord Mk MLI |

|---|---|

| Processor | AMD Ryzen 7 7800X3D |

| Motherboard | Gigabyte X670E Aorus Master |

| Cooling | Noctua NH-D15 SE with offsets |

| Memory | 32GB Team T-Create Expert DDR5 6000 MHz @ CL30-34-34-68 |

| Video Card(s) | Gainward GeForce RTX 4080 Phantom GS |

| Storage | 1TB Solidigm P44 Pro, 2 TB Corsair MP600 Pro, 2TB Kingston KC3000 |

| Display(s) | Acer XV272K LVbmiipruzx 4K@160Hz |

| Case | Fractal Design Torrent Compact |

| Audio Device(s) | Corsair Virtuoso SE |

| Power Supply | be quiet! Pure Power 12 M 850 W |

| Mouse | Logitech G502 Lightspeed |

| Keyboard | Corsair K70 Max |

| Software | Windows 10 Pro |

| Benchmark Scores | https://valid.x86.fr/yfsd9w |

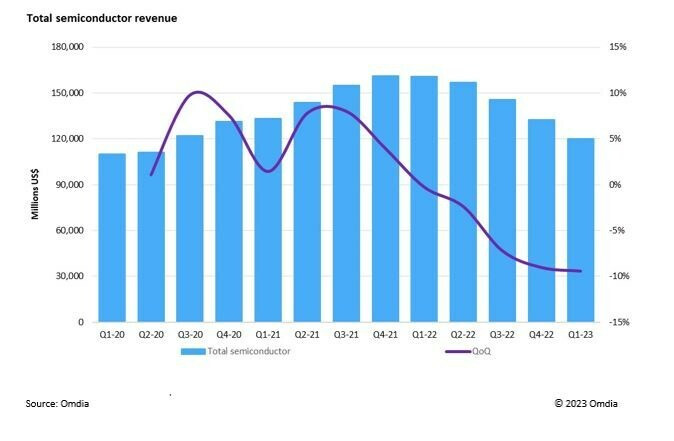

New research from Omdia reveals that the semiconductor market declined in revenue for a fifth straight quarter in the first quarter of 2023. This is the longest recorded period of decline since Omdia began tracking the market in 2002. Revenue in 1Q23 settled at $120.5B, down 9% from 4Q22. The semiconductor market is cyclical, and this prolonged decline follows the upsurge as the market grew to record revenues in each quarter between 4Q20 through 4Q21 following increased demand from the global pandemic.

The memory and MPU market are major areas of the semiconductor market that are contributing to the decline. The MPU market in 1Q23 was $13.1B, just 65% of its size in 1Q22 when it was $20B. The memory market fared worse, with 1Q23 coming in at $19.3B, just 44% of the market in 1Q22 when it was $43.6B. The combined MPU and memory markets declined 19% in 1Q23, dragging the market down to the 9% quarter-over-quarter (QoQ) decline.

Commenting on the latest Omdia analyst, Cliff Leimbach, Senior Analyst said: "The semiconductor market is plagued by a lack of demand that has continued for multiple quarters and resulted in declining ASPs for many components. However, there is demand thanks to generative AI. NVIDIA has seen strong revenue growth as they lead in this space, reversing the performance of most semiconductor companies to begin 2023, but other semiconductor companies have yet to take advantage of this space in a similar way."

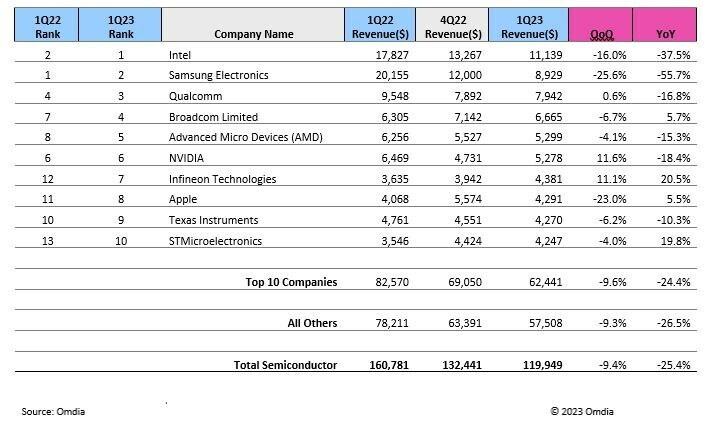

The decline of the memory market over the last three quarters has rearranged the market share rankings. One year ago, three of the top five semiconductor companies by revenue were memory companies, Samsung, SK Hynix, and Micron. Only Samsung remains in the top ten rankings. The last time both SK Hynix and Micron were not in the top ten rankings was in 2008 illustrating the struggles faced by memory-focused semiconductor companies.

NVIDIA released their financial results after publication of the CLT report, and surpassed estimates on strength of the company's generative AI chips due to strong demand.

Infineon moved into the top ten this year following an 11% increase QoQ due to its strength in the automotive sector.

View at TechPowerUp Main Site | Source

The memory and MPU market are major areas of the semiconductor market that are contributing to the decline. The MPU market in 1Q23 was $13.1B, just 65% of its size in 1Q22 when it was $20B. The memory market fared worse, with 1Q23 coming in at $19.3B, just 44% of the market in 1Q22 when it was $43.6B. The combined MPU and memory markets declined 19% in 1Q23, dragging the market down to the 9% quarter-over-quarter (QoQ) decline.

Commenting on the latest Omdia analyst, Cliff Leimbach, Senior Analyst said: "The semiconductor market is plagued by a lack of demand that has continued for multiple quarters and resulted in declining ASPs for many components. However, there is demand thanks to generative AI. NVIDIA has seen strong revenue growth as they lead in this space, reversing the performance of most semiconductor companies to begin 2023, but other semiconductor companies have yet to take advantage of this space in a similar way."

The decline of the memory market over the last three quarters has rearranged the market share rankings. One year ago, three of the top five semiconductor companies by revenue were memory companies, Samsung, SK Hynix, and Micron. Only Samsung remains in the top ten rankings. The last time both SK Hynix and Micron were not in the top ten rankings was in 2008 illustrating the struggles faced by memory-focused semiconductor companies.

NVIDIA released their financial results after publication of the CLT report, and surpassed estimates on strength of the company's generative AI chips due to strong demand.

Infineon moved into the top ten this year following an 11% increase QoQ due to its strength in the automotive sector.

View at TechPowerUp Main Site | Source