TheLostSwede

News Editor

- Joined

- Nov 11, 2004

- Messages

- 17,802 (2.42/day)

- Location

- Sweden

| System Name | Overlord Mk MLI |

|---|---|

| Processor | AMD Ryzen 7 7800X3D |

| Motherboard | Gigabyte X670E Aorus Master |

| Cooling | Noctua NH-D15 SE with offsets |

| Memory | 32GB Team T-Create Expert DDR5 6000 MHz @ CL30-34-34-68 |

| Video Card(s) | Gainward GeForce RTX 4080 Phantom GS |

| Storage | 1TB Solidigm P44 Pro, 2 TB Corsair MP600 Pro, 2TB Kingston KC3000 |

| Display(s) | Acer XV272K LVbmiipruzx 4K@160Hz |

| Case | Fractal Design Torrent Compact |

| Audio Device(s) | Corsair Virtuoso SE |

| Power Supply | be quiet! Pure Power 12 M 850 W |

| Mouse | Logitech G502 Lightspeed |

| Keyboard | Corsair K70 Max |

| Software | Windows 10 Pro |

| Benchmark Scores | https://valid.x86.fr/yfsd9w |

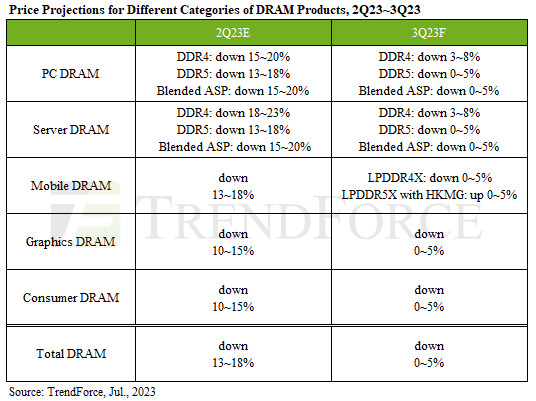

TrendForce reports that continued production cuts by DRAM suppliers have led to a gradual quarterly decrease in overall DRAM supply. Seasonal demand, on the other hand, is helping to mitigate inventory pressure on suppliers. TrendForce projects that the third quarter will see the ASP for DRAM converging towards a 0~5% decline. Despite suppliers' concerted efforts, inventory levels persistently remain high, keeping prices low. While production cutbacks may help to curtail quarterly price declines, a tangible recovery in prices may not be seen until 2024.

PC DRAM: The benefits of consolidated production cuts on DDR4 by the top three suppliers are expected to become evident in the third quarter. Furthermore, inventory pressure on suppliers has been partially alleviated due to aggressive purchasing by several OEMs at low prices during 2Q23. Evaluating average price trends for PC DRAM products in 3Q23 reveals that DDR4 will continue to remain in a state of persistent oversupply, leading to an expected quarterly price drop of 3~8%. DDR5 prices—influenced by suppliers' efforts to maintain prices and unmet buyer demand—are projected to see a 0-5% quarterly decline. The overall ASP of PC DRAM is projected to experience a QoQ decline of 0~5% in the third quarter.

Server DRAM: Buyer inventories remain high and the transition to new platforms has fallen short of expectations. Despite the recent investment focus by CSPs on AI server equipment, which is accelerating the procurement of high-capacity server DRAM such as DDR5 128G and HBM, there hasn't been a significant reduction in server DRAM inventories. The price decline for DDR4 and DDR5 stands at approximately 3~8% and 0~5% respectively, signaling a persistently weak pricing trend for server DRAM products. Consequently, average server DRAM prices are forecasted to decline by about 0~5% in 3Q23.

Mobile DRAM: Even though smartphone demand was weak in 1H23, the traditional peak season and concurrent production cuts by suppliers are expected to drive up demand for mobile DRAM. However, these measures offer limited assistance in being able to substantially reduce suppliers' inventory levels. Successive price declines over past quarters have now reached baseline prices for suppliers, prompting Korean firms to lead a hike in mobile DRAM prices. But due to the prevailing oversupply, a standoff has ensued between buyers and sellers. The ASP of mobile DRAM is predicted to fall by 0~5% in 3Q23, although sporadic price increases may occur due to strategic moves made by suppliers.

Graphics DRAM: The NVIDIA RTX 40 series, along with the traditional peak season, is anticipated to stimulate a significant upswing in demand for graphics DRAM—particularly GDDR6 16Gb—during the third quarter. However, given that buyers accumulated stock ahead of time in the second quarter and now hold substantial inventory, suppliers may find themselves unable to increase prices in a market that remains in a state of oversupply. Therefore, the market price of mainstream GDDR6 16Gb is projected to see a quarterly drop of 0~5% in the third quarter, mirroring an approximate 0~5% decline in ASP for graphics DRAM.

Consumer DRAM: The market is currently witnessing a sluggish transactional pace. SK hynix plans to expand the supply of DDR3 and DDR4 4Gb at its Wuxi fab, gradually increasing production capacity. Simultaneously, Winbond has transitioned into the mass production stage, with an increase in wafer input expected each quarter. As a result, the consumer DRAM market continues to grapple with oversupply. Nevertheless, suppliers are progressively cutting back production, the benefits which are expected to materialize in the third quarter. Given the substantial operating losses incurred by these suppliers, these factors should curtail the decline in ASP of consumer DRAM to 0~5% in 3Q23.

View at TechPowerUp Main Site | Source

PC DRAM: The benefits of consolidated production cuts on DDR4 by the top three suppliers are expected to become evident in the third quarter. Furthermore, inventory pressure on suppliers has been partially alleviated due to aggressive purchasing by several OEMs at low prices during 2Q23. Evaluating average price trends for PC DRAM products in 3Q23 reveals that DDR4 will continue to remain in a state of persistent oversupply, leading to an expected quarterly price drop of 3~8%. DDR5 prices—influenced by suppliers' efforts to maintain prices and unmet buyer demand—are projected to see a 0-5% quarterly decline. The overall ASP of PC DRAM is projected to experience a QoQ decline of 0~5% in the third quarter.

Server DRAM: Buyer inventories remain high and the transition to new platforms has fallen short of expectations. Despite the recent investment focus by CSPs on AI server equipment, which is accelerating the procurement of high-capacity server DRAM such as DDR5 128G and HBM, there hasn't been a significant reduction in server DRAM inventories. The price decline for DDR4 and DDR5 stands at approximately 3~8% and 0~5% respectively, signaling a persistently weak pricing trend for server DRAM products. Consequently, average server DRAM prices are forecasted to decline by about 0~5% in 3Q23.

Mobile DRAM: Even though smartphone demand was weak in 1H23, the traditional peak season and concurrent production cuts by suppliers are expected to drive up demand for mobile DRAM. However, these measures offer limited assistance in being able to substantially reduce suppliers' inventory levels. Successive price declines over past quarters have now reached baseline prices for suppliers, prompting Korean firms to lead a hike in mobile DRAM prices. But due to the prevailing oversupply, a standoff has ensued between buyers and sellers. The ASP of mobile DRAM is predicted to fall by 0~5% in 3Q23, although sporadic price increases may occur due to strategic moves made by suppliers.

Graphics DRAM: The NVIDIA RTX 40 series, along with the traditional peak season, is anticipated to stimulate a significant upswing in demand for graphics DRAM—particularly GDDR6 16Gb—during the third quarter. However, given that buyers accumulated stock ahead of time in the second quarter and now hold substantial inventory, suppliers may find themselves unable to increase prices in a market that remains in a state of oversupply. Therefore, the market price of mainstream GDDR6 16Gb is projected to see a quarterly drop of 0~5% in the third quarter, mirroring an approximate 0~5% decline in ASP for graphics DRAM.

Consumer DRAM: The market is currently witnessing a sluggish transactional pace. SK hynix plans to expand the supply of DDR3 and DDR4 4Gb at its Wuxi fab, gradually increasing production capacity. Simultaneously, Winbond has transitioned into the mass production stage, with an increase in wafer input expected each quarter. As a result, the consumer DRAM market continues to grapple with oversupply. Nevertheless, suppliers are progressively cutting back production, the benefits which are expected to materialize in the third quarter. Given the substantial operating losses incurred by these suppliers, these factors should curtail the decline in ASP of consumer DRAM to 0~5% in 3Q23.

View at TechPowerUp Main Site | Source