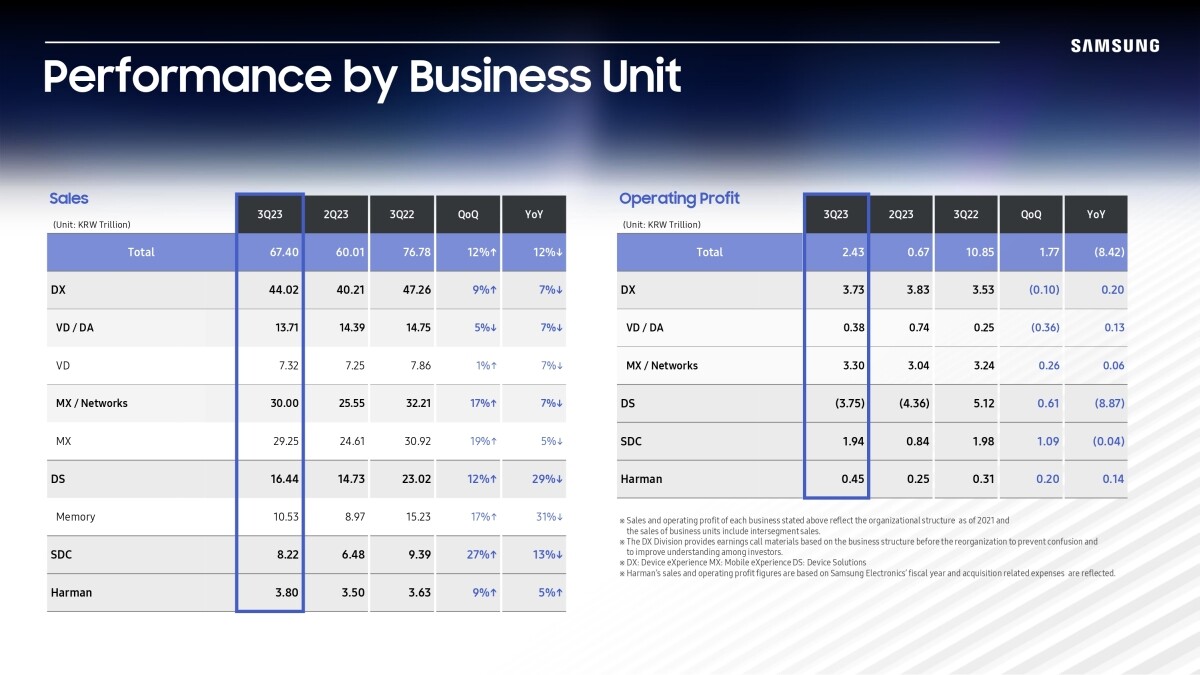

Samsung Electronics today reported financial results for the third quarter ended September 30, 2023. Total consolidated revenue was KRW 67.40 trillion, a 12% increase from the previous quarter, mainly due to new smartphone releases and higher sales of premium display products. Operating profit rose sequentially to KRW 2.43 trillion based on strong sales of flagship models in mobile and strong demand for displays, as losses at the Device Solutions (DS) Division narrowed.

The Memory Business reduced losses sequentially as sales of high valued-added products and average selling prices somewhat increased. Earnings in system semiconductors were impacted by a delay in demand recovery for major applications, but the Foundry Business posted a new quarterly high for new backlog from design wins. The mobile panel business reported a significant increase in earnings on the back of new flagship model releases by major customers, while the large panel business narrowed losses in the quarter. The Device eXperience (DX) Division achieved solid results due to robust sales of premium smartphones and TVs. Revenue at the Networks Business declined in major overseas markets as mobile operators scaled back investments.

Harman posted a quarterly record in operating profit, led by higher sales of car audio products amid an overall increase in orders from automotive customers and also consumer audio products such as portable speakers.

In the fourth quarter, the DS Division will focus on sales of high value-added products such as High Bandwidth Memory (HBM) while also strengthening its technological leadership. Both the DX Division and Samsung Display Corporation (SDC) will seek to maintain solid profitability by focusing on premium markets.

The Memory Business plans to expand sales of HBM3 products and will address growing demand for new interfaces while increasing the portion of advanced nodes. System semiconductors are expected to post improved results on the back of new products for mobile customers.

SDC expects to maintain strong performance in the mobile panel business, driven by robust demand for premium OLED panels for smartphones. The large panel business will expand QD-OLED sales, led by year-end seasonal demand.

The DX Division will strive to maintain solid profitability by reinforcing strategies for flagship smartphones and expanding sales of premium tablets and wearable products. For TVs, the Company expects solid seasonal demand for high value-added models. The Networks Business will seek to secure new orders in overseas markets, while the Digital Appliances Business will focus on sales of premium products and strengthening the product mix.

Harman will seek to post another robust quarter by expanding sales of audio products during end-year seasonality as well as addressing the continuing demand for automotive products.

In 2024, while macroeconomic uncertainties are likely to persist, memory market conditions are expected to recover. The DS Division will seek to expand sales of advanced node products and plans to meet demand for high-performance, high-bandwidth products by increasing sales of HBM3 and HBM3E with the industry-leading HBM production capacity in the industry. For the Foundry Business, the second generation 3-nanometer (nm) Gate-All-Around (GAA) process will start mass production and operations will begin at its new factory in Taylor, Texas. Furthermore, in the Advanced Package business, production will begin, based on the multiple orders it has received from domestic and overseas HPC customers, including orders for the Company's turnkey service that combines logic, HBM and 2.5D advanced packaging technologies.

For SDC, the mobile panel business plans to meet increasing demand for new applications, while the large panel business will improve profitability by adding new products and enhancing yields.

The DX Division will focus on the premium market by increasing sales of flagship smartphone models and innovative TV products. The Company plans to expand the application of AI, provide tailored hyper-connected experiences via SmartThings and secure technologies in new areas such as XR. The Networks Business will aim to increase revenue by seeking business opportunities overseas and reinforcing technology leadership in core 5G chips and virtualized Radio Access Network (vRAN) solutions.

The Digital Appliances Business plans to strengthen the leadership in premium segments with global launches of appliances featuring AI technology. The Company plans to continue advancing the connectivity experience between SmartThings-based digital appliances and other devices.

Harman is expected to secure orders in new areas including automotive displays and will address demand for high-growth products such as home audio equipment.

In the third quarter, Samsung Electronics' capital expenditure reached KRW 11.4 trillion, including KRW 10.2 trillion spent in the Device Solutions (DS) Division and KRW 0.7 trillion in Samsung Display Corporation (SDC). The cumulative total for the January-September period is KRW 36.7 trillion, with KRW 33.4 trillion allocated to the DS Division and KRW 1.6 trillion to SDC.

The full-year capital expenditure for 2023 is expected at approximately KRW 53.7 trillion, including KRW 47.5 trillion allocated to the DS Division and KRW 3.1 trillion to SDC.

Spending on memory is expected to be concentrated in Pyeongtaek, which includes completing the P3 infrastructure and progressing the P4 framework for mid- to long-term supply. The Company remains committed to investing in new technologies, such as securing industry-leading HBM production capacity. Foundry investments are expected to increase from last year, centering on production capacity expansion in Pyeongtaek for the EUV process as well as for infrastructure investment in Taylor. For SDC, investments will mainly focus on expanding capacity for flexible displays and OLED products for IT applications.

Foundry Achieves Record Backlog From Design Wins; Memory Demand To Recover in 2024

The DS Division posted KRW 16.44 trillion in consolidated revenue and KRW 3.75 trillion in operating losses in the third quarter.

For the Memory Business, the PC and mobile demand improved by increasing adoption of high-density products in both DRAM and NAND and the completion of customers' inventory adjustments. The server demand for generative AI-oriented, high-density and high-end products remained strong in comparison to the sluggish demand for conventional servers.

With a focus on improving profitability, the Memory Business continued to expand sales of advanced-node products such as HBM, DDR5, LPDDR5x and UFS 4.0, and it also strived to reduce inventory levels by production adjustment rather than by aggressive sales expansion.

Overall, bit growth came in under guidance but the average selling price (ASP) of both DRAM and NAND saw some decent increases when compared to the previous quarter.

Looking to the fourth quarter, thanks to effects of peak seasonality including year-end promotions and launches of new smartphones by major mobile customers, the demand for PCs and mobile is likely to improve. Additionally, the trend of high-density penetration for both PCs and mobile devices has been accelerating more than forecasted. Cloud service providers' capital expenditure is concentrated on generative AI, so the associated server demand is expected to remain strong.

The Memory Business will expand the sales portion of highly profitable automotive products and HBM3 mass-volume business for major customers, in line with growing demand for generative AI. Through the ramp-up of Pyeongtaek Line 3, Samsung will proactively address the rising demand for new interfaces such as DDR5, LPDDR5x, PCIe Gen 5 and UFS 4.0.

Looking ahead to 2024, PC and mobile demand is likely to benefit from the arrival of some replacement cycles for products sold during the initial phase of the pandemic. For DRAM, due to the spread of On-Device AI, the high-density trend in the flagship and high-end segments is expected to continue.

Overall memory demand is expected to recover gradually thanks to increasing demand for AI and normalizing inventory levels at customers, but various factors that can affect the server market - such as geopolitical issues and IT spending trends that are related to macroeconomic conditions and centered on generative AI - need to be continuously monitored.

In the third quarter, the System LSI Business posted a slower than expected improvement in earnings due to a delayed recovery in semiconductor demand and the impact from inventory adjustments.

During the quarter, the development of E2400 was completed, which has significantly improved performance for the CPU, GPU and NPU when compared to its predecessor. In addition, the Mobile Display Driver IC (DDI) achieved the highest quarterly sales this year on the back of a new product launched by customers, while the 200-megapixel image sensor has expanded the application from wide-angle cameras to telephoto cameras.

In the fourth quarter, the System LSI Business expects earnings to improve significantly, as supply to mobile customer's new products is predicted to increase. The mobile SoC is in the final stages of development for next year's flagship smartphones and is poised to expand the business portfolio by targeting global customers for the modem business, while also enhancing the solution capabilities for On-Device AI.

In 2024, as the mobile market is expected to pursue sales growth by increasing the portion of premium models, the System LSI Business will also seek growth by increasing sales of flagship products and expanding the business area beyond the mobile market.

Earnings at the Foundry Business remained weak as a slow recovery in major applications including mobile led to a delay in fab utilization rate improvement. However, the Foundry Business did achieve a quarterly record backlog for new design wins, centering on HPC applications.

In the fourth quarter, earnings are expected to improve as demand for semiconductors will likely increase with the launch of new products by major customers. The Foundry Business is stabilizing the GAA processes by continuously improving the yield of the second-generation 3 nm process, and it also plans to secure a design infrastructure that reflects the silicon results for 2 nm.

Looking ahead to 2024, the foundry market is expected to return to a state of growth with the recovery in mobile demand and continuing increase in HPC demand. The Foundry Business plans to mass produce the second-generation 3 nm process and the fourth-generation 4 nm process for HPC applications. It will also strengthen the overall product portfolio by focusing on the development of specialty processes such as RF and eMRAM to expand into various applications such as HPC, automotive and consumer applications.

Mobile Display Posts Solid Results, Will Continue Focus on High-End Market

SDC posted KRW 8.22 trillion in consolidated revenue and KRW 1.94 trillion in operating profit for the third quarter.

For the mobile display business, SDC saw a slight increase quarter-on-quarter in market demand on the back of seasonal demand and launches of new products by major smartphone makers. SDC achieved solid results by focusing on premium OLED, with the polarizing trend intensifying between high-end and mid-range-and-below markets.

For the large display business, SDC saw earnings improve from the previous quarter as it concentrated on high-end products while strengthening operational fundamentals resulted in enhanced yields and reduced losses.

In the fourth quarter, SDC expects sales in the mobile display business to remain relatively strong thanks to seasonal effects in the smartphone and IT markets. However, growth may be limited as lingering inflation and rising interest rates impact consumer sentiment. SDC will strive to generate similar results quarter-on-quarter by leveraging competitiveness in the high-end market and featuring launches of new foldable products.

For the large display business, despite concerns over prolonged tepid demand due to the economic downturn, SDC will continue its efforts to reduce losses with an enhanced product mix including an increased share of monitors.

In 2024, in spite of persistent and adverse macro factors, SDC will seek to secure robust results by utilizing its wide capabilities, including preemptive investments, development of differentiated technologies and effective management to ensure stable quality and yield.

Furthermore, as its strategic customers are releasing new products featuring OLED in the foldable smartphone, IT OLED, automotive and gaming segments, SDC will actively promote OLED's unique selling points and create a turning point in the market.

In particular, SDC will maintain its industry leadership by developing not only technology that caters to customer needs, but also a complete supply chain - both upstream and downstream - in the high-potential AR/VR markets.

Mobile Achieves Double-Digit Profit, Will Leverage Holiday Season in Q4

The MX and Networks businesses posted KRW 30.00 trillion in consolidated revenue and KRW 3.30 trillion in operating profit for the third quarter.

Overall market demand increased from the previous quarter, driven by a recovery in the global smartphone market. The sales and profitability of the MX Business increased quarter-on-quarter, driven by the successful launch of new flagship models. New foldable devices, tablets and wearables recorded strong sales, supported by a stable supply, and the Galaxy S23 series, launched in the first half of 2023, also maintained solid sales momentum.

In the fourth quarter, due to seasonality, the smartphone market is expected to grow and experience intensified competition, especially in the premium segment. Competition is also expected to increase in the mass-market segment, while market uncertainties are expected to remain due to ongoing geopolitical instability.

The MX Business will continue to maintain steady sales of its new foldable products and the Galaxy S23 series with various sales promotions in anticipation of the year-end holiday season. For tablets and wearables, the MX Business will expand sales with a focus on new premium products, leveraging seasonality and strengthening marketing campaigns in close collaboration with partners.

In 2024, smartphone market demand is expected to rebound as consumer sentiment stabilizes in anticipation of a global economic recovery, and growth in the premium segment is expected to continue. The premium segment of the tablet market is also expected to grow, while the smartwatch market is forecasted to achieve double-digit growth, with the True Wireless Stereo market set to grow modestly.

The MX Business will focus on further enhancing the smartphone experience for customers, seeking double-digit growth in annual flagship shipments and above-market smartphone revenue growth. For tablets, an emphasis will be placed on strengthening the premium product lineup, while for wearables, priority will be on expanding sales of new models and enhancing wellness features.

Moreover, the MX Business will advance generative AI technology in core features to deliver hyper-personalized experiences, as well as acquire technologies in future growth areas such as XR, Digital Health and Digital Wallet.

Through these efforts, the MX Business aims to achieve annual growth in revenue and profit in 2024 while optimizing resources to adapt to unstable market changes and improve profitability.

Visual Display and Digital Appliances To Focus on Securing Profitability

The Visual Display and Digital Appliances businesses posted KRW 13.71 trillion in consolidated revenue and KRW 0.38 trillion in operating profit in the third quarter.

Overall market demand for TVs increased quarter-on-quarter in the third quarter, led by seasonality, but declined year-on-year due to various macroeconomic factors affecting consumer demand.

The Visual Display Business improved year-on-year profitability as it expanded its leadership in the premium market to focus on selling high-value-added products - including Neo QLEDs, OLEDs and Super Big TVs - while reducing overall costs, especially material costs.

In the fourth quarter, demand uncertainty is expected to remain unresolved due to various risks in the business environment, apart from the premium market, where solid demand is projected.

The Visual Display Business will ensure the capture of peak-season demand by enhancing its competitiveness in both online and offline channels. In addition, it aims to secure profitability by improving its high-value-added product mix with Neo QLEDs, Lifestyle Screens and Super Big TVs.

In 2024, the TV market may fluctuate due to the external risks that were also present in 2023. However, consumer sentiment is expected to turn around from this year and slightly improve to alleviate the decline in market demand.

The Visual Display Business will continue to innovate TV products, focusing on premium and lifestyle screens, to lead the ultra-high-definition and ultra-large size TV market - especially targeting demand associated with major sports events scheduled in 2024.

The Visual Display Business will continue to center on the fundamentals of TV, including picture and sound quality, as well as other features that are highly valued in the market, to allow customers to enjoy differentiated screen experiences.

View at TechPowerUp Main Site | Source

The Memory Business reduced losses sequentially as sales of high valued-added products and average selling prices somewhat increased. Earnings in system semiconductors were impacted by a delay in demand recovery for major applications, but the Foundry Business posted a new quarterly high for new backlog from design wins. The mobile panel business reported a significant increase in earnings on the back of new flagship model releases by major customers, while the large panel business narrowed losses in the quarter. The Device eXperience (DX) Division achieved solid results due to robust sales of premium smartphones and TVs. Revenue at the Networks Business declined in major overseas markets as mobile operators scaled back investments.

Harman posted a quarterly record in operating profit, led by higher sales of car audio products amid an overall increase in orders from automotive customers and also consumer audio products such as portable speakers.

In the fourth quarter, the DS Division will focus on sales of high value-added products such as High Bandwidth Memory (HBM) while also strengthening its technological leadership. Both the DX Division and Samsung Display Corporation (SDC) will seek to maintain solid profitability by focusing on premium markets.

The Memory Business plans to expand sales of HBM3 products and will address growing demand for new interfaces while increasing the portion of advanced nodes. System semiconductors are expected to post improved results on the back of new products for mobile customers.

SDC expects to maintain strong performance in the mobile panel business, driven by robust demand for premium OLED panels for smartphones. The large panel business will expand QD-OLED sales, led by year-end seasonal demand.

The DX Division will strive to maintain solid profitability by reinforcing strategies for flagship smartphones and expanding sales of premium tablets and wearable products. For TVs, the Company expects solid seasonal demand for high value-added models. The Networks Business will seek to secure new orders in overseas markets, while the Digital Appliances Business will focus on sales of premium products and strengthening the product mix.

Harman will seek to post another robust quarter by expanding sales of audio products during end-year seasonality as well as addressing the continuing demand for automotive products.

In 2024, while macroeconomic uncertainties are likely to persist, memory market conditions are expected to recover. The DS Division will seek to expand sales of advanced node products and plans to meet demand for high-performance, high-bandwidth products by increasing sales of HBM3 and HBM3E with the industry-leading HBM production capacity in the industry. For the Foundry Business, the second generation 3-nanometer (nm) Gate-All-Around (GAA) process will start mass production and operations will begin at its new factory in Taylor, Texas. Furthermore, in the Advanced Package business, production will begin, based on the multiple orders it has received from domestic and overseas HPC customers, including orders for the Company's turnkey service that combines logic, HBM and 2.5D advanced packaging technologies.

For SDC, the mobile panel business plans to meet increasing demand for new applications, while the large panel business will improve profitability by adding new products and enhancing yields.

The DX Division will focus on the premium market by increasing sales of flagship smartphone models and innovative TV products. The Company plans to expand the application of AI, provide tailored hyper-connected experiences via SmartThings and secure technologies in new areas such as XR. The Networks Business will aim to increase revenue by seeking business opportunities overseas and reinforcing technology leadership in core 5G chips and virtualized Radio Access Network (vRAN) solutions.

The Digital Appliances Business plans to strengthen the leadership in premium segments with global launches of appliances featuring AI technology. The Company plans to continue advancing the connectivity experience between SmartThings-based digital appliances and other devices.

Harman is expected to secure orders in new areas including automotive displays and will address demand for high-growth products such as home audio equipment.

In the third quarter, Samsung Electronics' capital expenditure reached KRW 11.4 trillion, including KRW 10.2 trillion spent in the Device Solutions (DS) Division and KRW 0.7 trillion in Samsung Display Corporation (SDC). The cumulative total for the January-September period is KRW 36.7 trillion, with KRW 33.4 trillion allocated to the DS Division and KRW 1.6 trillion to SDC.

The full-year capital expenditure for 2023 is expected at approximately KRW 53.7 trillion, including KRW 47.5 trillion allocated to the DS Division and KRW 3.1 trillion to SDC.

Spending on memory is expected to be concentrated in Pyeongtaek, which includes completing the P3 infrastructure and progressing the P4 framework for mid- to long-term supply. The Company remains committed to investing in new technologies, such as securing industry-leading HBM production capacity. Foundry investments are expected to increase from last year, centering on production capacity expansion in Pyeongtaek for the EUV process as well as for infrastructure investment in Taylor. For SDC, investments will mainly focus on expanding capacity for flexible displays and OLED products for IT applications.

Foundry Achieves Record Backlog From Design Wins; Memory Demand To Recover in 2024

The DS Division posted KRW 16.44 trillion in consolidated revenue and KRW 3.75 trillion in operating losses in the third quarter.

For the Memory Business, the PC and mobile demand improved by increasing adoption of high-density products in both DRAM and NAND and the completion of customers' inventory adjustments. The server demand for generative AI-oriented, high-density and high-end products remained strong in comparison to the sluggish demand for conventional servers.

With a focus on improving profitability, the Memory Business continued to expand sales of advanced-node products such as HBM, DDR5, LPDDR5x and UFS 4.0, and it also strived to reduce inventory levels by production adjustment rather than by aggressive sales expansion.

Overall, bit growth came in under guidance but the average selling price (ASP) of both DRAM and NAND saw some decent increases when compared to the previous quarter.

Looking to the fourth quarter, thanks to effects of peak seasonality including year-end promotions and launches of new smartphones by major mobile customers, the demand for PCs and mobile is likely to improve. Additionally, the trend of high-density penetration for both PCs and mobile devices has been accelerating more than forecasted. Cloud service providers' capital expenditure is concentrated on generative AI, so the associated server demand is expected to remain strong.

The Memory Business will expand the sales portion of highly profitable automotive products and HBM3 mass-volume business for major customers, in line with growing demand for generative AI. Through the ramp-up of Pyeongtaek Line 3, Samsung will proactively address the rising demand for new interfaces such as DDR5, LPDDR5x, PCIe Gen 5 and UFS 4.0.

Looking ahead to 2024, PC and mobile demand is likely to benefit from the arrival of some replacement cycles for products sold during the initial phase of the pandemic. For DRAM, due to the spread of On-Device AI, the high-density trend in the flagship and high-end segments is expected to continue.

Overall memory demand is expected to recover gradually thanks to increasing demand for AI and normalizing inventory levels at customers, but various factors that can affect the server market - such as geopolitical issues and IT spending trends that are related to macroeconomic conditions and centered on generative AI - need to be continuously monitored.

In the third quarter, the System LSI Business posted a slower than expected improvement in earnings due to a delayed recovery in semiconductor demand and the impact from inventory adjustments.

During the quarter, the development of E2400 was completed, which has significantly improved performance for the CPU, GPU and NPU when compared to its predecessor. In addition, the Mobile Display Driver IC (DDI) achieved the highest quarterly sales this year on the back of a new product launched by customers, while the 200-megapixel image sensor has expanded the application from wide-angle cameras to telephoto cameras.

In the fourth quarter, the System LSI Business expects earnings to improve significantly, as supply to mobile customer's new products is predicted to increase. The mobile SoC is in the final stages of development for next year's flagship smartphones and is poised to expand the business portfolio by targeting global customers for the modem business, while also enhancing the solution capabilities for On-Device AI.

In 2024, as the mobile market is expected to pursue sales growth by increasing the portion of premium models, the System LSI Business will also seek growth by increasing sales of flagship products and expanding the business area beyond the mobile market.

Earnings at the Foundry Business remained weak as a slow recovery in major applications including mobile led to a delay in fab utilization rate improvement. However, the Foundry Business did achieve a quarterly record backlog for new design wins, centering on HPC applications.

In the fourth quarter, earnings are expected to improve as demand for semiconductors will likely increase with the launch of new products by major customers. The Foundry Business is stabilizing the GAA processes by continuously improving the yield of the second-generation 3 nm process, and it also plans to secure a design infrastructure that reflects the silicon results for 2 nm.

Looking ahead to 2024, the foundry market is expected to return to a state of growth with the recovery in mobile demand and continuing increase in HPC demand. The Foundry Business plans to mass produce the second-generation 3 nm process and the fourth-generation 4 nm process for HPC applications. It will also strengthen the overall product portfolio by focusing on the development of specialty processes such as RF and eMRAM to expand into various applications such as HPC, automotive and consumer applications.

Mobile Display Posts Solid Results, Will Continue Focus on High-End Market

SDC posted KRW 8.22 trillion in consolidated revenue and KRW 1.94 trillion in operating profit for the third quarter.

For the mobile display business, SDC saw a slight increase quarter-on-quarter in market demand on the back of seasonal demand and launches of new products by major smartphone makers. SDC achieved solid results by focusing on premium OLED, with the polarizing trend intensifying between high-end and mid-range-and-below markets.

For the large display business, SDC saw earnings improve from the previous quarter as it concentrated on high-end products while strengthening operational fundamentals resulted in enhanced yields and reduced losses.

In the fourth quarter, SDC expects sales in the mobile display business to remain relatively strong thanks to seasonal effects in the smartphone and IT markets. However, growth may be limited as lingering inflation and rising interest rates impact consumer sentiment. SDC will strive to generate similar results quarter-on-quarter by leveraging competitiveness in the high-end market and featuring launches of new foldable products.

For the large display business, despite concerns over prolonged tepid demand due to the economic downturn, SDC will continue its efforts to reduce losses with an enhanced product mix including an increased share of monitors.

In 2024, in spite of persistent and adverse macro factors, SDC will seek to secure robust results by utilizing its wide capabilities, including preemptive investments, development of differentiated technologies and effective management to ensure stable quality and yield.

Furthermore, as its strategic customers are releasing new products featuring OLED in the foldable smartphone, IT OLED, automotive and gaming segments, SDC will actively promote OLED's unique selling points and create a turning point in the market.

In particular, SDC will maintain its industry leadership by developing not only technology that caters to customer needs, but also a complete supply chain - both upstream and downstream - in the high-potential AR/VR markets.

Mobile Achieves Double-Digit Profit, Will Leverage Holiday Season in Q4

The MX and Networks businesses posted KRW 30.00 trillion in consolidated revenue and KRW 3.30 trillion in operating profit for the third quarter.

Overall market demand increased from the previous quarter, driven by a recovery in the global smartphone market. The sales and profitability of the MX Business increased quarter-on-quarter, driven by the successful launch of new flagship models. New foldable devices, tablets and wearables recorded strong sales, supported by a stable supply, and the Galaxy S23 series, launched in the first half of 2023, also maintained solid sales momentum.

In the fourth quarter, due to seasonality, the smartphone market is expected to grow and experience intensified competition, especially in the premium segment. Competition is also expected to increase in the mass-market segment, while market uncertainties are expected to remain due to ongoing geopolitical instability.

The MX Business will continue to maintain steady sales of its new foldable products and the Galaxy S23 series with various sales promotions in anticipation of the year-end holiday season. For tablets and wearables, the MX Business will expand sales with a focus on new premium products, leveraging seasonality and strengthening marketing campaigns in close collaboration with partners.

In 2024, smartphone market demand is expected to rebound as consumer sentiment stabilizes in anticipation of a global economic recovery, and growth in the premium segment is expected to continue. The premium segment of the tablet market is also expected to grow, while the smartwatch market is forecasted to achieve double-digit growth, with the True Wireless Stereo market set to grow modestly.

The MX Business will focus on further enhancing the smartphone experience for customers, seeking double-digit growth in annual flagship shipments and above-market smartphone revenue growth. For tablets, an emphasis will be placed on strengthening the premium product lineup, while for wearables, priority will be on expanding sales of new models and enhancing wellness features.

Moreover, the MX Business will advance generative AI technology in core features to deliver hyper-personalized experiences, as well as acquire technologies in future growth areas such as XR, Digital Health and Digital Wallet.

Through these efforts, the MX Business aims to achieve annual growth in revenue and profit in 2024 while optimizing resources to adapt to unstable market changes and improve profitability.

Visual Display and Digital Appliances To Focus on Securing Profitability

The Visual Display and Digital Appliances businesses posted KRW 13.71 trillion in consolidated revenue and KRW 0.38 trillion in operating profit in the third quarter.

Overall market demand for TVs increased quarter-on-quarter in the third quarter, led by seasonality, but declined year-on-year due to various macroeconomic factors affecting consumer demand.

The Visual Display Business improved year-on-year profitability as it expanded its leadership in the premium market to focus on selling high-value-added products - including Neo QLEDs, OLEDs and Super Big TVs - while reducing overall costs, especially material costs.

In the fourth quarter, demand uncertainty is expected to remain unresolved due to various risks in the business environment, apart from the premium market, where solid demand is projected.

The Visual Display Business will ensure the capture of peak-season demand by enhancing its competitiveness in both online and offline channels. In addition, it aims to secure profitability by improving its high-value-added product mix with Neo QLEDs, Lifestyle Screens and Super Big TVs.

In 2024, the TV market may fluctuate due to the external risks that were also present in 2023. However, consumer sentiment is expected to turn around from this year and slightly improve to alleviate the decline in market demand.

The Visual Display Business will continue to innovate TV products, focusing on premium and lifestyle screens, to lead the ultra-high-definition and ultra-large size TV market - especially targeting demand associated with major sports events scheduled in 2024.

The Visual Display Business will continue to center on the fundamentals of TV, including picture and sound quality, as well as other features that are highly valued in the market, to allow customers to enjoy differentiated screen experiences.

View at TechPowerUp Main Site | Source