TheLostSwede

News Editor

- Joined

- Nov 11, 2004

- Messages

- 18,376 (2.46/day)

- Location

- Sweden

| System Name | Overlord Mk MLI |

|---|---|

| Processor | AMD Ryzen 7 7800X3D |

| Motherboard | Gigabyte X670E Aorus Master |

| Cooling | Noctua NH-D15 SE with offsets |

| Memory | 32GB Team T-Create Expert DDR5 6000 MHz @ CL30-34-34-68 |

| Video Card(s) | Gainward GeForce RTX 4080 Phantom GS |

| Storage | 1TB Solidigm P44 Pro, 2 TB Corsair MP600 Pro, 2TB Kingston KC3000 |

| Display(s) | Acer XV272K LVbmiipruzx 4K@160Hz |

| Case | Fractal Design Torrent Compact |

| Audio Device(s) | Corsair Virtuoso SE |

| Power Supply | be quiet! Pure Power 12 M 850 W |

| Mouse | Logitech G502 Lightspeed |

| Keyboard | Corsair K70 Max |

| Software | Windows 10 Pro |

| Benchmark Scores | https://valid.x86.fr/yfsd9w |

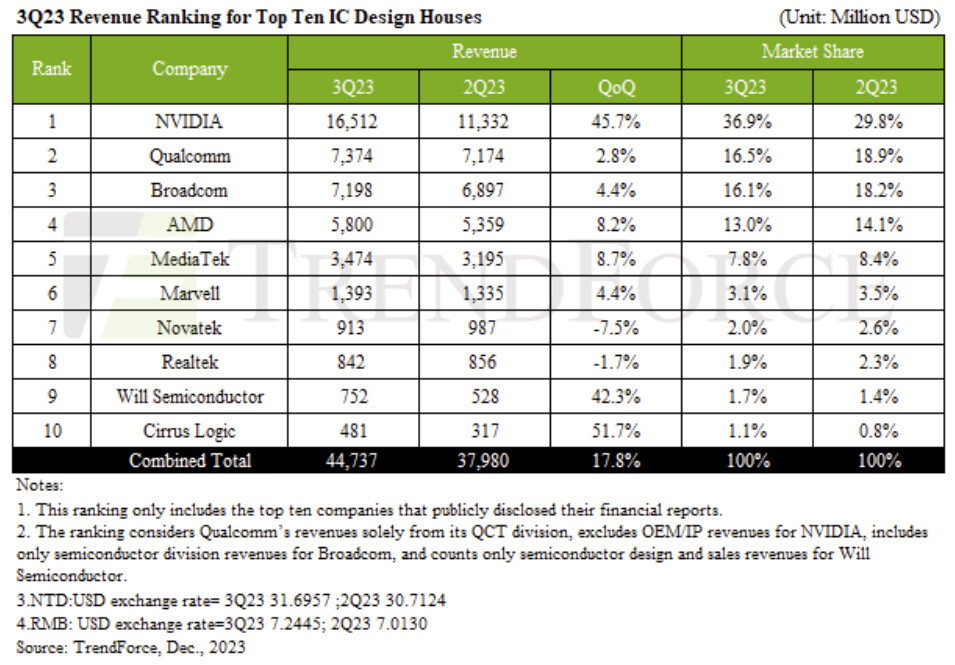

TrendForce reports that 3Q23 has been a historic quarter for the world's leading IC design houses as total revenue soared 17.8% to reach a record-breaking US$44.7 billion. This remarkable growth is fueled by a robust season of stockpiling for smartphones and laptops, combined with a rapid acceleration in the shipment of generative AI chips and components. NVIDIA, capitalizing on the AI boom, emerged as the top performer in revenue and market share. Notably, analog IC supplier Cirrus Logic overtook US PMIC manufacturer MPS to snatch the tenth spot, driven by strong demand for smartphone stockpiling.

NVIDIA's revenue soared 45.7% to US$16.5 billion in the third quarter, bolstered by sustained demand for generative AI and LLMs. Its data center business—accounting for nearly 80% of its revenue—was a key driver in this exceptional growth.

Qualcomm, riding the wave of its newly launched flagship AP Snapdragon 8 Gen 3 and the release of new Android smartphones, saw its third-quarter revenue climb by 2.8% QoQ to around US$7.4 billion. However, NVIDIA's rapid growth eroded Qualcomm's market share to 16.5%. Broadcom, with its strategic emphasis on AI server-related products like AI ASIC chips, high-end switches, and network interface cards, along with its seasonal wireless product stockpiling, managed to offset weaker demand in server storage connectivity and broadband. This strategic maneuvering led to a 4.4% QoQ revenue boost to US$7.2 billion.

AMD witnessed an 8.2% increase in its 3Q revenue, reaching US$5.8 billion. This success was due to the widespread adoption of its 4th Gen EPYC server CPUs by cloud and enterprise customers and the favorable impact of seasonal laptop stockpiling. MediaTek's revenue rose by 8.7% to US$3.5 billion in the third quarter, buoyed by a healthy replenishment demand for smartphone APs, WiFi 6, and mobile/laptop PMIC components, as inventories across brand clients stabilized.

Cirrus Logic ousts MPS from tenth position thanks to smartphone inventory replenishment

Marvell also made significant gains, with its third-quarter revenue hitting US$1.4 billion, a 4.4% QoQ increase. This growth was primarily driven by increasing demand for generative AI from cloud clients and the expansion of its data center business—despite declines in sectors like enterprise networking and automotive. However, the outlook for some sectors remains mixed, with areas like TV and networking still facing uncertainties, leading to a cautious approach from clients. This resulted in some IC design companies, such as Novatek and Realtek, witnessing a decline in revenues by 7.5% and 1.7%, respectively.

Will Semiconductor benefited from the demand for Android smartphone components, breaking free from past inventory corrections with a 42.3% increase in 3Q revenue to US$752 million. Cirrus Logic, similarly capitalizing on the smartphone component stockpiling trend, saw a significant 51.7% jump in revenue to US$481 million, ousting MPS from the top ten.

In summary, TrendForce forecasts sustained growth for the top ten IC design houses in the upcoming fourth quarter. This optimistic outlook is underpinned by a gradual normalization of inventory levels and a modest seasonal rebound in the smartphone and notebook market. Additionally, the global surge in LLMs extends beyond CSPs, internet companies, and private enterprises, reaching regional countries and small-to-medium businesses, further bolstering this positive revenue trend.

View at TechPowerUp Main Site | Source

NVIDIA's revenue soared 45.7% to US$16.5 billion in the third quarter, bolstered by sustained demand for generative AI and LLMs. Its data center business—accounting for nearly 80% of its revenue—was a key driver in this exceptional growth.

Qualcomm, riding the wave of its newly launched flagship AP Snapdragon 8 Gen 3 and the release of new Android smartphones, saw its third-quarter revenue climb by 2.8% QoQ to around US$7.4 billion. However, NVIDIA's rapid growth eroded Qualcomm's market share to 16.5%. Broadcom, with its strategic emphasis on AI server-related products like AI ASIC chips, high-end switches, and network interface cards, along with its seasonal wireless product stockpiling, managed to offset weaker demand in server storage connectivity and broadband. This strategic maneuvering led to a 4.4% QoQ revenue boost to US$7.2 billion.

AMD witnessed an 8.2% increase in its 3Q revenue, reaching US$5.8 billion. This success was due to the widespread adoption of its 4th Gen EPYC server CPUs by cloud and enterprise customers and the favorable impact of seasonal laptop stockpiling. MediaTek's revenue rose by 8.7% to US$3.5 billion in the third quarter, buoyed by a healthy replenishment demand for smartphone APs, WiFi 6, and mobile/laptop PMIC components, as inventories across brand clients stabilized.

Cirrus Logic ousts MPS from tenth position thanks to smartphone inventory replenishment

Marvell also made significant gains, with its third-quarter revenue hitting US$1.4 billion, a 4.4% QoQ increase. This growth was primarily driven by increasing demand for generative AI from cloud clients and the expansion of its data center business—despite declines in sectors like enterprise networking and automotive. However, the outlook for some sectors remains mixed, with areas like TV and networking still facing uncertainties, leading to a cautious approach from clients. This resulted in some IC design companies, such as Novatek and Realtek, witnessing a decline in revenues by 7.5% and 1.7%, respectively.

Will Semiconductor benefited from the demand for Android smartphone components, breaking free from past inventory corrections with a 42.3% increase in 3Q revenue to US$752 million. Cirrus Logic, similarly capitalizing on the smartphone component stockpiling trend, saw a significant 51.7% jump in revenue to US$481 million, ousting MPS from the top ten.

In summary, TrendForce forecasts sustained growth for the top ten IC design houses in the upcoming fourth quarter. This optimistic outlook is underpinned by a gradual normalization of inventory levels and a modest seasonal rebound in the smartphone and notebook market. Additionally, the global surge in LLMs extends beyond CSPs, internet companies, and private enterprises, reaching regional countries and small-to-medium businesses, further bolstering this positive revenue trend.

View at TechPowerUp Main Site | Source