- Joined

- Oct 9, 2007

- Messages

- 47,511 (7.49/day)

- Location

- Hyderabad, India

| System Name | RBMK-1000 |

|---|---|

| Processor | AMD Ryzen 7 5700G |

| Motherboard | ASUS ROG Strix B450-E Gaming |

| Cooling | DeepCool Gammax L240 V2 |

| Memory | 2x 8GB G.Skill Sniper X |

| Video Card(s) | Palit GeForce RTX 2080 SUPER GameRock |

| Storage | Western Digital Black NVMe 512GB |

| Display(s) | BenQ 1440p 60 Hz 27-inch |

| Case | Corsair Carbide 100R |

| Audio Device(s) | ASUS SupremeFX S1220A |

| Power Supply | Cooler Master MWE Gold 650W |

| Mouse | ASUS ROG Strix Impact |

| Keyboard | Gamdias Hermes E2 |

| Software | Windows 11 Pro |

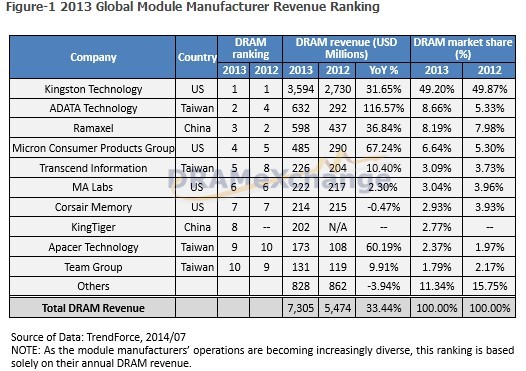

The global PC DRAM module market revenues arrived at US$ 7.3 billion in 2013, a 32% YoY increase from 2012's US$ 5.5 billion, according to DRAMeXchange, the memory and storage research division of TrendForce. The main factors leading to the revenue growth included price increases for PC DRAM, increased spot market demand, and the rising proportion of contract market transactions. The top ten module manufacturers accounted for nearly 88% of the entire market's revenue in 2013, with Kingston Technology maintaining its usual leading position within the industry. ADATA Technology and Ramaxel, which ended up in second and third place, respectively, showed respective revenue growth of 116% and 37%. As the module manufacturers' operations are becoming increasingly diverse, the ranking for 2013 is based solely on their annual DRAM revenue.

2013 was definitely a strong year for the entire DRAM industry as far as price growth is concerned, pointed out DRAMeXchange. The DRAM market's transformation into an oligopoly has enabled the market's supply and demand to be more tightly regulated, while the top tier DRAM manufacturers' decision to transition to Mobile DRAM following the increased sales of smartphones and tablets caused PC DRAM supply to tighten. The DDR3 4Gb contract prices, as a result of the restricted PC DRAM supplies, rose from a low of US$ 1.84 to US$ 3.94, a 114% increase. The spot market price for DDR3 4Gb, on the other hand, rose approximately 88% to US$ 4.27 thanks to the DRAM manufacturers' decision to prioritize supplies for PC-OEM clients in 2013. At present, the difference between the contract and spot prices is still around 20%. Though uncommon in the industry, the simultaneous contract and spot price growth has provided a notable boost to the module manufacturers' annual revenues.

As before, Kingston Technology is able to secure the top position in the 2013 module industry thanks to its success in the contract and spot markets. In recent periods, the eMCP product lines developed by the company's subsidiary, KSI, has enabled it to increase its revenues in the China market, and in turn encouraged it to set its target on the first tier manufacturers' supply chains. ADATA, which finished in the second place, managed to increase its revenues by a hefty 116% in 2013 and was able to retain a leading position in Taiwan's module memory market due to its low cost inventory and flexible business strategies. Benefiting from the product orders from domestic clients such as Lenovo and the strong sales momentum in foreign markets, Ramaxel ended in third place in 2013, and saw its revenues grow by 37%. Thanks to the consistently stable supplies from its parent company, Micron, Crucial Technology (whose official name is set to be changed to Micron Consumer Products Group in the future), ended up in the fourth place. Transcend rose from the eighth to fifth spot this year due to the major growth in the sales of its industry memory products.

View at TechPowerUp Main Site

2013 was definitely a strong year for the entire DRAM industry as far as price growth is concerned, pointed out DRAMeXchange. The DRAM market's transformation into an oligopoly has enabled the market's supply and demand to be more tightly regulated, while the top tier DRAM manufacturers' decision to transition to Mobile DRAM following the increased sales of smartphones and tablets caused PC DRAM supply to tighten. The DDR3 4Gb contract prices, as a result of the restricted PC DRAM supplies, rose from a low of US$ 1.84 to US$ 3.94, a 114% increase. The spot market price for DDR3 4Gb, on the other hand, rose approximately 88% to US$ 4.27 thanks to the DRAM manufacturers' decision to prioritize supplies for PC-OEM clients in 2013. At present, the difference between the contract and spot prices is still around 20%. Though uncommon in the industry, the simultaneous contract and spot price growth has provided a notable boost to the module manufacturers' annual revenues.

As before, Kingston Technology is able to secure the top position in the 2013 module industry thanks to its success in the contract and spot markets. In recent periods, the eMCP product lines developed by the company's subsidiary, KSI, has enabled it to increase its revenues in the China market, and in turn encouraged it to set its target on the first tier manufacturers' supply chains. ADATA, which finished in the second place, managed to increase its revenues by a hefty 116% in 2013 and was able to retain a leading position in Taiwan's module memory market due to its low cost inventory and flexible business strategies. Benefiting from the product orders from domestic clients such as Lenovo and the strong sales momentum in foreign markets, Ramaxel ended in third place in 2013, and saw its revenues grow by 37%. Thanks to the consistently stable supplies from its parent company, Micron, Crucial Technology (whose official name is set to be changed to Micron Consumer Products Group in the future), ended up in the fourth place. Transcend rose from the eighth to fifth spot this year due to the major growth in the sales of its industry memory products.

View at TechPowerUp Main Site