TheLostSwede

News Editor

- Joined

- Nov 11, 2004

- Messages

- 18,139 (2.45/day)

- Location

- Sweden

| System Name | Overlord Mk MLI |

|---|---|

| Processor | AMD Ryzen 7 7800X3D |

| Motherboard | Gigabyte X670E Aorus Master |

| Cooling | Noctua NH-D15 SE with offsets |

| Memory | 32GB Team T-Create Expert DDR5 6000 MHz @ CL30-34-34-68 |

| Video Card(s) | Gainward GeForce RTX 4080 Phantom GS |

| Storage | 1TB Solidigm P44 Pro, 2 TB Corsair MP600 Pro, 2TB Kingston KC3000 |

| Display(s) | Acer XV272K LVbmiipruzx 4K@160Hz |

| Case | Fractal Design Torrent Compact |

| Audio Device(s) | Corsair Virtuoso SE |

| Power Supply | be quiet! Pure Power 12 M 850 W |

| Mouse | Logitech G502 Lightspeed |

| Keyboard | Corsair K70 Max |

| Software | Windows 10 Pro |

| Benchmark Scores | https://valid.x86.fr/yfsd9w |

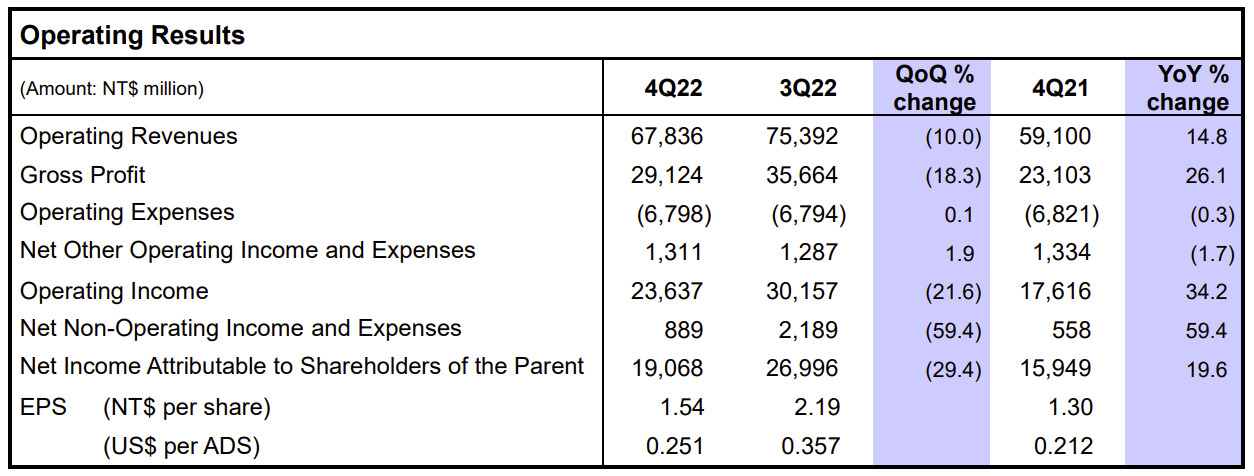

United Microelectronics Corporation ("UMC" or "The Company"), a leading global semiconductor foundry, today announced its consolidated operating results for the fourth quarter of 2022. Fourth quarter consolidated revenue was NT$67.84 billion, decreasing 10.0% QoQ from NT$75.39 billion in 3Q22. Compared to a year ago, 4Q22 revenue grew 14.8% YoY from NT$59.10 billion in 4Q21. Consolidated gross margin for 4Q22 was 42.9%. Net income attributable to the shareholders of the parent was NT$19.1 billion, with earnings per ordinary share of NT$1.54.

Jason Wang, co-president of UMC, said, "In the fourth quarter, due to a significant slowdown across most of our end markets and inventory correction in the semiconductor industry, our wafer shipments fell 14.8% QoQ while overall fab utilization rate dropped to 90%. Average selling price increased slightly during the quarter as a result of our ongoing product mix optimization efforts, moderating the decline in revenue."

"For the full year 2022, UMC's revenue hit a record high of NT$278.7 billion while operating income exceeded NT$100 billion. Gross margin reached 45%, driven by a more favorable foreign exchange rate, expanding 22/28 nm portfolio, and newly added capacity. We had taken advantage of the industry upturn over the past two years to enhance our differentiation in specialty technology offering, improve profitability, and deepen relationships with key customers. Revenue from 22/28 nm technologies increased more than 56% YoY, driven by our industry-leading 28 nm process for OLED display drivers and image signal processors. Our automotive segment also delivered impressive growth in 2022, increasing 82% YoY to account for approximately 9% of total sales. We expect this segment will continue to be a key growth catalyst in 2023 and beyond, driven by the long-term trend of vehicle electrification and automation. UMC is well positioned to serve the market with our comprehensive portfolio of auto-grade process technologies and facilities certified according to rigorous quality standards, while we continue to build strong partnerships with world-class automotive leaders."

Co-president Wang commented, "Given the soft global economic outlook for 2023, we expect the current challenging environment to persist through the first quarter as customers' days of inventory are still higher than normal while order visibility remains low. To manage this period of weakness, the Company is implementing strict cost control measures and deferring certain capital expenditures where possible. In the longer term, we remain positive that UMC's differentiated

specialty technology leadership, geographically diversified capacity offering, and quality and operational excellence will enable the Company to capture demand fueled by continuous digital transformation across industries and be the foundry of choice for leading customers."

Co-president Wang added, "In 2022, we took solid steps in executing our net zero by 2050 roadmap. As part of our efforts to reduce emissions across the entire value chain, UMC recently introduced a program to empower our suppliers with resources to measure and manage their emissions output. To round out the important progress we made towards our ESG goals this year, we were honored to receive recognition from domestic and international institutions. In the 2022 Dow Jones Sustainability Indices (DJSI), UMC was ranked first in terms of overall sustainability performance among semiconductor foundry peers in the 2022 DJSI, while we were the only semiconductor firm globally to achieve double-A scoring for climate change and water security in CDP's annual evaluation of corporate environmental action. Sustainability and a company's longterm success are inextricably linked, and UMC will continue to strive to meet expectations of all of our stakeholders while acting as responsible social and environment stewards."

Fourth quarter operating revenues declined by 10.0% sequentially to NT$67.84 billion resulting from the inventory correction within the semi industry which lowered wafer shipments. Revenue contribution from 40 nm and below technologies represented 45% of wafer revenue. Gross profit decreased 18.3% QoQ to NT$29.12 billion, or 42.9% of revenue. Operating expenses remained flat at NT$6.80 billion. Net other operating income increased to NT$1.31 billion. Net non-operating income totaled NT$0.89 billion. Net income attributable to shareholders of the parent amounted to NT$19.07 billion.

Earnings per ordinary share for the quarter was NT$1.54. Earnings per ADS was US$0.251. The basic weighted average number of shares outstanding in 4Q22 was

12,348,880,384, compared with 12,305,516,644 shares in 3Q22 and 12,254,114,875 shares in 4Q21. The diluted weighted average number of shares outstanding was 12,684,106,050 in 4Q22, compared with 12,635,661,561 shares in 3Q22 and 12,489,949,678 shares in 4Q21. The fully diluted shares counted on December 31, 2022 were approximately 12,684,106,000.

Quarter-over-Quarter Guidance:

View at TechPowerUp Main Site | Source

Jason Wang, co-president of UMC, said, "In the fourth quarter, due to a significant slowdown across most of our end markets and inventory correction in the semiconductor industry, our wafer shipments fell 14.8% QoQ while overall fab utilization rate dropped to 90%. Average selling price increased slightly during the quarter as a result of our ongoing product mix optimization efforts, moderating the decline in revenue."

"For the full year 2022, UMC's revenue hit a record high of NT$278.7 billion while operating income exceeded NT$100 billion. Gross margin reached 45%, driven by a more favorable foreign exchange rate, expanding 22/28 nm portfolio, and newly added capacity. We had taken advantage of the industry upturn over the past two years to enhance our differentiation in specialty technology offering, improve profitability, and deepen relationships with key customers. Revenue from 22/28 nm technologies increased more than 56% YoY, driven by our industry-leading 28 nm process for OLED display drivers and image signal processors. Our automotive segment also delivered impressive growth in 2022, increasing 82% YoY to account for approximately 9% of total sales. We expect this segment will continue to be a key growth catalyst in 2023 and beyond, driven by the long-term trend of vehicle electrification and automation. UMC is well positioned to serve the market with our comprehensive portfolio of auto-grade process technologies and facilities certified according to rigorous quality standards, while we continue to build strong partnerships with world-class automotive leaders."

Co-president Wang commented, "Given the soft global economic outlook for 2023, we expect the current challenging environment to persist through the first quarter as customers' days of inventory are still higher than normal while order visibility remains low. To manage this period of weakness, the Company is implementing strict cost control measures and deferring certain capital expenditures where possible. In the longer term, we remain positive that UMC's differentiated

specialty technology leadership, geographically diversified capacity offering, and quality and operational excellence will enable the Company to capture demand fueled by continuous digital transformation across industries and be the foundry of choice for leading customers."

Co-president Wang added, "In 2022, we took solid steps in executing our net zero by 2050 roadmap. As part of our efforts to reduce emissions across the entire value chain, UMC recently introduced a program to empower our suppliers with resources to measure and manage their emissions output. To round out the important progress we made towards our ESG goals this year, we were honored to receive recognition from domestic and international institutions. In the 2022 Dow Jones Sustainability Indices (DJSI), UMC was ranked first in terms of overall sustainability performance among semiconductor foundry peers in the 2022 DJSI, while we were the only semiconductor firm globally to achieve double-A scoring for climate change and water security in CDP's annual evaluation of corporate environmental action. Sustainability and a company's longterm success are inextricably linked, and UMC will continue to strive to meet expectations of all of our stakeholders while acting as responsible social and environment stewards."

Fourth quarter operating revenues declined by 10.0% sequentially to NT$67.84 billion resulting from the inventory correction within the semi industry which lowered wafer shipments. Revenue contribution from 40 nm and below technologies represented 45% of wafer revenue. Gross profit decreased 18.3% QoQ to NT$29.12 billion, or 42.9% of revenue. Operating expenses remained flat at NT$6.80 billion. Net other operating income increased to NT$1.31 billion. Net non-operating income totaled NT$0.89 billion. Net income attributable to shareholders of the parent amounted to NT$19.07 billion.

Earnings per ordinary share for the quarter was NT$1.54. Earnings per ADS was US$0.251. The basic weighted average number of shares outstanding in 4Q22 was

12,348,880,384, compared with 12,305,516,644 shares in 3Q22 and 12,254,114,875 shares in 4Q21. The diluted weighted average number of shares outstanding was 12,684,106,050 in 4Q22, compared with 12,635,661,561 shares in 3Q22 and 12,489,949,678 shares in 4Q21. The fully diluted shares counted on December 31, 2022 were approximately 12,684,106,000.

Quarter-over-Quarter Guidance:

- Wafer Shipments: To decrease in the high teens % range

- ASP in USD: To remain flat

- Gross Profit Margin: Will be in the mid-30% range

- Capacity Utilization: approximately 70%

- 2023 CAPEX: US$3.0 billion

View at TechPowerUp Main Site | Source