- Joined

- Oct 9, 2007

- Messages

- 47,527 (7.48/day)

- Location

- Hyderabad, India

| System Name | RBMK-1000 |

|---|---|

| Processor | AMD Ryzen 7 5700G |

| Motherboard | ASUS ROG Strix B450-E Gaming |

| Cooling | DeepCool Gammax L240 V2 |

| Memory | 2x 8GB G.Skill Sniper X |

| Video Card(s) | Palit GeForce RTX 2080 SUPER GameRock |

| Storage | Western Digital Black NVMe 512GB |

| Display(s) | BenQ 1440p 60 Hz 27-inch |

| Case | Corsair Carbide 100R |

| Audio Device(s) | ASUS SupremeFX S1220A |

| Power Supply | Cooler Master MWE Gold 650W |

| Mouse | ASUS ROG Strix Impact |

| Keyboard | Gamdias Hermes E2 |

| Software | Windows 11 Pro |

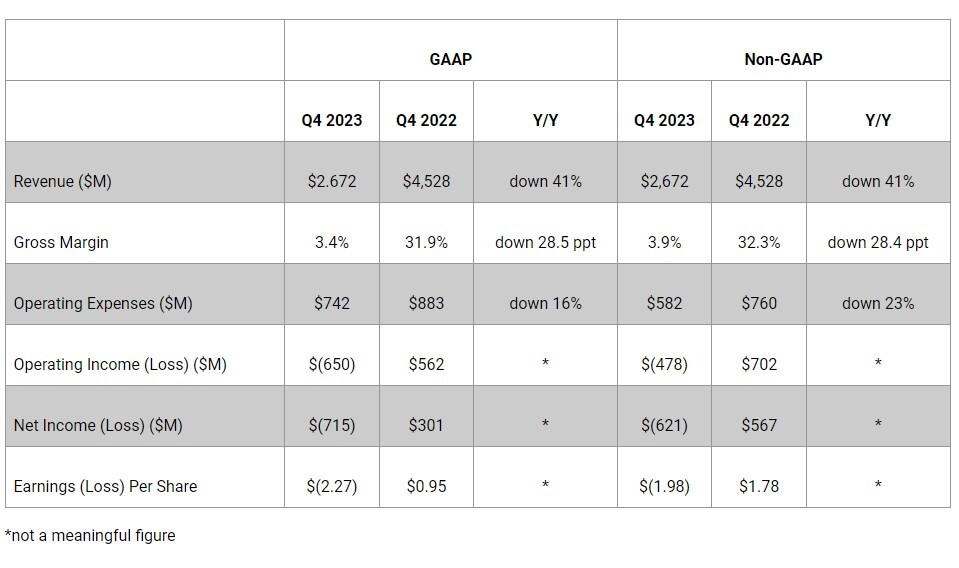

Western Digital Corp. (Nasdaq: WDC) today reported fiscal fourth quarter and fiscal year 2023 financial results. "Throughout the fiscal fourth quarter and fiscal year, Western Digital continued to optimize our operations and successfully execute our innovative product roadmap, priming ourselves for greater profitability when demand rebounds across hard drives and flash. As a result of these efforts, we delivered revenue above our expectation and delivered a range of industry-leading products to our customers," said David Goeckeler, Western Digital CEO.

"We are encouraged by several indicators signaling improving Flash market dynamics. Our two largest end markets, Client and Consumer, are returning to growth, inventories are normalizing, content per unit is increasing and price declines have been moderating. Western Digital is well-positioned to capitalize on improving market conditions and capture long-term growth opportunities in data storage, spanning from client to edge to cloud," continued David Goeckeler.

Summary

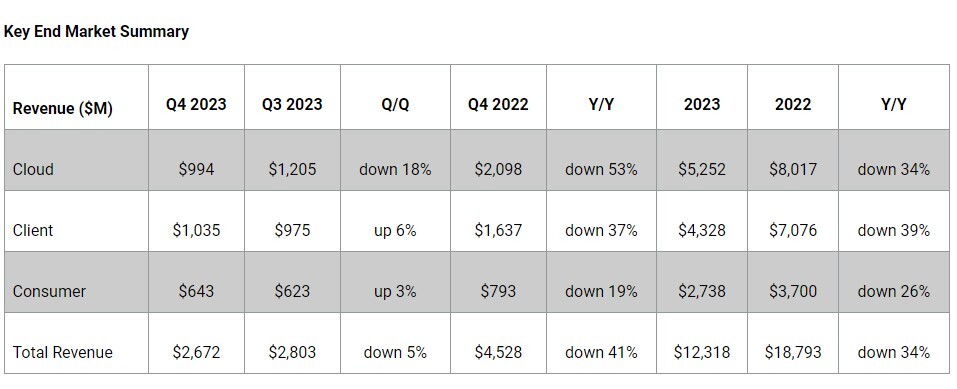

Key End Market Summary

In the fiscal fourth quarter:

View at TechPowerUp Main Site

"We are encouraged by several indicators signaling improving Flash market dynamics. Our two largest end markets, Client and Consumer, are returning to growth, inventories are normalizing, content per unit is increasing and price declines have been moderating. Western Digital is well-positioned to capitalize on improving market conditions and capture long-term growth opportunities in data storage, spanning from client to edge to cloud," continued David Goeckeler.

Summary

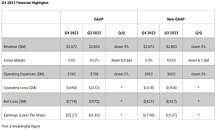

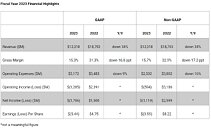

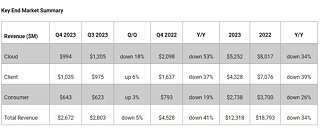

- Fourth quarter revenue was $2.7 billion, down 5% sequentially (QoQ). Cloud revenue decreased 18% (QoQ), Client revenue increased 6% and Consumer revenue increased 3% (QoQ). Fiscal year 2023 revenue was $12.3 billion.

- Fourth quarter GAAP earnings per share (EPS) was $(2.27) and Non-GAAP EPS was $(1.98), which includes $211 million of underutilization related charges in Flash and HDD. Fiscal year 2023 GAAP EPS was $(5.44) and Non-GAAP EPS was $(3.59).

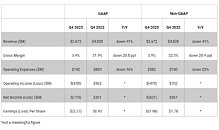

- Expect fiscal first quarter 2024 revenue to be in the range of $2.55 billion to $2.75 billion.

- Expect Non-GAAP EPS in the range of $(2.10) to $(1.80) which includes $200 to $220 million of underutilization charges in Flash and HDD.

Key End Market Summary

In the fiscal fourth quarter:

- Cloud represented 37% of total revenue. Sequentially, the decline was primarily due to a decrease in capacity enterprise drive shipments. The year-over-year decrease was primarily due to declines in both hard drive and flash product shipments.

- Client represented 39% of total revenue. Sequentially, the increase was driven by growth in bit shipments for gaming consoles. The year-over-year decrease was due to declines in flash pricing, and lower client SSD and hard drive unit shipments for PC applications.

- Consumer represented 24% of total revenue. Sequentially, the increase was primarily due to higher retail SSD shipments. The year-over-year decrease was driven by price declines in Flash and lower retail hard drive shipments.

- Cloud represented 43% of total revenue. The year-over-year decrease was primarily due to reduced shipments of capacity enterprise hard drives and enterprise SSDs.

- Client represented 35% of total revenue. The year-over-year decrease was primarily due to declines in flash pricing, as well as lower client SSD and hard drive unit shipments for PC applications.

- Consumer represented 22% of total revenue. Revenue decreased year-over-year, as growth in retail SSD bit shipments was more than offset by broad-based flash price decline and lower consumer hard drive shipments.

View at TechPowerUp Main Site