Monday, September 11th 2023

Microsoft Introduces Xbox Mastercard - Outlines Perks for Gamers

We know players are interested in getting more value from Xbox, and we've heard feedback from the community that they want more ways to get value from their purchases. Today, I'm excited to share that we are introducing the no annual fee1 Xbox Mastercard in partnership with Barclays US Consumer Bank, a leading co-branded credit card issuer in the United States.

With the Xbox Mastercard credit card, players can earn card points with everyday purchases to redeem on games and add-ons at xbox.com. The Xbox Mastercard will be available exclusively to Xbox Insiders in the 50 United States beginning on September 21, with availability to all Xbox players in the 50 United States coming in 2024.

With the Xbox Mastercard, players can earn card points for every $1 spent on purchases including:

With the Xbox Mastercard, players can earn card points for every $1 spent on purchases including: Cardmembers will also get access to more benefits including:

Cardmembers will also get access to more benefits including:

Application details can be viewed here. If you're an Xbox Insider with residence in the continental United States, Alaska, or Hawaii, you can apply starting on September 21. The Xbox Mastercard will be available in waves to Xbox Insiders throughout this fall.

Source:

Xbox News

With the Xbox Mastercard credit card, players can earn card points with everyday purchases to redeem on games and add-ons at xbox.com. The Xbox Mastercard will be available exclusively to Xbox Insiders in the 50 United States beginning on September 21, with availability to all Xbox players in the 50 United States coming in 2024.

- Xbox & Microsoft - Earn 5x card points on eligible products at the Microsoft Store.

- Streaming Services - Earn 3x card points on eligible streaming services like Netflix and Disney+.

- Dining Delivery Services - Earn 3x card points on eligible dining delivery services like Grubhub and DoorDash.

- Everyday purchases - Earn 1x card points on all other everyday purchases.

- A bonus of 5,000 card points (a $50 value) after their first purchase.

- Three months of Xbox Game Pass Ultimate for new Game Pass members after their first purchase. If they're already a Game Pass member, they can easily gift it to a friend to play together.

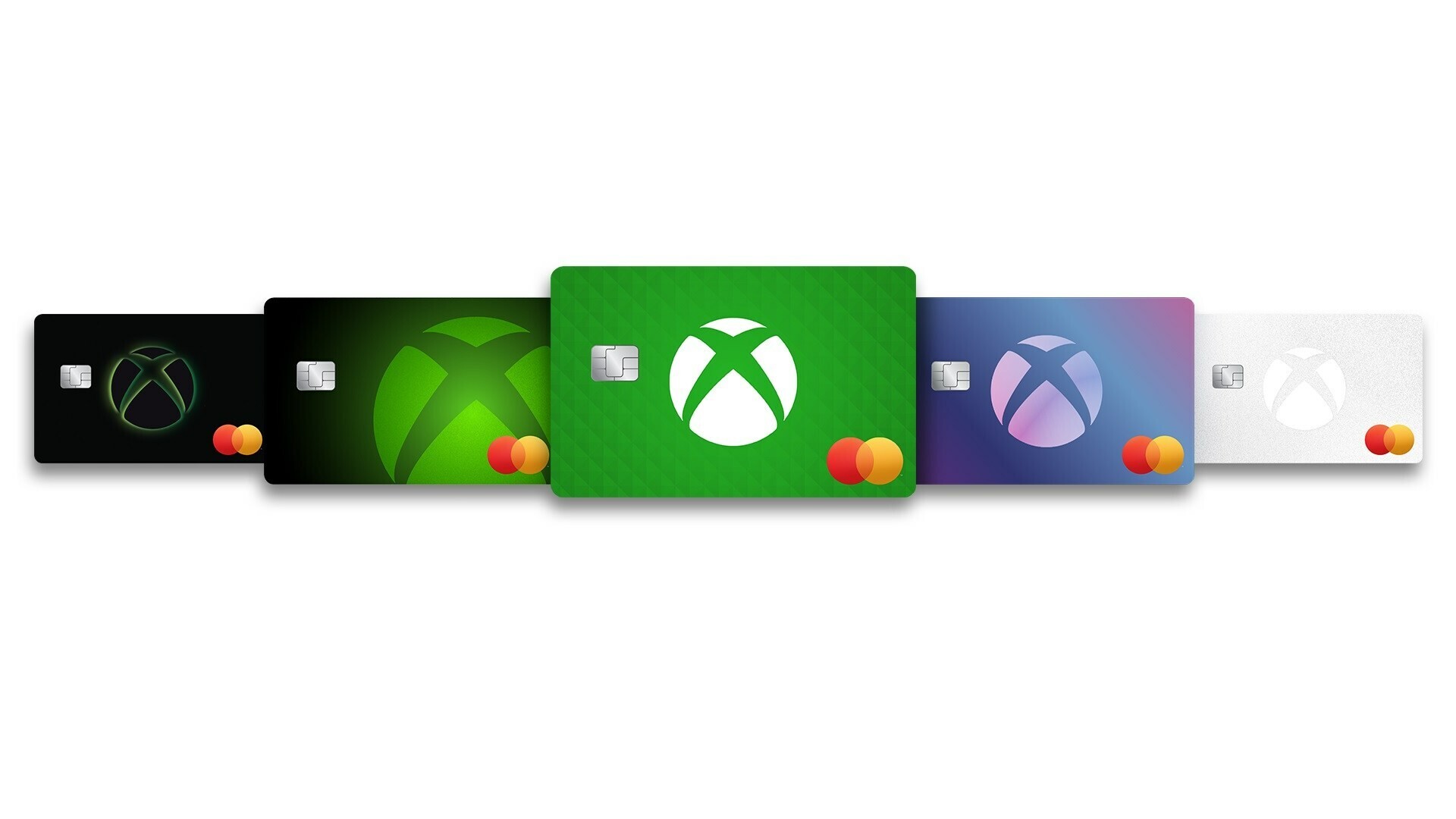

- Choice of one of five iconic designs for their card, with the option of personalizing it with their gamertag.

- Flexibility of use with contactless payments and digital wallets.

- Free online access to cardmembers' FICO Credit Score, which allows users to keep an eye on their credit score and receive alerts when their score has changed.

- $0 Fraud Liability protection, so cardmembers are not responsible for charges they didn't authorize.

Application details can be viewed here. If you're an Xbox Insider with residence in the continental United States, Alaska, or Hawaii, you can apply starting on September 21. The Xbox Mastercard will be available in waves to Xbox Insiders throughout this fall.

12 Comments on Microsoft Introduces Xbox Mastercard - Outlines Perks for Gamers

I have enough credit cards, and I'd rather get the travel bonuses or just do cashback for you know...anything I want.

The bank still didn't trust me, so I only got a sub $1,600 credit limit...

Personal credit cards are heavily controlled by the active jurisdiction so Americans can't apply for credit cards from other countries (there might be a few exceptions but none significant).

There are many people across the planet who would love to get an Apple Card but aren't eligible because they don't live in the USA because it is issued by Goldman Sachs Bank USA (Salt Lake City, UT).

Used to be a Barclays customer in the UK, they suck, more so than most banks.

Yeah, I'm aware of that too, lots of peculiar legal issues.

I prefer to avoid credit cards when possible, but alas, in Sweden cash is not even accepted by many stores and restaurants, so paying by card or a weird local phone based payment service are the main options.

Does that make Apple's cards religious or just conservative?

There is obviously more risk in consumer lending to people who don't have a good chance to repay their debts on time. The American consumer lending industry feeds on people who won't pay off their credit cards every month but carry a balance and thus generate finance charges. Those finance charges (along with merchant transaction fees) fund these benefits as well as all of the fancy services, apps, etc.

Credit cards are convenient and if there's anything Americans love, it's fast convenience.

Of course, the better credit cards here in the USA require a better credit record from the applicant. Young people who have recently joined the workforce often are turned down from the best credit cards. In the worst cases, they have to get a secured credit card which basically requires a deposit (like $500 for a card with a $500 limit) just so you can develop a positive credit history. People who declare bankruptcy often have to rebuild their credit with secured cards and loans. Even when they do get accepted for an unsecured card, it's usually at a much lower credit limit and higher interest rate than others with a solid established credit history. I believe the US consumer credit interest rates are pretty high compared to many other places.

I haven't looked at the fine print for the Xbox Mastercard offering but I wouldn't be surprised if it were targeted at young consumers who are just starting out building their credit. This doesn't look like the type of financial instrument that a consumer with 20+ years of credit history would really benefit much from. People are at different stages in their lives and this is probably an appealing offering to some.

It's worth pointing out that branded credit cards are very commonplace here in the USA. Many stores have their own (like Amazon) and even the major sports leagues usually have some sort of branded card program.

I know someone that, when AmEx's Serve was partnered with League of Legends, he got their debit card. He would would transfer money to the LoL Serve card and then use the card to pay his mortgage, car payments and so on. For a while, when you used that card you would earn 1 RP (Riot Point) for every 1 dollar spent. Serve and LoL stopped the feature years ago (upon looking it up, appears it was stopped December 1st, 2014) and he still has thousands of RPs for LoL.

We don't play LoL much anymore, but every Christmas he still goes out and gifts a handful of skins to everyone on his friend's list since he doesn't use the points for anything else.

Only thing I do is I use my AmEx credit card to pay for groceries. I then pay off the balance at the end of the month. AmEx gives 3% cash back, up to $6,000 on groceries. Once I hit that $6,000 limit I stop using it for the year after I take advantage of the $180 I've built up. 3 years ago $180 used to be the average grocery bill for me about every 11 days. $6000 limit usually came right around the start of December. These days $280 is the average grocery bill every 11 days so that $6000 limit gets reached by August.

On a 1% cashback purchase, if you spend $100 you get $1 back. On MS, you get 100 points. As a current Level 2 Rewards member, 910 points = $1. So spending $100 I would basically get just 10 cents.

Points are annoying because it has hard to put a real hard cash value on it. For example, I am a Hilton Honors member. I just spent 58,000 points. There were 4 hotels all $235/night. One Hotel wanted 80k points a night, while the cheapest Hotel was 55k points a night. They get to use points as funny money and charge you basically whatever they want with points. Very easy way to dramatically lower the actual cash value.

And then establish a convoluted points scheme to make customers think they get more than they actually do.

Isn't that getting old?

As I mentioned earlier, there are people at various points in their lives. This particular credit card's primary target audience is the 18-24 age bracket followed by the 25-29 bracket.

By the time many people reach their 30s, they have different priorities like raising a family or setting up a house so credit card benefits will swing to other categories. Microsoft Store points aren't going to fill up your shopping cart with baby food, diapers, or new rugs. Older people have homes that are pretty well furnished so they'll end up going for more travel-related perks like cards with no foreign transaction fees or airport lounge access.

When I'm standing in line at a supermarket or big box store, I often see people pull out wallets with 15-20 credit cards (or have that many in the phone's e-wallet), each one for a particular situation. I probably have 7-8 credit cards but use only two or three in my regular rotation, the rest stay in an drawer in my home office. I have two that have no foreign transaction fees so those come out when I travel internationally.

I don't own the exact same cards I had 20 years ago. It's okay to change them up occasionally. They're just financial instruments that are there for a individual's convenience. I certainly don't have any interest in most of them.

Remember that there is no one single credit card that is perfect for everyone everywhere in all situations. Americans are fortunate to have a wide variety of consumer cards to select from. I don't really care if someone uses an Xbox Mastercard to pay for their next Doordash delivery to get 3 percent off. After all another Xbox cardholder who is paying 22% interest is underwriting that bennie, not me.

You are free in most situations to pay with cash, a check, debit card, or some crap credit card that offers almost zero benefits. But let's be real, in the USA in 2023 you really need a credit card to develop a good credit history which is increasingly important for things like good insurance rates, auto rental, consumer purchase protection and even things like renting an apartment or applying for a job. You'll want excellent credit once you buy real estate to get better mortgage rates. This can provide savings of tens of thousands of dollars of mortgage interest over the long term.

This is disgusting pure and simple. The only thing worse is payment processors recent clamp down on generated disposable cards, this seems like a second part of that: tie in your xbox subscription to your xbox card that you'll never be able to cancel.