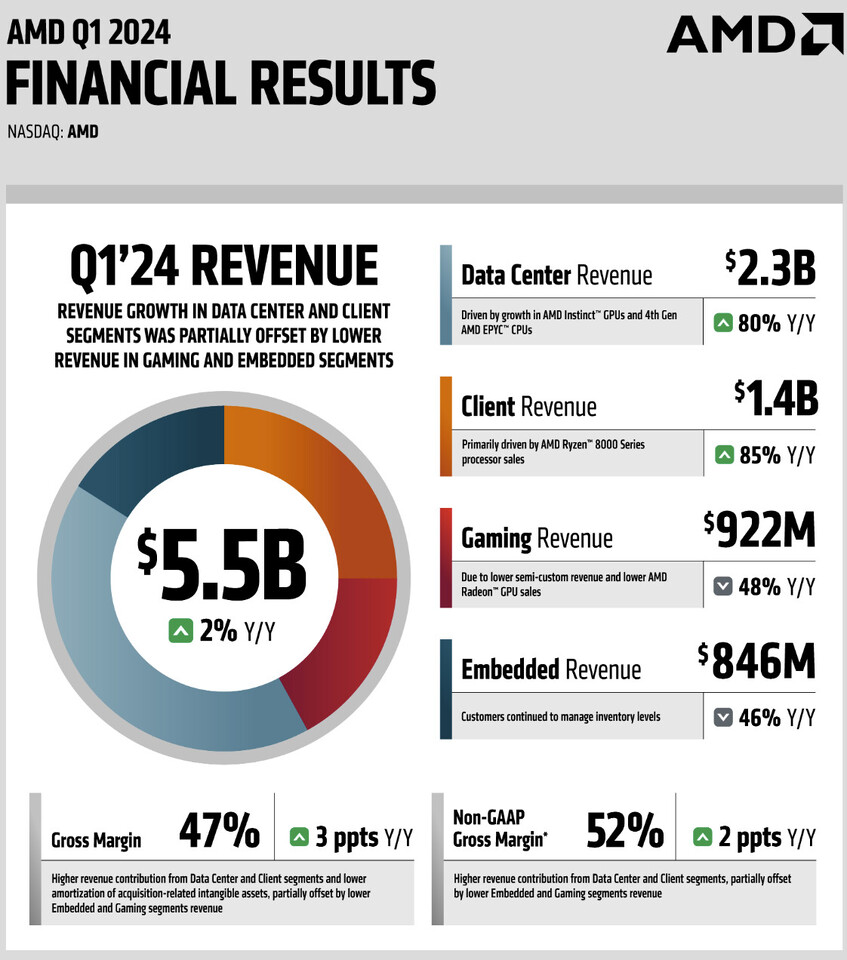

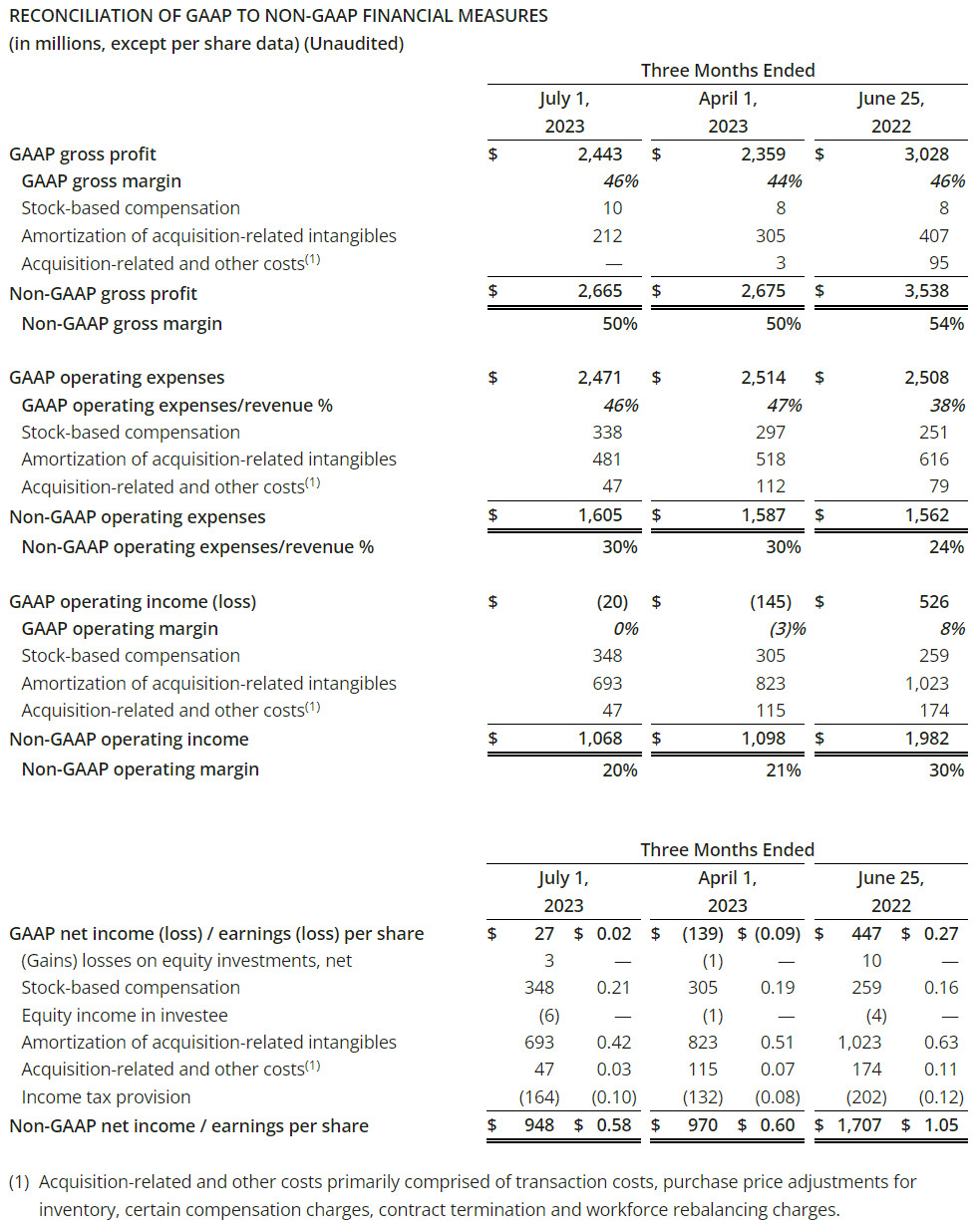

AMD Reports First Quarter 2024 Financial Results

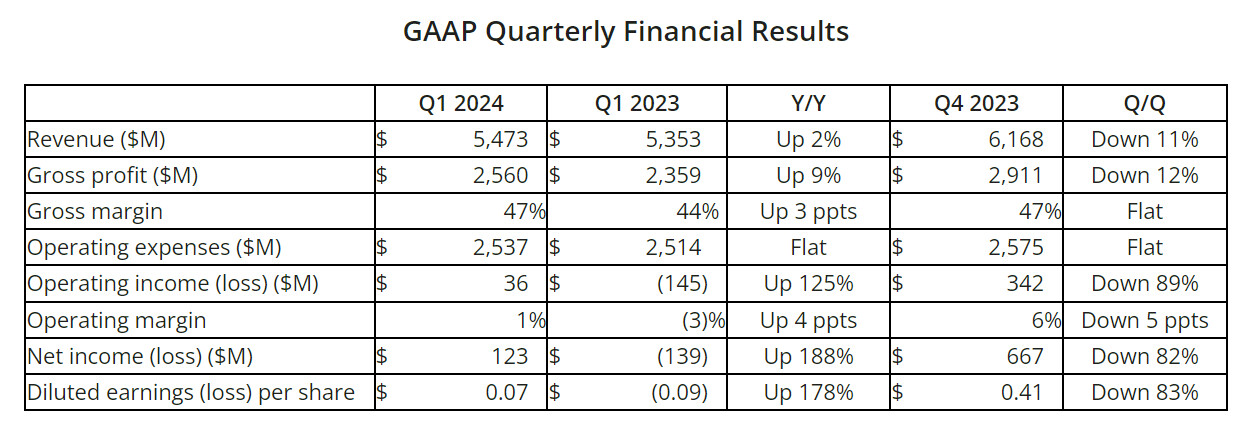

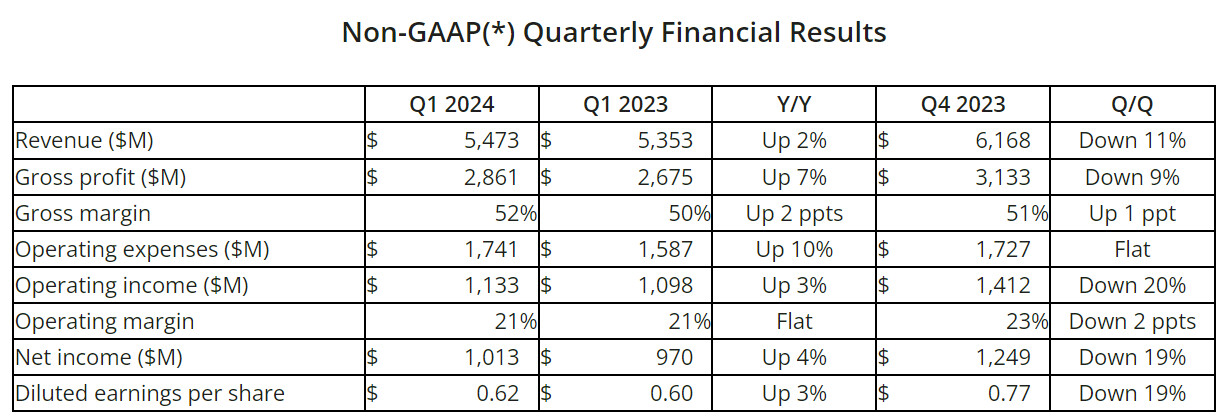

AMD (NASDAQ:AMD) today announced revenue for the first quarter of 2024 of $5.5 billion, gross margin of 47%, operating income of $36 million, net income of $123 million and diluted earnings per share of $0.07. On a non-GAAP basis, gross margin was 52%, operating income was $1.1 billion, net income was $1.0 billion and diluted earnings per share was $0.62.

"We delivered strong first quarter results with our Data Center and Client segments each growing more than 80% year-over-year driven by the ramp of MI300 AI accelerator shipments and the adoption of our Ryzen and EPYC processors," said AMD Chair and CEO Dr. Lisa Su. "This is an incredibly exciting time for the industry as widespread deployment of AI is driving demand for significantly more compute across a broad range of markets. We are executing very well as we ramp our data center business and enable AI capabilities across our product portfolio."

"We delivered strong first quarter results with our Data Center and Client segments each growing more than 80% year-over-year driven by the ramp of MI300 AI accelerator shipments and the adoption of our Ryzen and EPYC processors," said AMD Chair and CEO Dr. Lisa Su. "This is an incredibly exciting time for the industry as widespread deployment of AI is driving demand for significantly more compute across a broad range of markets. We are executing very well as we ramp our data center business and enable AI capabilities across our product portfolio."