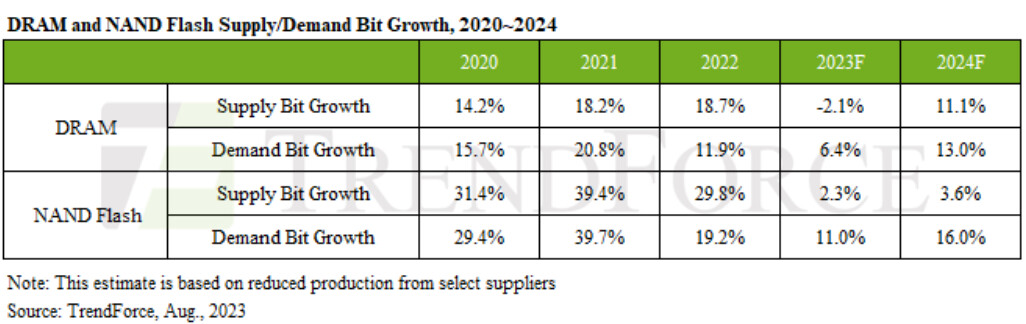

After a Low Base Year in 2023, DRAM and NAND Flash Bit Demand Expected to Increase by 13% and 16% Respectively in 2024

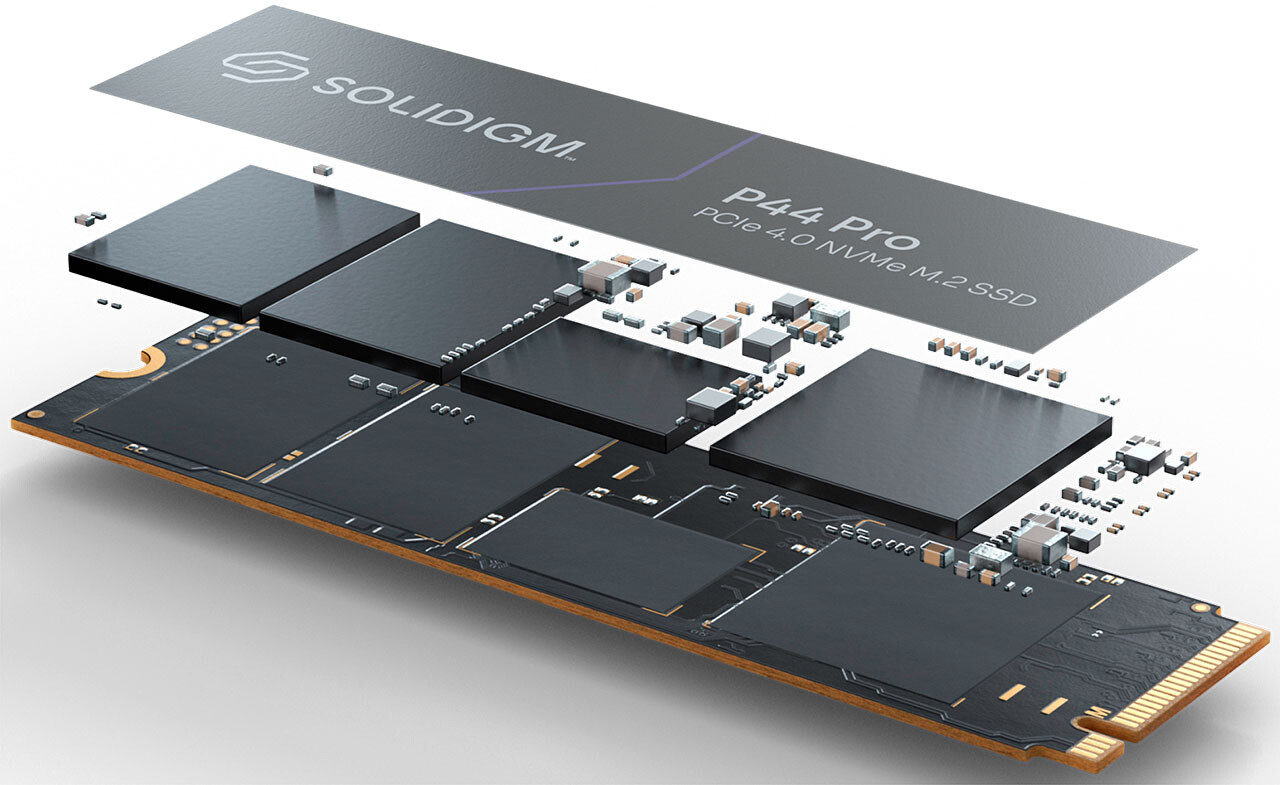

TrendForce expects that memory suppliers will continue their strategy of scaling back production of both DRAM and NAND Flash in 2024, with the cutback being particularly pronounced in the financially struggling NAND Flash sector. Market demand visibility for consumer electronic is projected to remain uncertain in 1H24. Additionally, capital expenditure for general-purpose servers is expected to be weakened due to competition from AI servers. Considering the low baseline set in 2023 and the current low pricing for some memory products, TrendForce anticipates YoY bit demand growth rates for DRAM and NAND Flash to be 13% and 16%, respectively. Nonetheless, achieving effective inventory reduction and restoring supply-demand balance next year will largely hinge on suppliers' ability to exercise restraint in their production capacities. If managed effectively, this could open up an opportunity for a rebound in average memory prices.

PC: The annual growth rate for average DRAM capacity is projected at approximately 12.4%, driven mainly by Intel's new Meteor Lake CPUs coming into mass production in 2024. This platform's DDR5 and LPDDR5 exclusivity will likely make DDR5 the new mainstream, surpassing DDR4 in the latter half of 2024. The growth rate in PC client SSDs will not be as robust as that of PC DRAM, with just an estimated growth of 8-10%. As consumer behavior increasingly shifts toward cloud-based solutions, the demand for laptops with large storage capacities is decreasing. Even though 1 TB models are becoming more available, 512 GB remains the predominant storage option. Furthermore, memory suppliers are maintaining price stability by significantly reducing production. Should prices hit rock bottom and subsequently rebound, PC OEMs are expected to face elevated SSD costs. This, when combined with Windows increasing its licensing fees for storage capacities at and above 1 TB, is likely to put a damper on further growth in average storage capacities.

PC: The annual growth rate for average DRAM capacity is projected at approximately 12.4%, driven mainly by Intel's new Meteor Lake CPUs coming into mass production in 2024. This platform's DDR5 and LPDDR5 exclusivity will likely make DDR5 the new mainstream, surpassing DDR4 in the latter half of 2024. The growth rate in PC client SSDs will not be as robust as that of PC DRAM, with just an estimated growth of 8-10%. As consumer behavior increasingly shifts toward cloud-based solutions, the demand for laptops with large storage capacities is decreasing. Even though 1 TB models are becoming more available, 512 GB remains the predominant storage option. Furthermore, memory suppliers are maintaining price stability by significantly reducing production. Should prices hit rock bottom and subsequently rebound, PC OEMs are expected to face elevated SSD costs. This, when combined with Windows increasing its licensing fees for storage capacities at and above 1 TB, is likely to put a damper on further growth in average storage capacities.