PC Shipments Expected to Fall by -3.7% in 2014, According to IDC

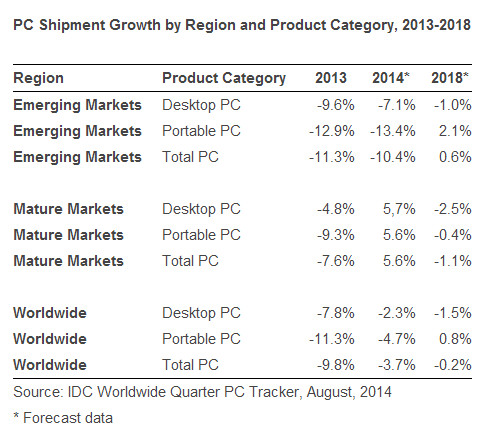

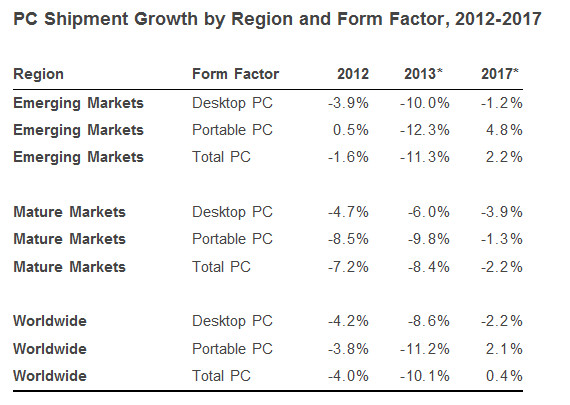

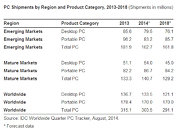

Worldwide PC shipments are expected to fall by -3.7% in 2014, an improvement from the previous forecast of -6%, according to the International Data Corporation (IDC) Worldwide Quarterly PC Tracker. PC shipments in emerging regions remain constrained by ongoing competition from alternative devices and a number of economic/political challenges. However, commercial demand and even a rekindling of consumer interest in mature markets helped to boost results for the first half of 2014 as well as the outlook for the rest of the year.

PC shipments in mature regions are now projected to grow by 5.6% in 2014 - the highest since 2010 - with both consumer and commercial segments showing positive growth. On the other hand, the outlook for emerging market has been lowered slightly to reflect reduced stability and economic conditions in Asia/Pacific, Latin America, and Central Europe, the Middle East and Africa (CEMA).

PC shipments in mature regions are now projected to grow by 5.6% in 2014 - the highest since 2010 - with both consumer and commercial segments showing positive growth. On the other hand, the outlook for emerging market has been lowered slightly to reflect reduced stability and economic conditions in Asia/Pacific, Latin America, and Central Europe, the Middle East and Africa (CEMA).