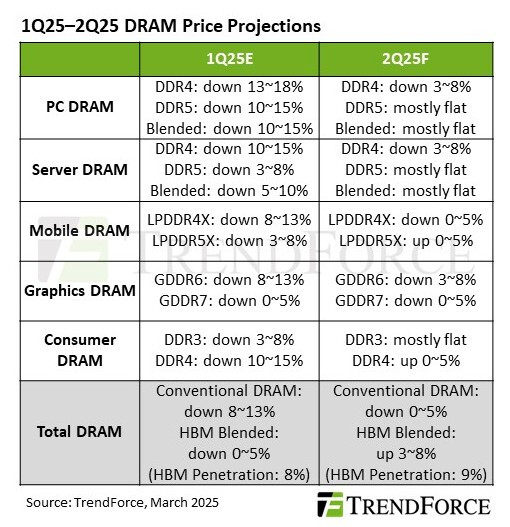

Rising Demand and EOL Plans from Suppliers Drive Strong DDR4 Contract Price Hikes in 2Q25 for Server and PC Markets

TrendForce's latest investigations find that DDR4 contract prices for servers and PCs are expected to rise more sharply in the second quarter of 2025 due to two key factors: major DRAM suppliers scaling back DDR4 production and buyers accelerating procurement ahead of U.S. tariff changes. As a result, server DDR4 contract prices are forecast to rise by 18-23% QoQ, while PC DDR4 prices are projected to increase by 13-18%—both surpassing earlier estimates.

TrendForce notes that DDR4 has been in the market for over a decade, and demand is increasingly shifting toward DDR5. Given the significantly higher profit margins for HBM, DDR5, and LPDDR5(X), suppliers have laid out EOL plans for DDR4, with final shipments expected by early 2026. Current EOL notifications largely target server and PC clients, while consumer DRAM (mainly DDR4) remains in production due to continued mainstream demand.

TrendForce notes that DDR4 has been in the market for over a decade, and demand is increasingly shifting toward DDR5. Given the significantly higher profit margins for HBM, DDR5, and LPDDR5(X), suppliers have laid out EOL plans for DDR4, with final shipments expected by early 2026. Current EOL notifications largely target server and PC clients, while consumer DRAM (mainly DDR4) remains in production due to continued mainstream demand.