Apr 16th, 2025 10:08 EDT

change timezone

Latest GPU Drivers

New Forum Posts

- The TPU UK Clubhouse (26117)

- 5070ti overclock...what are your settings? (6)

- Help me identify Chip of this DDR4 RAM (21)

- Last game you purchased? (772)

- Windows 11 fresh install to do list (23)

- How to relubricate a fan and/or service a troublesome/noisy fan. (229)

- GPU Memory Temprature is always high (16)

- Help For XFX RX 590 GME Chinese - Vbios (4)

- PCGH: "hidden site" to see total money spend on steam (3)

- Share your AIDA 64 cache and memory benchmark here (3053)

Popular Reviews

- G.SKILL Trident Z5 NEO RGB DDR5-6000 32 GB CL26 Review - AMD EXPO

- ASUS GeForce RTX 5080 TUF OC Review

- DAREU A950 Wing Review

- The Last Of Us Part 2 Performance Benchmark Review - 30 GPUs Compared

- Sapphire Radeon RX 9070 XT Pulse Review

- Sapphire Radeon RX 9070 XT Nitro+ Review - Beating NVIDIA

- Upcoming Hardware Launches 2025 (Updated Apr 2025)

- Thermaltake TR100 Review

- Zotac GeForce RTX 5070 Ti Amp Extreme Review

- TerraMaster F8 SSD Plus Review - Compact and quiet

Controversial News Posts

- NVIDIA GeForce RTX 5060 Ti 16 GB SKU Likely Launching at $499, According to Supply Chain Leak (182)

- NVIDIA Sends MSRP Numbers to Partners: GeForce RTX 5060 Ti 8 GB at $379, RTX 5060 Ti 16 GB at $429 (124)

- Nintendo Confirms That Switch 2 Joy-Cons Will Not Utilize Hall Effect Stick Technology (105)

- Over 200,000 Sold Radeon RX 9070 and RX 9070 XT GPUs? AMD Says No Number was Given (100)

- Nintendo Switch 2 Launches June 5 at $449.99 with New Hardware and Games (99)

- Sony Increases the PS5 Pricing in EMEA and ANZ by Around 25 Percent (85)

- NVIDIA PhysX and Flow Made Fully Open-Source (77)

- NVIDIA Pushes GeForce RTX 5060 Ti Launch to Mid-April, RTX 5060 to May (77)

News Posts matching #market

Return to Keyword Browsing

NVIDIA Confirms Verified Priority Access Program for GeForce RTX 50 Series is Alive

NVIDIA has confirmed that its Verified Priority Access (VPA) program for the GeForce RTX 50 Series remains active following its initial announcement two months ago. The program allows a limited number of US-based GeForce account holders to purchase RTX 5090 and RTX 5080 Founders Edition cards directly from the NVIDIA Marketplace. The VPA scheme was introduced three weeks after the RTX 50 Series launch to address supply shortages and high reseller prices. Initially, two months ago, users with NVIDIA Accounts created on or before January 30, 2025, at 6 AM Pacific Time, could register their interest through an online form. Invitations would have been emailed to qualifying account holders, with the first notifications scheduled for next week.

This pilot program applies only to US GeForce users and is limited to the RTX 5090, RTX 5080, and RTX 5070 Founders Edition cards. The recently released RTX 5070 Ti is not included and must be purchased through AIB partner custom designs. NVIDIA has not disclosed how many priority access slots are available or whether the program will expand internationally. All we know is that an NVIDIA representative on Reddit posted, "VPA for the GeForce RTX 50 series Founders Edition graphics cards has not ended," responding to an alleged VPA program rumor that it has ended. If the US pilot is successful, the company may consider adding more markets and product lines. Eligible users should watch their inboxes for an invitation to buy at the original MSRP.

This pilot program applies only to US GeForce users and is limited to the RTX 5090, RTX 5080, and RTX 5070 Founders Edition cards. The recently released RTX 5070 Ti is not included and must be purchased through AIB partner custom designs. NVIDIA has not disclosed how many priority access slots are available or whether the program will expand internationally. All we know is that an NVIDIA representative on Reddit posted, "VPA for the GeForce RTX 50 series Founders Edition graphics cards has not ended," responding to an alleged VPA program rumor that it has ended. If the US pilot is successful, the company may consider adding more markets and product lines. Eligible users should watch their inboxes for an invitation to buy at the original MSRP.

Intel Refreshes its Iconic Brand Motto - Introduces: "That's the Power of Intel Inside "

Intel introduced its new brand to the world Tuesday at the Intel Vision 2025 event in Las Vegas. Leading with "That's the power of Intel Inside," Intel leans into the essential role the company—along with its partners and customers—plays in the world while giving a nod to the company's wildly popular "Intel Inside" campaign of the 1990s.

Brett Hannath, chief marketing officer for Intel, says the new brand platform anchors on the idea that "Intel ignites the greatness within"—in every employee, customer, consumer, community, partner. All the while, it allows Intel to reflect on its proud heritage. (The Intel Inside co-marketing campaign launched in 1991 helped Intel become a household name around the globe over the next decade.) More than a marketing initiative, "That's the power of Intel Inside" is an avenue for amplifying Intel's importance in today's world. Intel's leaders plan to leverage the new brand platform to drive differentiation, revenue growth, and equity with customers and partners.

Brett Hannath, chief marketing officer for Intel, says the new brand platform anchors on the idea that "Intel ignites the greatness within"—in every employee, customer, consumer, community, partner. All the while, it allows Intel to reflect on its proud heritage. (The Intel Inside co-marketing campaign launched in 1991 helped Intel become a household name around the globe over the next decade.) More than a marketing initiative, "That's the power of Intel Inside" is an avenue for amplifying Intel's importance in today's world. Intel's leaders plan to leverage the new brand platform to drive differentiation, revenue growth, and equity with customers and partners.

Trump Tariffs to Hike PC Costs at Least 20%, System Integrators Take the Biggest Blow

While semiconductors are exempt (for now at least) from Trump's tariffs, other components going into our PCs are not. According to Tom's Hardware, which spoke to multiple system integrators, tariffs are about to hike PC costs by at least 20%, with system integrators hurt the most. The tariff package imposes a 54% rate on Chinese goods, 34% on top of earlier tariffs, and significant duties on Taiwan, South Korea, and Vietnam products. These countries supply essential PC components such as SSDs, RAM, cases, and graphics cards. Wallace Santos, CEO of Maingear, highlighted the immediate effects on production: "Tariffs have a direct impact on our cost structure… which we have to pass down to our customers." He further explained that some suppliers have halted production in China, leading to scarcity and escalating costs. Santos estimates that prices for his PCs will rise "20 to 25% as a result of the tariffs."

Other company leaders express concern over the limited alternatives available. Kelt Reeves, CEO of Falcon Northwest, stated, "Sadly the overwhelming majority of PC component manufacturing is not done in the US and never has been. There's no US alternative supplier for most PC parts." Reeves added that even US-based system integrators are "facing skyrocketing costs" due to the tariffs, which are set to worsen an already challenging market situation caused by ongoing GPU shortages. Jon Bach, CEO of Puget Systems, shared his perspective in a recent blog post, noting that his company might absorb some costs to minimize consumer price increases. However, even before the latest tariff updates, Bach predicted a price rise of "20 to 45 percent by June." Critics of the tariffs warn of broader economic issues. Gary Shapiro, CEO of the Consumer Technology Association, condemned the policy as "massive tax hikes on Americans that will drive inflation, kill jobs on Main Street, and may cause a recession for the US economy." With these tariffs taking effect, the PC industry faces a period of adjustment marked by increased costs and significant supply chain challenges.

Other company leaders express concern over the limited alternatives available. Kelt Reeves, CEO of Falcon Northwest, stated, "Sadly the overwhelming majority of PC component manufacturing is not done in the US and never has been. There's no US alternative supplier for most PC parts." Reeves added that even US-based system integrators are "facing skyrocketing costs" due to the tariffs, which are set to worsen an already challenging market situation caused by ongoing GPU shortages. Jon Bach, CEO of Puget Systems, shared his perspective in a recent blog post, noting that his company might absorb some costs to minimize consumer price increases. However, even before the latest tariff updates, Bach predicted a price rise of "20 to 45 percent by June." Critics of the tariffs warn of broader economic issues. Gary Shapiro, CEO of the Consumer Technology Association, condemned the policy as "massive tax hikes on Americans that will drive inflation, kill jobs on Main Street, and may cause a recession for the US economy." With these tariffs taking effect, the PC industry faces a period of adjustment marked by increased costs and significant supply chain challenges.

Ubisoft Creates New Subsidiary With Tencent for Top 3 AAA Game Franchises

After many rumors and supposed leaks claimed that Tencent was preparing a buyout of Ubisoft, it seems as though an alternative solution was reached, with Ubisoft today announcing that it has created a new subsidiary to house some of its biggest gaming franchises. According to the announcement, the new business entity is "based on its Assassin's Creed, Far Cry, and Tom Clancy's Rainbow Six brands," and it received initial funding from Tencent, which owns a 25% stake in the new business. Tencent's investment in the new subsidiary is to the tune of €1.16 billion.

The announcement also gives us an indication of what to expect from these game franchises going forward. For starters, Ubisoft mentions that the new subsidiary—and likely the capital injection from the Tencent investment—is part of a new business model that would allow it to invest more in increasing the quality of its creative outputs. Supposedly, it will focus on quality story-driven solo games and growing its multiplayer offerings with more frequent content updates, more social features, and introducing "free-to-play touchpoints." The acquisition comes after a series of delays marred the lead-up to the launch of the latest Assassin's Creed Shadows, which ultimately seems to have been a commercial success. In keeping with other trends, Ubisoft mentions in the press release that the move to split off these gaming IPs will also help accelerate its recent moves to make these gaming franchises multi-platform. Recently, Ubisoft has repeatedly stated that its strategy moving forward would include more multi-platform day-one launches, as opposed to console exclusives and timed exclusives.

The announcement also gives us an indication of what to expect from these game franchises going forward. For starters, Ubisoft mentions that the new subsidiary—and likely the capital injection from the Tencent investment—is part of a new business model that would allow it to invest more in increasing the quality of its creative outputs. Supposedly, it will focus on quality story-driven solo games and growing its multiplayer offerings with more frequent content updates, more social features, and introducing "free-to-play touchpoints." The acquisition comes after a series of delays marred the lead-up to the launch of the latest Assassin's Creed Shadows, which ultimately seems to have been a commercial success. In keeping with other trends, Ubisoft mentions in the press release that the move to split off these gaming IPs will also help accelerate its recent moves to make these gaming franchises multi-platform. Recently, Ubisoft has repeatedly stated that its strategy moving forward would include more multi-platform day-one launches, as opposed to console exclusives and timed exclusives.

ZOTAC US Store Hikes Up GeForce RTX 5090 Pricing Again - SOLID OC Now $2700, Flagship Hits $3000 Mark

ASUS and MSI's price hiking of GeForce RTX 50-series graphics cards is already a well explored subject matter (news-wise), but GPU market watchdogs have spent time investigating circumstances further down from the perch of NVIDIA's most visible board partner players. Citing evidence presented on the official Team Green subreddit, VideoCardz has levelled criticism in ZOTAC's direction. Apparently, the brand's North American store has—quite recently—jacked up asking prices for its custom GeForce RTX 5090 designs. The Hong Kong-based manufacturer only offers a choice of two models via its US webstore: SOLID OC and AMP Extreme INFINITY. At the time of writing, ZOTAC's webshop is undergoing "construction work"—fortunately, screenshots and crucial points of info were preserved by Redditors and media outlets. The flagship AMP Extreme INFINITY SKU has hit an unprecedented $2999.99 price point, although not reaching the heights of ASUS Astral ($3359.99!). A mid-March Wayback Machine save state reveals a previous RTX 5090 AMP Extreme INFINITY listing at $2599.99, but its initial launch price was $2499.99. Naturally, a flagship design—comprised of a robust cooling solution, fancy features/accessories and ARGB lighting—demands a premium upcharge, but ZOTAC's top-tier SKU is priced $1001 above Team Green's $1999 MSRP baseline.

ZOTAC's GeForce RTX 5090 SOLID (non-OC) SKU was supposed to act as the "barebones" baseline MSRP-conformant model, but price watchers noted that ZOTAC USA had removed this entry from the official webstore. Tom's Hardware reckons that the last recorded cost of ownership was $2199.99. ZOTAC's next best option is the brand's factory-overclocked variant—GeForce RTX 5090 SOLID OC—now adjusted up to $2699.99. Launch pricing was somewhere just above $2200, but that figure has changed over time. It was $2369.99, prior to this week—according to a Wayback Machine archived state. As reported last month, ZOTAC rolled out a "Priority Access Campaign" via Discord—this anti-scalping strategy received praise upon initiation, but VideoCardz's watchful eye has kept track of very few successful transactions. According to their latest investigative piece, a "top secret" ZOTAC Discord group was formed—this separate elite member-focused channel offers even "easier access" to coveted cutting-edge gaming graphics card.

ZOTAC's GeForce RTX 5090 SOLID (non-OC) SKU was supposed to act as the "barebones" baseline MSRP-conformant model, but price watchers noted that ZOTAC USA had removed this entry from the official webstore. Tom's Hardware reckons that the last recorded cost of ownership was $2199.99. ZOTAC's next best option is the brand's factory-overclocked variant—GeForce RTX 5090 SOLID OC—now adjusted up to $2699.99. Launch pricing was somewhere just above $2200, but that figure has changed over time. It was $2369.99, prior to this week—according to a Wayback Machine archived state. As reported last month, ZOTAC rolled out a "Priority Access Campaign" via Discord—this anti-scalping strategy received praise upon initiation, but VideoCardz's watchful eye has kept track of very few successful transactions. According to their latest investigative piece, a "top secret" ZOTAC Discord group was formed—this separate elite member-focused channel offers even "easier access" to coveted cutting-edge gaming graphics card.

China Leads as Global Semiconductor Fab Investment Expected to Reach $110B in 2025

Global fab equipment spending for front-end facilities in 2025 is anticipated to increase by 2% year-over-year (YoY) to $110 billion, marking the sixth consecutive year of growth since 2020, SEMI announced today in its latest quarterly World Fab Forecast report.

Fab equipment spending is projected to rise by 18% in the following year, reaching $130 billion. This growth in investment is driven not only by demand in the high-performance computing (HPC) and memory sectors to support data center expansions, but also by the increasing integration of artificial intelligence (AI), which is driving up the silicon content required for edge devices.

Fab equipment spending is projected to rise by 18% in the following year, reaching $130 billion. This growth in investment is driven not only by demand in the high-performance computing (HPC) and memory sectors to support data center expansions, but also by the increasing integration of artificial intelligence (AI), which is driving up the silicon content required for edge devices.

NAND Flash Prices Begin to Recover in 2Q25 as Production Cuts and Inventory Rebuilding Take Effect

TrendForce reports that NAND Flash suppliers began reducing production in the fourth quarter of 2024, and the effects are now starting to show. In anticipation of potential U.S. tariff increases, consumer electronics brands have accelerated production, further driving up demand. Concurrently, inventory restocking is underway across the PC, smartphone, and data center sectors. As a result, NAND Flash prices are expected to stabilize in the second quarter of 2025, with prices for wafers and client SSDs projected to rise.

Client SSD prices to rise 3-8% while enterprise SSD prices to remain flat

After three consecutive quarters of inventory depletion, client SSD demand is rebounding as OEMs resume production early. The upcoming end of Windows 10 support and the launch of new-generation CPUs are expected to drive replacement demand for PCs. Meanwhile, the DeepSeek effect is accelerating the adoption of edge AI, further fueling client SSD demand. With production cuts and supply adjustments gradually restoring balance, client SSD contract prices are projected to rise 3% to 8% QoQ in Q2.

Client SSD prices to rise 3-8% while enterprise SSD prices to remain flat

After three consecutive quarters of inventory depletion, client SSD demand is rebounding as OEMs resume production early. The upcoming end of Windows 10 support and the launch of new-generation CPUs are expected to drive replacement demand for PCs. Meanwhile, the DeepSeek effect is accelerating the adoption of edge AI, further fueling client SSD demand. With production cuts and supply adjustments gradually restoring balance, client SSD contract prices are projected to rise 3% to 8% QoQ in Q2.

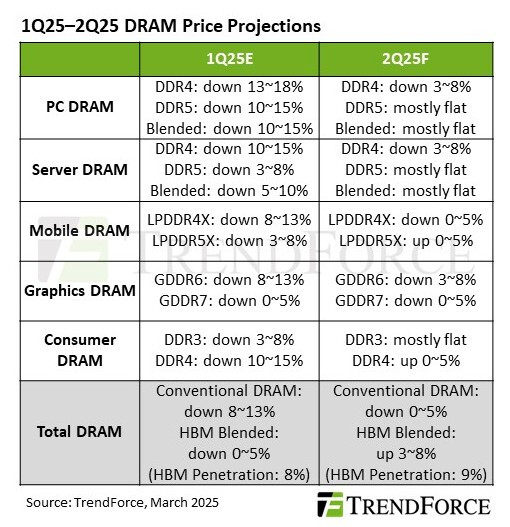

Downstream Inventory Reduction Eases DRAM Price Decline in 2Q25

TrendForce's latest findings reveal that U.S. tariff hikes prompted most downstream brands to frontload shipments to 1Q25, accelerating inventory reduction across the memory supply chain. Looking ahead to the second quarter, conventional DRAM prices are expected to decline by just 0-5% QoQ, while average DRAM pricing including HBM is forecast to rise by 3-8%, driven by increasing shipments of HBM3e 12hi.

PC and server DRAM prices to hold steady

In response to potential U.S. tariff hikes, major PC OEMs are requesting ODMs to increase production, accelerating DRAM depletion in their inventories. OEMs with lower inventory levels may raise procurement from suppliers in Q2 to ensure stable DRAM supply for the second half of 2025.

PC and server DRAM prices to hold steady

In response to potential U.S. tariff hikes, major PC OEMs are requesting ODMs to increase production, accelerating DRAM depletion in their inventories. OEMs with lower inventory levels may raise procurement from suppliers in Q2 to ensure stable DRAM supply for the second half of 2025.

Xbox Opens Doors to a Billion Players - Xbox App Mockup Hints at Steam Library Detection

At Xbox, our mission is clear: bring the joy and community of gaming to everyone on the planet. We believe that gamers should be able to play the games they want, with the people they want, anywhere they want. Central to this vision is empowering game creators to deliver exceptional content across all platforms seamlessly. Our goal is simple: to make every screen in the world an Xbox.

Since the original Xbox debuted as the first game console equipped with a built-in hard drive, this kernel of innovation has been at the core of our identity. With Xbox Live, we reshaped multiplayer gaming, establishing an industry standard for online connectivity, community building, and digital distribution. Furthering our commitment to accessibility and choice, Xbox Game Pass introduced a subscription model that redefined how players discover and engage with games, creating new opportunities for developers to connect with audiences worldwide. Since our earliest explorations in the console space, we're proud to have led the way in ensuring that hardware and services can best meet the changing needs of the gaming audience.

Since the original Xbox debuted as the first game console equipped with a built-in hard drive, this kernel of innovation has been at the core of our identity. With Xbox Live, we reshaped multiplayer gaming, establishing an industry standard for online connectivity, community building, and digital distribution. Furthering our commitment to accessibility and choice, Xbox Game Pass introduced a subscription model that redefined how players discover and engage with games, creating new opportunities for developers to connect with audiences worldwide. Since our earliest explorations in the console space, we're proud to have led the way in ensuring that hardware and services can best meet the changing needs of the gaming audience.

Yeston Predicts Stabilization of Radeon RX 9070 Series Supply After April

Coverage of Radeon RX 9070 XT and RX 9070 launch batches has mainly focused on Western market conditions, with little insight into goings-on in China. AMD and board partners held a special RDNA 4 kick-off event in Beijing at the end of February, roughly twelve hours in advance of their international presentation. According to VideoCardz, initial supplies of Yeston's Sakura and Sakura Atlantis graphics cards were snapped up quickly by regional customers. The Chinese AIB specializes in brightly-hued shroud and backplate designs, often decorated with "waifu" illustrations and miscellaneous cute graphics. Unfortunately, interested parties from abroad are limited to importing from local retail platforms.

Yeston's social media accounts have alerted potential customers to re-stocks and connected developments—their latest bulletin hints about an improved situation, following another swift depletion of refreshed stock: "hello everyone! Thank you for the support! We have received a lot of messages and would love to inform you now the supply is unstable, but we will restock every week. Please don't be frustrated if you didn't get it. The supply will become stable and continue to be available after April." Interestingly, this morning's message did not touch upon the controversial topic of price hikes. At launch, Yeston's latest Navi 48 GPU-based offerings conformed or floated just above Team Red baseline MSRP (including VAT)—4999 RMB (~$686 USD) for XT, 4499 RMB (~$617 USD) for non-XT—likely boosting demand around that time. Last week, AMD board partners in Japan expressed concerns about current supply constraints—GPU market share in that region had climbed to ~45%, due to the popularity of RX 9070 Series graphics cards. Team Red could lose ground if GPU allocation limitations continue.

Yeston's social media accounts have alerted potential customers to re-stocks and connected developments—their latest bulletin hints about an improved situation, following another swift depletion of refreshed stock: "hello everyone! Thank you for the support! We have received a lot of messages and would love to inform you now the supply is unstable, but we will restock every week. Please don't be frustrated if you didn't get it. The supply will become stable and continue to be available after April." Interestingly, this morning's message did not touch upon the controversial topic of price hikes. At launch, Yeston's latest Navi 48 GPU-based offerings conformed or floated just above Team Red baseline MSRP (including VAT)—4999 RMB (~$686 USD) for XT, 4499 RMB (~$617 USD) for non-XT—likely boosting demand around that time. Last week, AMD board partners in Japan expressed concerns about current supply constraints—GPU market share in that region had climbed to ~45%, due to the popularity of RX 9070 Series graphics cards. Team Red could lose ground if GPU allocation limitations continue.

Global Top 10 IC Design Houses See 49% YoY Growth in 2024, NVIDIA Commands Half the Market

TrendForce reveals that the combined revenue of the world's top 10 IC design houses reached approximately US$249.8 billion in 2024, marking a 49% YoY increase. The booming AI industry has fueled growth across the semiconductor sector, with NVIDIA leading the charge, posting an astonishing 125% revenue growth, widening its lead over competitors, and solidifying its dominance in the IC industry.

Looking ahead to 2025, advancements in semiconductor manufacturing will further enhance AI computing power, with LLMs continuing to emerge. Open-source models like DeepSeek could lower AI adoption costs, accelerating AI penetration from servers to personal devices. This shift positions edge AI devices as the next major growth driver for the semiconductor industry.

Looking ahead to 2025, advancements in semiconductor manufacturing will further enhance AI computing power, with LLMs continuing to emerge. Open-source models like DeepSeek could lower AI adoption costs, accelerating AI penetration from servers to personal devices. This shift positions edge AI devices as the next major growth driver for the semiconductor industry.

Foxconn Reports 17-Year High in FY2024 & Q4 Financial Results

Hon Hai Technology Group ("Foxconn") today announced its full year and fourth quarter 2024 financial results.

Full year 2024 net profit reached NT$152.7 billion, resulting in earnings per share of NT$11.01, a 17-year-high. At the same time, the Group announced that it will distribute a cash dividend of NT$5.80 per share, a record level since it's listing in 1991. Despite significant changes in global tariff policies, geopolitical risks and monetary policies, the outlook for 2025 is for strong growth. The company also shared key developments around its three major smart platforms, as well as on AI and EV in 2025.

Full year 2024 net profit reached NT$152.7 billion, resulting in earnings per share of NT$11.01, a 17-year-high. At the same time, the Group announced that it will distribute a cash dividend of NT$5.80 per share, a record level since it's listing in 1991. Despite significant changes in global tariff policies, geopolitical risks and monetary policies, the outlook for 2025 is for strong growth. The company also shared key developments around its three major smart platforms, as well as on AI and EV in 2025.

Former Sony Exec Views First-party PS5 to PC Porting as "Almost Like Printing Money"

Last month, Shuhei Yoshida announced his retirement from Sony Interactive Entertainment. His career at the company started back in 1986, and by 1993 he became involved with the corporation's nascent PlayStation division. The Japanese industry veteran has gone on a press appearance blitz over the past couple of weeks; many headlines have been generated by his candid musings. Most recently, Sacred Symbols+ engaged in a conversation with Yoshida—their (paywalled) two-hour long podcast episode (#347) was made available to subscribers this week. The former PlayStation chief divulged that he pushed hard for the conversion of first-party titles from console origins to PC platforms, but his colleagues were reportedly reluctant to adopt this practice (at the time). Yoshida-san outlined the benefits: "releasing on PC does many things: it reaches a new audience who do not own consoles—especially in regions where consoles are not as popular. The idea is that those people may become fans of a particular franchise, and when a new game in that series comes out, they may be convinced to purchase a PlayStation." Sony started readjusting its exclusivity model a few years ago; greater ambitions were revealed in 2024.

He continued with this thought process: "it also adds additional income, because porting to PC is way cheaper than creating an original title...So, it's almost like printing money. And that helps us to invest in new titles now that the cost of games has increased." The ex-SIE boss believes that emerging markets are best served with releases on PC. Yoshida mentioned a huge (almost untapped) market—his ex-colleagues could do well, by targeting said region in the near future: "China is a huge PC game market...And China is a growing but very small console market. In order to reach the audience in countries like China then it's crucial to release on PC. So, I believe PC versions really reach a new audience." PC gamers have largely welcomed an improved flow of ported first-party titles, but Sony has absorbed feedback flak in early 2025; namely an underwhelming reception to Marvel's Spider-Man 2. In late January, Team Sony announced a revised PlayStation Network account policy; backpedalling from a system that featured strict sign-in requirements.

He continued with this thought process: "it also adds additional income, because porting to PC is way cheaper than creating an original title...So, it's almost like printing money. And that helps us to invest in new titles now that the cost of games has increased." The ex-SIE boss believes that emerging markets are best served with releases on PC. Yoshida mentioned a huge (almost untapped) market—his ex-colleagues could do well, by targeting said region in the near future: "China is a huge PC game market...And China is a growing but very small console market. In order to reach the audience in countries like China then it's crucial to release on PC. So, I believe PC versions really reach a new audience." PC gamers have largely welcomed an improved flow of ported first-party titles, but Sony has absorbed feedback flak in early 2025; namely an underwhelming reception to Marvel's Spider-Man 2. In late January, Team Sony announced a revised PlayStation Network account policy; backpedalling from a system that featured strict sign-in requirements.

Lenovo Group: Third Quarter Financial Results 2024/25

Lenovo Group Limited (HKSE: 992) (ADR: LNVGY), together with its subsidiaries ('the Group'), today announced Q3 results for fiscal year 2024/25, reporting significant increases in overall group revenue and profit. Revenue grew 20% year-on-year to US$18.8 billion, marking the third consecutive quarter of double-digit growth. Net income more than doubled year-on-year to US$693 million (including a non-recurring income tax credit of US$282 million) on a Hong Kong Financial Reporting Standards (HKFRS) basis. The Group's diversified growth engines continue to accelerate, with non-PC revenue mix up more than four points year-on-year to 46%. The quarter's results were driven by the Group's focused hybrid-AI strategy, the turnaround of the Infrastructure Solutions Group, as well as double-digit growth for both the Intelligent Devices Group and Solutions and Services Group.

Lenovo continues to invest in R&D, with R&D expenses up nearly 14% year-on-year to US$621 million. At the recent global technology event CES 2025, Lenovo launched a series of innovative products, including the world's first rollable AI laptop, the world's first handheld gaming device that allows gamers free choice of Windows OS or Steam OS, as well as Moto AI - winning 185 industry awards for its portfolio of innovation.

Lenovo continues to invest in R&D, with R&D expenses up nearly 14% year-on-year to US$621 million. At the recent global technology event CES 2025, Lenovo launched a series of innovative products, including the world's first rollable AI laptop, the world's first handheld gaming device that allows gamers free choice of Windows OS or Steam OS, as well as Moto AI - winning 185 industry awards for its portfolio of innovation.

Acer to Hike Prices in the US by Around 10 Percent Due to Tariffs, According to CEO

In an interview with The Telegraph, Acer CEO and chairman Jason Chen said that its products made in the PRC will see a price increase of 10 percent as direct results of the new tariffs that the US will levy on electronics. However, Mr Chen is quoted as saying "We think 10 percent probably will be the default price increase because of the import tax." which doesn't mean it will be exactly 10 percent, as it might vary a bit between product segments. That said, what's clear is that Acer and most likely every other company that manufactures hardware in the PRC aren't going to eat any of the tariffs, as the companies appear to be shifting the burden of the new tariffs straight over to the end consumers. Mr Chen also suggested that some companies might be increasing their pricing by more than 10 percent.

The price increase will happen over time, as the new tariffs won't affect products that have left the PRC before the end of February. Alongside Acer, which is the fifth-biggest computer brand in the US market, it's likely that Dell, HP and Lenovo, as well as Apple, are going to hike their prices by the same 10 percent or more. Acer moved the assembly of its desktop computers out of the PRC during Trump's previous term, when a 25 percent tariff was imposed. Now Acer is looking at moving at least some additional parts of its productions out of the PRC and the US is on the table for some of its products. Considering that some 80 percent of all laptops imported to the US are made in the PRC, the Consumer Trade Association is expecting the new tariffs to cost US consumers some US$143 billion, which it assumes will lead to a slump in sales of consumer electronics.

The price increase will happen over time, as the new tariffs won't affect products that have left the PRC before the end of February. Alongside Acer, which is the fifth-biggest computer brand in the US market, it's likely that Dell, HP and Lenovo, as well as Apple, are going to hike their prices by the same 10 percent or more. Acer moved the assembly of its desktop computers out of the PRC during Trump's previous term, when a 25 percent tariff was imposed. Now Acer is looking at moving at least some additional parts of its productions out of the PRC and the US is on the table for some of its products. Considering that some 80 percent of all laptops imported to the US are made in the PRC, the Consumer Trade Association is expecting the new tariffs to cost US consumers some US$143 billion, which it assumes will lead to a slump in sales of consumer electronics.

Global Semiconductor Manufacturing Industry Reports Solid Q4 2024 Results

The global semiconductor manufacturing industry closed 2024 with strong fourth quarter results and solid year-on-year (YoY) growth across most of the key industry segments, SEMI announced today in its Q4 2024 publication of the Semiconductor Manufacturing Monitor (SMM) Report, prepared in partnership with TechInsights. The industry outlook is cautiously optimistic at the start of 2025 as seasonality and macroeconomic uncertainty may impede near-term growth despite momentum from strong investments related to AI applications.

After declining in the first half of 2024, electronics sales bounced back later in the year resulting in a 2% annual increase. Electronics sales grew 4% YoY in Q4 2024 and are expected to see a 1% YoY increase in Q1 2025 impacted by seasonality. Integrated circuit (IC) sales rose by 29% YoY in Q4 2024 and continued growth is expected in Q1 2025 with a 23% increase YoY as AI-fueled demand continues boosting shipments of high-performance computing (HPC) and datacenter memory chips.

After declining in the first half of 2024, electronics sales bounced back later in the year resulting in a 2% annual increase. Electronics sales grew 4% YoY in Q4 2024 and are expected to see a 1% YoY increase in Q1 2025 impacted by seasonality. Integrated circuit (IC) sales rose by 29% YoY in Q4 2024 and continued growth is expected in Q1 2025 with a 23% increase YoY as AI-fueled demand continues boosting shipments of high-performance computing (HPC) and datacenter memory chips.

Supplier Production Cuts and AI Demand Expected to Drive NAND Flash Price Recovery in 2H25

TrendForce's latest findings reveal that the NAND Flash market continues to be plagued by oversupply in the first quarter of 2025, leading to sustained price declines and financial strain for suppliers. However, TrendForce anticipates a significant improvement in the market's supply-demand balance in the second half of the year.

Key factors contributing to this shift include proactive production cuts by manufacturers, inventory reductions in the smartphone sector, and growing demand driven by AI and DeepSeek applications. These elements are expected to alleviate oversupply and support a price rebound for NAND Flash.

Key factors contributing to this shift include proactive production cuts by manufacturers, inventory reductions in the smartphone sector, and growing demand driven by AI and DeepSeek applications. These elements are expected to alleviate oversupply and support a price rebound for NAND Flash.

GlobalFoundries Reports Fourth Quarter 2024 and Fiscal Year 2024 Financial Results

GlobalFoundries Inc. (GF), today announced preliminary financial results for the fourth quarter and fiscal year ended December 31, 2024.

"In the fourth quarter, the GF team delivered solid financial results that exceeded the Non-IFRS midpoint of the guidance ranges we provided in our November earnings release," said Dr. Thomas Caulfield, President and CEO of GF. "2024 presented a unique set of challenges for our industry, but thanks to our focus on operational excellence, we generated over $1 billion of Non-IFRS adjusted free cash flow. As we look to 2025, we are encouraged by our strong design win momentum across our end markets and product portfolio as we position GF for a growth year."

"In the fourth quarter, the GF team delivered solid financial results that exceeded the Non-IFRS midpoint of the guidance ranges we provided in our November earnings release," said Dr. Thomas Caulfield, President and CEO of GF. "2024 presented a unique set of challenges for our industry, but thanks to our focus on operational excellence, we generated over $1 billion of Non-IFRS adjusted free cash flow. As we look to 2025, we are encouraged by our strong design win momentum across our end markets and product portfolio as we position GF for a growth year."

Global Semiconductor Sales Hit $627 Billion in 2024

The Semiconductor Industry Association (SIA) today announced global semiconductor sales hit $627.6 billion in 2024, an increase of 19.1% compared to the 2023 total of $526.8 billion. Additionally, fourth-quarter sales of $170.9 billion were 17.1% more than the fourth quarter of 2023, and 3.0% higher than the third quarter of 2024. And global sales for the month of December 2024 were $57.0 billion, a decrease of 1.2% compared to the November 2024 total. Monthly sales are compiled by the World Semiconductor Trade Statistics (WSTS) organization and represent a three-month moving average. SIA represents 99% of the U.S. semiconductor industry by revenue and nearly two-thirds of non-U.S. chip firms.

"The global semiconductor market experienced its highest-ever sales year in 2024, topping $600 billion in annual sales for the first time, and double-digit market growth is projected for 2025," said John Neuffer, SIA president and CEO. "Semiconductors enable virtually all modern technologies - including medical devices, communications, defense applications, AI, advanced transportation, and countless others - and the long-term industry outlook is incredibly strong."

"The global semiconductor market experienced its highest-ever sales year in 2024, topping $600 billion in annual sales for the first time, and double-digit market growth is projected for 2025," said John Neuffer, SIA president and CEO. "Semiconductors enable virtually all modern technologies - including medical devices, communications, defense applications, AI, advanced transportation, and countless others - and the long-term industry outlook is incredibly strong."

Intel Xeon Server Processor Shipments Fall to a 13-Year Low

Intel's data center business has experienced a lot of decline in recent years. Once the go-to choice for data center buildout, nowadays, Xeon processors have reached a 13-year low. According to SemiAnalysis analyst Sravan Kundojjala on X, the once mighty has fallen to a 13-year low number, less than 50% of its CPU sales in the peak observed in 2021. In a chart that is indexed to 2011 CPU volume, the analysis gathered from server volume and 10K fillings shows the decline that Intel has experienced in recent years. Following the 2021 peak, the volume of shipped CPUs has remained in free fall, reaching less than 50% of its once-dominant position. The main cause for this volume contraction is attributed to Intel's competitors gaining massive traction. AMD, with its EPYC CPUs, has been Intel's primary competitor, pushing the boundaries on CPU core count per socket and performance per watt, all at an attractive price point.

During a recent earnings call, Intel's interim c-CEO leadership admitted that Intel is still behind the competition with regard to performance, even with Granite Rapids and Clearwater Forest, which promised to be their advantage in the data center. "So I think it would not be unfathomable that I would put a data center product outside if that meant that I hit the right product, the right market window as well as the right performance for my customers," said Intel co-CEO Michelle Johnston Holthaus, adding that "Intel Foundry will need to earn my business every day, just as I need to earn the business of my customers." This confirms that the company is now dedicated to restoring its product leadership, even if its internal foundry is not doing okay. It will take some time before Intel CPU volume shipments recover, and with AMD executing well in data center, it is becoming a highly intense battle.

During a recent earnings call, Intel's interim c-CEO leadership admitted that Intel is still behind the competition with regard to performance, even with Granite Rapids and Clearwater Forest, which promised to be their advantage in the data center. "So I think it would not be unfathomable that I would put a data center product outside if that meant that I hit the right product, the right market window as well as the right performance for my customers," said Intel co-CEO Michelle Johnston Holthaus, adding that "Intel Foundry will need to earn my business every day, just as I need to earn the business of my customers." This confirms that the company is now dedicated to restoring its product leadership, even if its internal foundry is not doing okay. It will take some time before Intel CPU volume shipments recover, and with AMD executing well in data center, it is becoming a highly intense battle.

German Tech Supply Chain Sees Massive 35% Market Contraction, Semiconductors Drop 41%

The fourth quarter of 2024 also remained well below the same quarter of the previous year, with a decline of more than 35%. At EUR 704 million, the turnover of FBDi's reporting members was the lowest since the end of 2020. For the whole of 2024, reporting members thus lost 36% of their previous year's turnover, reaching EUR 3464 million.

The biggest losses were suffered by semiconductors, which lost 41% of the previous year's turnover over the year as a whole, ending up at EUR 2192 million. The trend was slightly more positive for IP&E, which achieved a total volume of 1120 million euros for the year as a whole, a decline of only 25%. Especially Electromechanics (-15.8% y-o-y and BtB 1.04) and Power Supplies (-20.0% y-o-y and BtB 1.04) stand out positively.

The biggest losses were suffered by semiconductors, which lost 41% of the previous year's turnover over the year as a whole, ending up at EUR 2192 million. The trend was slightly more positive for IP&E, which achieved a total volume of 1120 million euros for the year as a whole, a decline of only 25%. Especially Electromechanics (-15.8% y-o-y and BtB 1.04) and Power Supplies (-20.0% y-o-y and BtB 1.04) stand out positively.

Former Sony Exec Believes PlayStation 6 Will Retain Optical Disc Support

A former chairman of Sony Interactive Entertainment USA—Shawn Layden—has shared his views regarding current and future PlayStation product landscapes. In an interview conducted by podcaster Reece Reilly (of KIWI TALKZ), the American businessman was asked about Microsoft's recent-ish release of all-digital Xbox home consoles. Layden believes that Sony will not copy its main rival's homework—the heavily rumored "PlayStation 6" could launch in two forms: with an optical drive, or without. The ex-SIE boss commented about a potential disc-less future platform: "I don't think Sony can get away with it now...I think Xbox has had more success in pursuing that strategy, but Xbox is really most successful in their business in a clutch of countries: the U.S., Canada, UK, Ireland, Australia, New Zealand, South Africa. Coincidentally enough—all English-speaking countries."

The current day PlayStation 5 family—consisting of standard, slim, and Pro models—is this generation's market leader; having established a huge international userbase (roughly 65 million units, back in September 2024). Layden cites these numbers as a guideline for the makeup of a new-gen model: "Sony, which is the number one platform in probably 170 countries around the world, has an obligation or a responsibility to say: 'If we go discless, how much of my market is not able to make that jump?' Can users in rural Italy get a decent connection to enjoy games?" He thinks that his former colleagues are making very careful considerations, given the complicated nature of catering to a diverse audience: "which part of your market will be damaged by going to disc-less market? I'm sure they're doing their research on it. And there will be a tipping point, where there's some percentage where you can say, 'Okay that's fine, we can turn our back on that part of the market.' But Sony's market is globally so huge, I think it would be hard for them to go fully disc-less, even with the next generation."

The current day PlayStation 5 family—consisting of standard, slim, and Pro models—is this generation's market leader; having established a huge international userbase (roughly 65 million units, back in September 2024). Layden cites these numbers as a guideline for the makeup of a new-gen model: "Sony, which is the number one platform in probably 170 countries around the world, has an obligation or a responsibility to say: 'If we go discless, how much of my market is not able to make that jump?' Can users in rural Italy get a decent connection to enjoy games?" He thinks that his former colleagues are making very careful considerations, given the complicated nature of catering to a diverse audience: "which part of your market will be damaged by going to disc-less market? I'm sure they're doing their research on it. And there will be a tipping point, where there's some percentage where you can say, 'Okay that's fine, we can turn our back on that part of the market.' But Sony's market is globally so huge, I think it would be hard for them to go fully disc-less, even with the next generation."

AMD Faces Investor Skepticism as AI Market Moves Toward Custom Chips

AMD is set to share its fourth-quarter results on Tuesday, Feb. 4 facing opportunities and problems in the fast-changing AI chip market as investors are expected to look closely at AMD's AI strategy. Reuters reports that experts think AMD's revenue will increase by over 22% to $7.53 billion. They expect its data center part to make up more than half of total sales at $4.15 billion. Yet, investors still worry about how AMD stands in the AI race. TD Cowen experts and Omdia believe AMD could sell $10 billion worth of AI chips this year, this is twice what AMD itself thinks it will sell, which is $5 billion. However, the scene is getting more complex with Big Tech firms like Microsoft, Amazon, and Meta making their own special chips for AI work. This move to custom chips, along with NVIDIA's strong market position and its popular CUDA software, makes things tough for AMD. The high costs of switching chipmakers also make it hard for AMD to grow its share of the market, however, the ongoing increase in AI spending by tech giants could help balance out these problems. Investors see "customer silicon and NVIDIA as the AI chip market going forward," said Ryuta Makino, analyst at AMD investor Gabelli Funds.

Supply chain issues make AMD's position more difficult as TSMC is boosting its advanced packaging ability to fix bottlenecks, while NVIDIA's production increase of its new "Blackwell" AI chips might restrict AMD's access to manufacturing resources. Yet, AMD's business has some good news, its personal computer unit should grow by almost 33% to $1.94 billion catching up to Intel.

Supply chain issues make AMD's position more difficult as TSMC is boosting its advanced packaging ability to fix bottlenecks, while NVIDIA's production increase of its new "Blackwell" AI chips might restrict AMD's access to manufacturing resources. Yet, AMD's business has some good news, its personal computer unit should grow by almost 33% to $1.94 billion catching up to Intel.

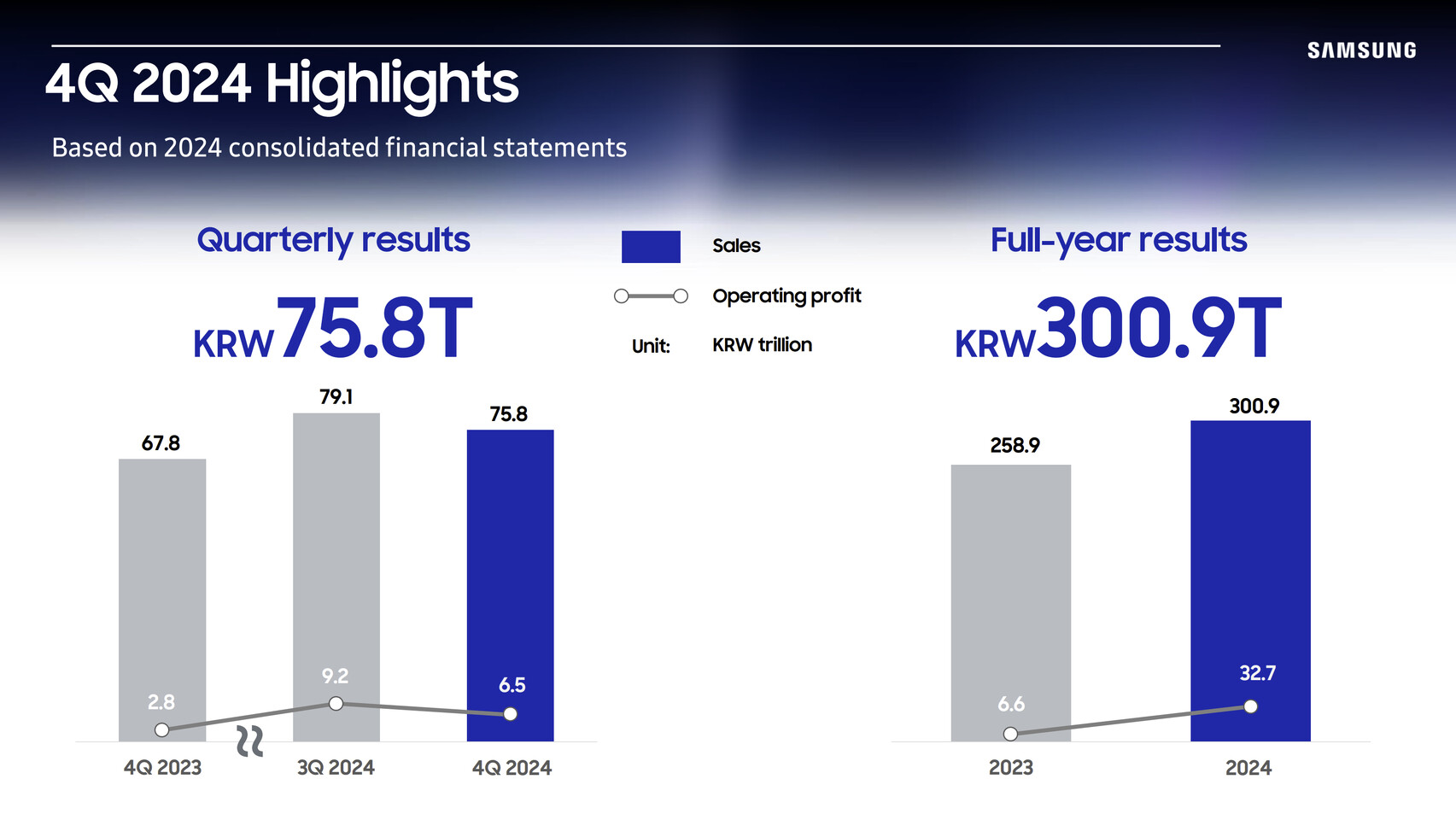

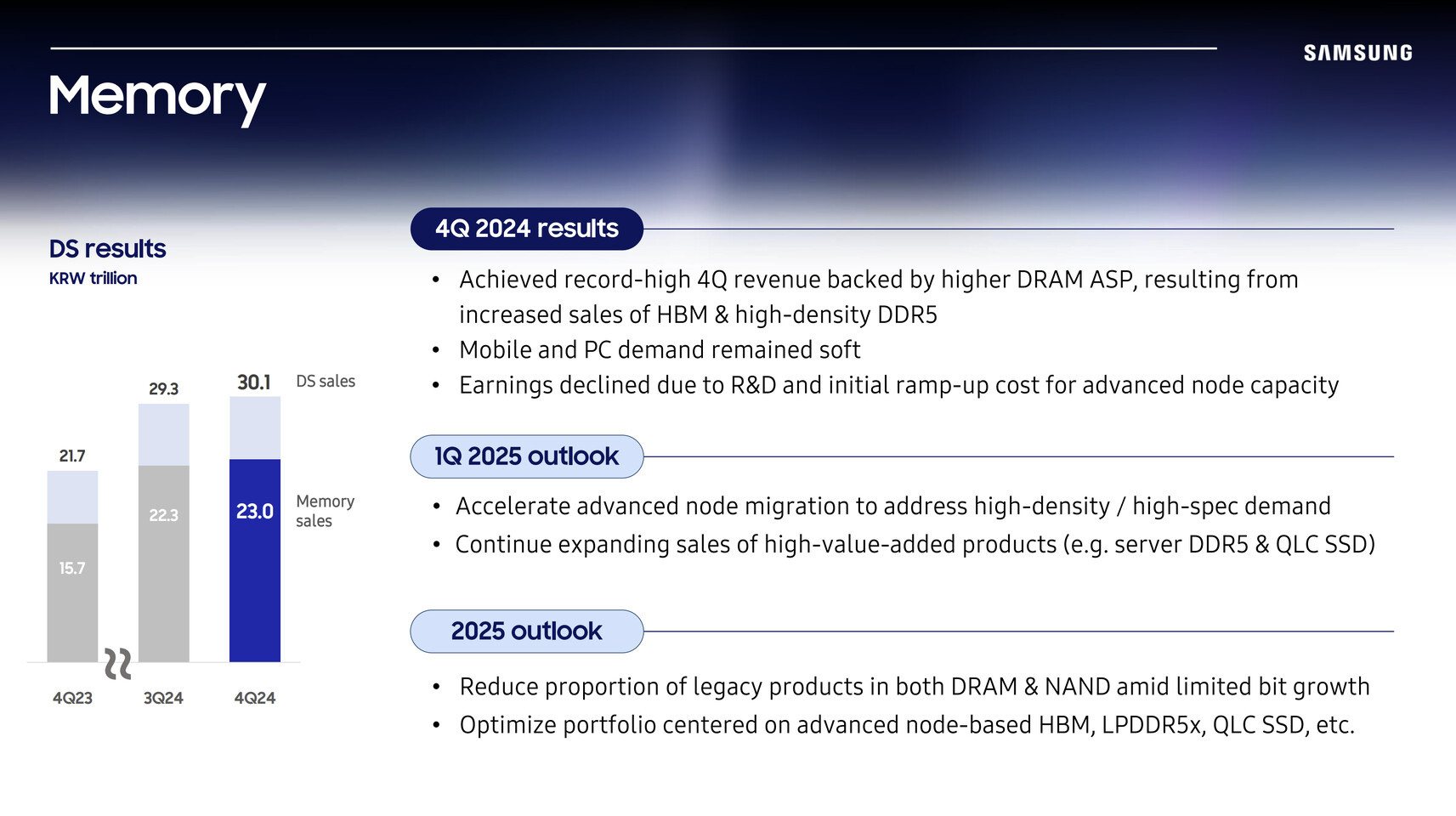

Samsung Electronics Announces Fourth Quarter and FY 2024 Results

Samsung Electronics today reported financial results for the fourth quarter and the fiscal year 2024. The Company posted KRW 75.8 trillion in consolidated revenue and KRW 6.5 trillion in operating profit in the quarter ended December 31, 2024. For the full year, it reported KRW 300.9 trillion in annual revenue and KRW 32.7 trillion in operating profit.

Although fourth quarter revenue and operating profit decreased on a quarter-on-quarter (QoQ) basis, annual revenue reached the second-highest on record, surpassed only in 2022. Meanwhile, operating profit was down KRW 2.7 trillion QoQ, due to soft market conditions especially for IT products, and an increase in expenditures including R&D. In the first quarter of 2025, while overall earnings improvement may be limited due to weakness in the semiconductors business, the Company aims to pursue growth through increased sales of smartphones with differentiated AI experiences, as well as premium products in the Device eXperience (DX) Division.

Although fourth quarter revenue and operating profit decreased on a quarter-on-quarter (QoQ) basis, annual revenue reached the second-highest on record, surpassed only in 2022. Meanwhile, operating profit was down KRW 2.7 trillion QoQ, due to soft market conditions especially for IT products, and an increase in expenditures including R&D. In the first quarter of 2025, while overall earnings improvement may be limited due to weakness in the semiconductors business, the Company aims to pursue growth through increased sales of smartphones with differentiated AI experiences, as well as premium products in the Device eXperience (DX) Division.

ASML Reports €28.3 Billion Total Net Sales and €7.6 Billion Net Income in 2024

Today, ASML Holding NV (ASML) has published its 2024 fourth-quarter and full-year results.

"Our fourth-quarter was a record in terms of revenue, with total net sales coming in at €9.3 billion, and a gross margin of 51.7%, both above our guidance. This was primarily driven by additional upgrades. We also recognized revenue on two High NA EUV systems. We shipped a third High NA EUV system to a customer in the fourth quarter.

- Q4 total net sales of €9.3 billion, gross margin of 51.7%, net income of €2.7 billion

- Quarterly net bookings in Q4 of €7.1 billion of which €3.0 billion is EUV

- 2024 total net sales of €28.3 billion, gross margin of 51.3%, net income of €7.6 billion

- ASML expects Q1 2025 total net sales between €7.5 billion and €8.0 billion, and a gross margin between 52% and 53%

- ASML expects 2025 total net sales to be between €30 billion and €35 billion, with a gross margin between 51% and 53%

"Our fourth-quarter was a record in terms of revenue, with total net sales coming in at €9.3 billion, and a gross margin of 51.7%, both above our guidance. This was primarily driven by additional upgrades. We also recognized revenue on two High NA EUV systems. We shipped a third High NA EUV system to a customer in the fourth quarter.

Apr 16th, 2025 10:08 EDT

change timezone

Latest GPU Drivers

New Forum Posts

- The TPU UK Clubhouse (26117)

- 5070ti overclock...what are your settings? (6)

- Help me identify Chip of this DDR4 RAM (21)

- Last game you purchased? (772)

- Windows 11 fresh install to do list (23)

- How to relubricate a fan and/or service a troublesome/noisy fan. (229)

- GPU Memory Temprature is always high (16)

- Help For XFX RX 590 GME Chinese - Vbios (4)

- PCGH: "hidden site" to see total money spend on steam (3)

- Share your AIDA 64 cache and memory benchmark here (3053)

Popular Reviews

- G.SKILL Trident Z5 NEO RGB DDR5-6000 32 GB CL26 Review - AMD EXPO

- ASUS GeForce RTX 5080 TUF OC Review

- DAREU A950 Wing Review

- The Last Of Us Part 2 Performance Benchmark Review - 30 GPUs Compared

- Sapphire Radeon RX 9070 XT Pulse Review

- Sapphire Radeon RX 9070 XT Nitro+ Review - Beating NVIDIA

- Upcoming Hardware Launches 2025 (Updated Apr 2025)

- Thermaltake TR100 Review

- Zotac GeForce RTX 5070 Ti Amp Extreme Review

- TerraMaster F8 SSD Plus Review - Compact and quiet

Controversial News Posts

- NVIDIA GeForce RTX 5060 Ti 16 GB SKU Likely Launching at $499, According to Supply Chain Leak (182)

- NVIDIA Sends MSRP Numbers to Partners: GeForce RTX 5060 Ti 8 GB at $379, RTX 5060 Ti 16 GB at $429 (124)

- Nintendo Confirms That Switch 2 Joy-Cons Will Not Utilize Hall Effect Stick Technology (105)

- Over 200,000 Sold Radeon RX 9070 and RX 9070 XT GPUs? AMD Says No Number was Given (100)

- Nintendo Switch 2 Launches June 5 at $449.99 with New Hardware and Games (99)

- Sony Increases the PS5 Pricing in EMEA and ANZ by Around 25 Percent (85)

- NVIDIA PhysX and Flow Made Fully Open-Source (77)

- NVIDIA Pushes GeForce RTX 5060 Ti Launch to Mid-April, RTX 5060 to May (77)