Report Suggests that Samsung Will Increase DRAM & NAND Prices by 3 to 5%

Earlier today, industry moles in South Korea have heard whispers about Samsung Electronics planning a new pricing strategy for NAND and DRAM product lines. According to an MK news articles, local sources believe that company leadership will: "raise memory chip prices—by 3-5% from the current level—for major global customers. It is reported that some customers have already begun contract negotiations that reflect the increase conditions." Regional watchdogs posit that the megacorporation is reacting to very current geopolitical tensions (i.e. tariffs). Earlier this week, a main rival—Micron—informed customers about forthcoming memory price increases. Naturally, the North American memory chip giant is not "fully" affected by recent seismic shifts. A "significant growth demand" has caused jacked up charges—effective across DRAM, NAND flash, and HBM portfolios—projected throughout 2025 and 2026.

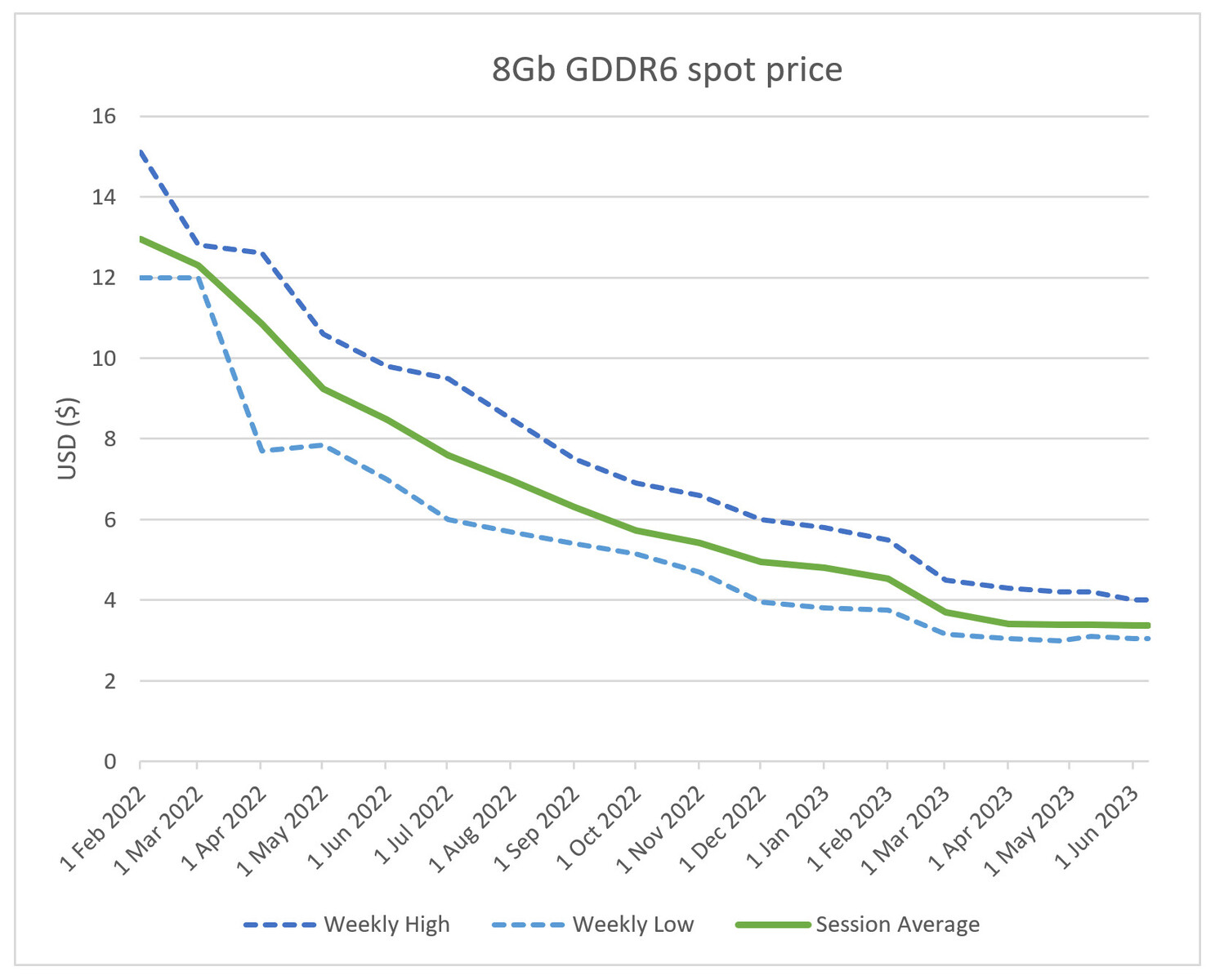

Returning to South Korean shores and Samsung, one unnamed semiconductor insider opined to MK: "oversupply continued throughout last year, but supply has recently decreased as major companies have begun to reduce production...In addition, artificial intelligence (AI) devices are appearing one after another in China, and demand for semiconductors is gradually increasing due to industrial automation." DRAMeXchange—an appropriately named market research organization—has kept track relevant trends. As disclosed by the MK news piece—as of last month, general-purpose DRAM DDR4 prices: "remained flat for the fourth month in a row." Looking at conditions for DDR5 (used in high-performance PCs and enterprise equipment), prices soared by 12%. DRAMeXchange observed NAND costs rising by 9.6%: "continuing an upward trend for the third consecutive month."

Returning to South Korean shores and Samsung, one unnamed semiconductor insider opined to MK: "oversupply continued throughout last year, but supply has recently decreased as major companies have begun to reduce production...In addition, artificial intelligence (AI) devices are appearing one after another in China, and demand for semiconductors is gradually increasing due to industrial automation." DRAMeXchange—an appropriately named market research organization—has kept track relevant trends. As disclosed by the MK news piece—as of last month, general-purpose DRAM DDR4 prices: "remained flat for the fourth month in a row." Looking at conditions for DDR5 (used in high-performance PCs and enterprise equipment), prices soared by 12%. DRAMeXchange observed NAND costs rising by 9.6%: "continuing an upward trend for the third consecutive month."