Tuesday, October 29th 2024

AMD Reports Third Quarter 2024 Financial Results, Revenue Up 18 Percent YoY

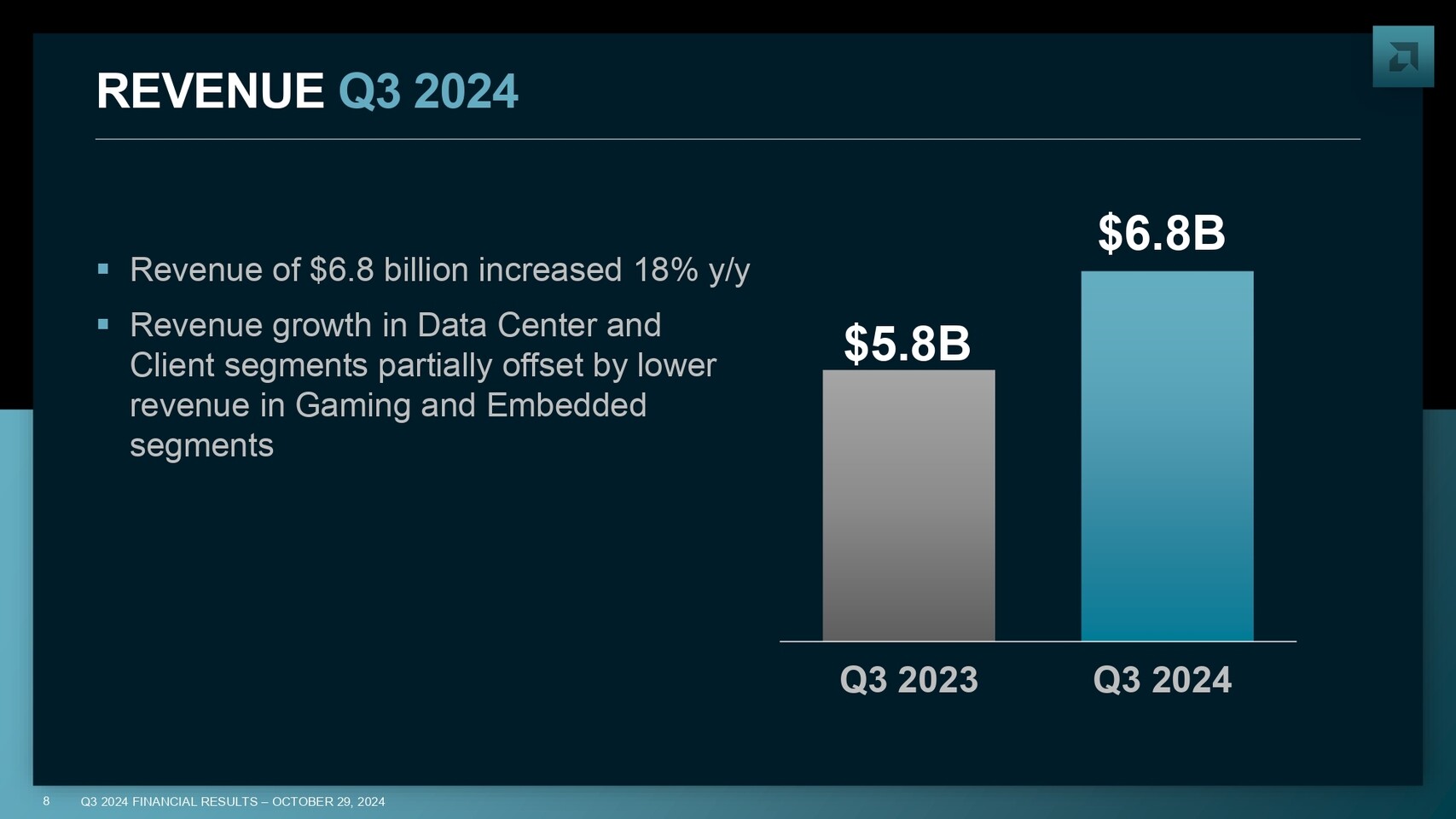

AMD today announced revenue for the third quarter of 2024 of $6.8 billion, gross margin of 50%, operating income of $724 million, net income of $771 million and diluted earnings per share of $0.47. On a non-GAAP basis, gross margin was 54%, operating income was $1.7 billion, net income was $1.5 billion and diluted earnings per share was $0.92.

"We delivered strong third quarter financial results with record revenue led by higher sales of EPYC and Instinct data center products and robust demand for our Ryzen PC processors," said AMD Chair and CEO Dr. Lisa Su. "Looking forward, we see significant growth opportunities across our data center, client and embedded businesses driven by the insatiable demand for more compute."

"We are pleased with our execution in the third quarter, delivering strong year-over-year expansion in gross margin and earnings per share," said AMD EVP, CFO and Treasurer Jean Hu. "We are on-track to deliver record annual revenue for 2024 based on significant growth in our Data Center and Client segments."

"We are pleased with our execution in the third quarter, delivering strong year-over-year expansion in gross margin and earnings per share," said AMD EVP, CFO and Treasurer Jean Hu. "We are on-track to deliver record annual revenue for 2024 based on significant growth in our Data Center and Client segments."

Segment Summary

Recent PR Highlights

Recent PR Highlights

AMD's outlook statements are based on current expectations. The following statements are forward-looking and actual results could differ materially depending on market conditions and the factors set forth under "Cautionary Statement" below.

For the fourth quarter of 2024, AMD expects revenue to be approximately $7.5 billion, plus or minus $300 million. At the mid-point of the revenue range, this represents year-over-year growth of approximately 22% and sequential growth of approximately 10%. Non-GAAP gross margin is expected to be approximately 54%.

Source:

AMD

"We delivered strong third quarter financial results with record revenue led by higher sales of EPYC and Instinct data center products and robust demand for our Ryzen PC processors," said AMD Chair and CEO Dr. Lisa Su. "Looking forward, we see significant growth opportunities across our data center, client and embedded businesses driven by the insatiable demand for more compute."

Segment Summary

- Record Data Center segment revenue of $3.5 billion was up 122% year-over-year and 25% sequentially primarily driven by the strong ramp of AMD Instinct GPU shipments and growth in AMD EPYC CPU sales.

- Client segment revenue was $1.9 billion, up 29% year-over-year and 26% sequentially primarily driven by strong demand for "Zen 5" AMD Ryzen processors.

- Gaming segment revenue was $462 million, down 69% year-over-year and 29% sequentially primarily due to a decrease in semi-custom revenue.

- Embedded segment revenue was $927 million, down 25% year-over-year as customers normalized their inventory levels. On a sequential basis, revenue increased 8% as demand improved in several end markets.

- At the Advancing AI 2024 event this month, AMD and strategic partners including Dell, Google Cloud, HPE, Lenovo, Meta, Microsoft, Oracle Cloud Infrastructure, Supermicro and AI leaders Databricks, Essential AI, Fireworks AI, Luma AI and Reka AI unveiled a broad portfolio of solutions delivering enterprise AI at scale based on the latest AMD Instinct accelerators, EPYC CPUs, AMD networking solutions and Ryzen PRO CPUs:

- New AMD EPYC 9005 Series processors, with record-breaking performance and energy efficiency for diverse data center needs, available in a wide range of platforms from leading OEMs and ODMs.

- AMD Instinct MI325X accelerators, delivering leadership performance and memory capabilities for the most demanding AI workloads. AMD also shared new details on next-gen AMD Instinct accelerators planned to launch in 2025 and 2026.

- An expanded high performance networking portfolio to maximize performance, scalability and efficiency for AI systems, with the new AMD Pensando Salina DPU and AMD Pensando Pollara 400 NIC.

- New Ryzen AI PRO 300 Series mobile processors, powering next-gen AI PCs for the enterprise with 50+ AI TOPS and leadership performance, battery life, security and manageability features.

- AMD continues to extend leadership AI performance, optimizations and customer adoption for AMD Instinct accelerators and AMD ROCm open software:

- Oracle Cloud Infrastructure selected AMD Instinct MI300X accelerators with AMD ROCm open software to power its latest OCI Compute Supercluster designed for demanding AI workloads.

- AMD unveiled its first results on leading AI benchmark MLPerf, revealing excellent performance for AMD Instinct MI300X accelerators advanced by the AMD ROCm software platform, on-par with NVIDIA H100.

- AMD highlighted support for the latest Llama 3.2 release from Meta, enabling developers to build new agentic applications and personalized AI experiences on AMD accelerators and processors from cloud to edge and AI PCs.

- AMD and ecosystem partners are enabling new AI PC platforms and capabilities:

- In partnership with Microsoft, AMD announced that Copilot+ will be enabled on AMD CPU-powered AI PCs via a free upgrade planned to be available starting in November 2024.

- OEM partners including Acer, HP, Lenovo and ASUS announced new systems powered by AMD Ryzen AI 300 Series mobile processors, leveraging the leadership gaming, content creation and everyday performance of the new "Zen 5" architecture.

- AMD expanded its embedded portfolio for a range of applications, including:

- New AMD EPYC Embedded 8004 Series processors, designed to deliver outstanding performance and power efficiency for demanding workloads.

- The smaller form factor, cost-optimized AMD Alveo UL3422 Accelerator Card, a fintech accelerator for ultra-low latency electronic trading applications.

- The AMD Artix UltraScale+ XA AU7P, a cost-optimized, automotive-qualified FPGA for ADAS sensor applications and in-vehicle infotainment.

- AMD announced an agreement to acquire ZT Systems, a leading provider of AI and general purpose compute infrastructure for the world's largest hyperscale providers, to expand the company's data center AI systems capabilities and accelerate deployment of AMD AI rack scale systems with cloud and enterprise customers. The acquisition is subject to regulatory clearance and other customary closing conditions and is expected to close in the first half of 2025.

- AMD completed the acquisition of Silo AI to accelerate development and deployment of AI models on AMD hardware.

- AMD and Intel announced the creation of an x86 ecosystem advisory group with Broadcom, Dell, Google, HPE, HP, Lenovo, Meta, Microsoft, Oracle, Red Hat and industry luminaries Linus Torvalds and Tim Sweeney to collaborate on architectural interoperability and simplify software development.

AMD's outlook statements are based on current expectations. The following statements are forward-looking and actual results could differ materially depending on market conditions and the factors set forth under "Cautionary Statement" below.

For the fourth quarter of 2024, AMD expects revenue to be approximately $7.5 billion, plus or minus $300 million. At the mid-point of the revenue range, this represents year-over-year growth of approximately 22% and sequential growth of approximately 10%. Non-GAAP gross margin is expected to be approximately 54%.

35 Comments on AMD Reports Third Quarter 2024 Financial Results, Revenue Up 18 Percent YoY

In its most recent quarter (August), Nvidia posted 154% YoY growth (8.5x more growth than AMD). Nvidia will report their earnings in a month but it is likely that they will forecast more than 22% YoY growth for the next quarter.

In short, Nvidia's business is growing much faster than AMD's, particularly its non-gaming business units. The market expects AMD to make a little more money. They expect Nvidia to make a lot more money. I mean a LOT.

We can forget about including Intel in this comparison right now. Nvidia's market cap is something like 30x bigger than Intel's. That wasn't the case twenty years ago.

Basically AMD is holding onto the ledge with their fingernails, not trying to fall in the abyss that Intel is in.

Note that the market punishing a company for weak guidance is very common. They aren't just picking on AMD. Apple stopped giving their own guidance when the pandemic began but never resumed providing guidance.

Anyhow, don't read too deeply into after hours trading. But for sure, AMD will open down tomorrow morning.

But the extreme rise of Nvidia dwarfs all players combined.

AMD needs to either combine Client and Gaming segments or get serious about GPUs for gaming.It’s time to ignore after hour results. None of the knee jerk reaction to earnings makes any sense.

If I have $100 I don't have to stick all of it in one company. I could stick $50 in Company N, $25 in Company A, $15 in Company I, and hold $10 in cash. Company A says "this is how we see our next quarter." If I don't like Company A's prospects, I could reduce my $25 investment by $15 and stick that money somewhere else, maybe Company G. That's what some of these after hours traders are doing. And tomorrow morning, the broad market will do the same.

Most investors don't stick all of their assets in one investment. So even those who invest in NVDA should have holdings in other companies. Maybe AMAT. Maybe AVGO. Maybe TSM. Maybe NXPI.

Remember not to think of investors as your little Aunt Millie buying one or two shares of AMD, AAPL, or GOOG. Most of these big companies' shares are controlled by institutional investors: fund managers, retirement funds, pension plans, etc. If you look at AMD's profile, 72.64% of the float is held by institutions.

One cardinal rule of investing: if you think your money has a better chance of appreciating somewhere other than your current investments, consider making an adjustment. A lot of beginner investors get stuck in a mindset that they will wait until things get better. If they buy Stock A at $100 which drops to $80, they will hold out until Stock A returns to $100. A smarter investor will look around and if they think Stock B has a chance of going from $30 to $40 in that timeframe, they'll jump ship.

This is why AMD, closing around $166 is down 27% compared to its 52-week high. By contrast, Nvidia is trading just 4% below its 52-week high. Nvidia is making more money and the market recognizes that. Both companies are seeing growth but Nvidia's is much steeper. And not just this quarter. Nvidia has been killing it in Datacenter for a couple of years. Every 19" rack filled with Nvidia GPUs is a 19" rack that's not filled with AMD or Intel.

And after hours trading after earnings is silly though. Always a stupid illogical knee jerk reaction and unpredictable.

I don't participate in after hours trading and try to avoid looking at it because often there is little correlation between after-hours prices and how the market will react on following day of regular trading. A slightly better clue is pre-market trading about 30 minutes before the opening bell. That's often a better gauge of what to expect but it's worth pointing out that the big boys (institutional investors) don't muck about with after hours.

After hours volumes are very small so there's a fair amount of pricing anomalies. After hours is mostly just juvenile drama like kids spazzing out about something trending on TikTok.

Right now, AMD is -8% after hours. Tomorrow if they are down a more modest -4%, that would still be a loss of $10.7 billion in market capitalization. What would a $10.7B loss in market cap be for NVDA? About -0.3%.

The primary responsibility for a publicly traded company is to increase shareholder value. AMD is doing that. The problem is that there are other companies who are offering greater increases in shareholder value. If I can still $100 in AMD and $100 in NVDIA. A year later, AMD is worth $119. Good. NVDA is worth $254. Better than good, great. And if both companies provide guidance that says things are going to be like this for a while, why wouldn't I pull out that $119 from AMD and stick it in NVDA? That's what some of these after hours investors are doing as we type this.

Remember, Nvidia has said that they've sold out of a year's worth of Blackwell GPUs. These are not customers who pick up a card at Best Buy and drive it home. These are billion dollar purchase orders.

At some point the AI craze and GPU market will cool off but the AI thing is still pretty early and everyone is trying to get a leg up on the competition. And there are plenty of people waiting for AI accelerator prices to come down. But it's not like Nvidia's phone at the orders desk is going to stop ringing tomorrow.

Now that being said, that's not what brings big money so what should AMD do about graphics ?

Look at nvidia, and also their own past, while gaming isn't what brings in the cash in buckets it spreads risk.

Nvidia makes AD102, it's massive and when they were designing it I don't think anyone would bet the market for gamers for such a large chip was worth the risk so what have nvidia been pivoting to?

A gpu that works in the datacenter and does decently at gaming, now they have 3 markets for one chip and they can take the reduced risk and make it large.

Datacenter (Nvidia L40), Gaming (RTX4090) and Professional (RTX6000 ada, RTX 5000 ada etc)

the risk profile is rather low because if datacenter sells less than expected they still have 2 other markets.

Lets look at the 7900XTX and what the market is for it?

Gaming...

when is the last time you saw a radeon pro gpu in a workstation ? and the AI ventures with it is extremely limited at best with the quality of ROCM for consumer gpu's, and not to mention how bad they are as a package when 100$ more gets you same performance at amd's best with all the other possibilities with nvidia with RT (rendering) and Tensor for AI and other things.

MI 300 series is doing pretty good but it's datacenter only, and it's not doing as good as nvidia

It punishes companies that have steady growth, and awards sudden jumps in value. But it also punishes sudden drops of growth, so if they'll see a ceiling to Nvidia's stellar growth in AI, there will be a large market correction...

It is a lose - lose situation for users of all tech that isn't AI related, and AI - well, it's now forced to be tech stock market saviour, and it will be a self fulfilling prophecy - everyone and their grandmother will only cater to AI.

retail investors look at the present share price. that is a mindset that took me years to change personally.makes perfect sense as it is small retail investors having an outsized effect on the price, but it also presents an opportunity if you want in on AMD or otherwise want to lower your cost basis.yup - don't be afraid to take losses here to make money elsewhere.

knowing when to fold is as important as knowing when to bet. both gambling and day trading.

don't forget, large investment funds (or even those that have large enough holdings) also value future payout of dividends as much as increases in share price. those are things that plug bottom lines.