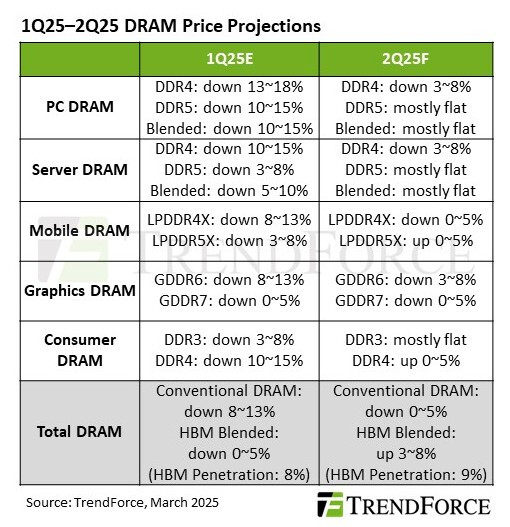

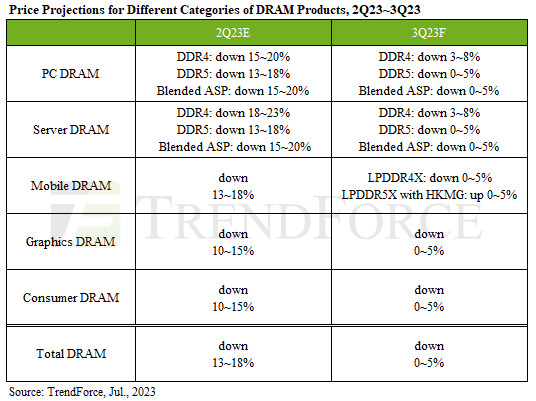

Downstream Inventory Reduction Eases DRAM Price Decline in 2Q25

TrendForce's latest findings reveal that U.S. tariff hikes prompted most downstream brands to frontload shipments to 1Q25, accelerating inventory reduction across the memory supply chain. Looking ahead to the second quarter, conventional DRAM prices are expected to decline by just 0-5% QoQ, while average DRAM pricing including HBM is forecast to rise by 3-8%, driven by increasing shipments of HBM3e 12hi.

PC and server DRAM prices to hold steady

In response to potential U.S. tariff hikes, major PC OEMs are requesting ODMs to increase production, accelerating DRAM depletion in their inventories. OEMs with lower inventory levels may raise procurement from suppliers in Q2 to ensure stable DRAM supply for the second half of 2025.

PC and server DRAM prices to hold steady

In response to potential U.S. tariff hikes, major PC OEMs are requesting ODMs to increase production, accelerating DRAM depletion in their inventories. OEMs with lower inventory levels may raise procurement from suppliers in Q2 to ensure stable DRAM supply for the second half of 2025.