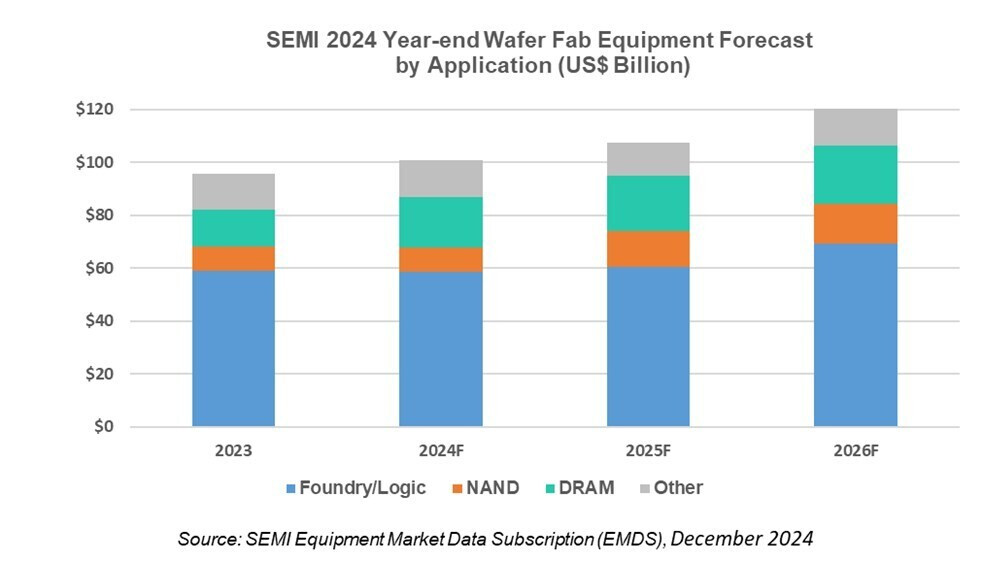

China Leads as Global Semiconductor Fab Investment Expected to Reach $110B in 2025

Global fab equipment spending for front-end facilities in 2025 is anticipated to increase by 2% year-over-year (YoY) to $110 billion, marking the sixth consecutive year of growth since 2020, SEMI announced today in its latest quarterly World Fab Forecast report.

Fab equipment spending is projected to rise by 18% in the following year, reaching $130 billion. This growth in investment is driven not only by demand in the high-performance computing (HPC) and memory sectors to support data center expansions, but also by the increasing integration of artificial intelligence (AI), which is driving up the silicon content required for edge devices.

Fab equipment spending is projected to rise by 18% in the following year, reaching $130 billion. This growth in investment is driven not only by demand in the high-performance computing (HPC) and memory sectors to support data center expansions, but also by the increasing integration of artificial intelligence (AI), which is driving up the silicon content required for edge devices.