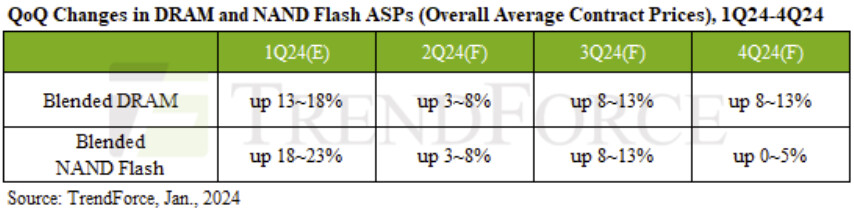

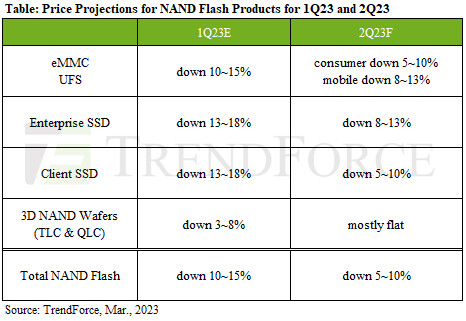

3Q25 NAND Flash Contract Prices Projected to Rise 5-10%; Weak Smartphone Demand Limits eMMC and UFS Growth

TrendForce's latest investigations find that the NAND Flash market has seen significant improvement in supply-demand balance following production cuts and inventory reduction in the first half of 2025. As suppliers shift production capacity toward higher-margin products, the overall supply in circulation has tightened.

On the demand side, increased enterprise investment in AI and mass shipments of NVIDIA's next-generation Blackwell chips have provided strong support. Looking ahead to the third quarter, average NAND Flash contract prices are projected to rise by 5% to 10%. However, due to an uncertain outlook for smartphone demand in the second half of the year, price increases for eMMC and UFS products are expected to be more modest.

On the demand side, increased enterprise investment in AI and mass shipments of NVIDIA's next-generation Blackwell chips have provided strong support. Looking ahead to the third quarter, average NAND Flash contract prices are projected to rise by 5% to 10%. However, due to an uncertain outlook for smartphone demand in the second half of the year, price increases for eMMC and UFS products are expected to be more modest.