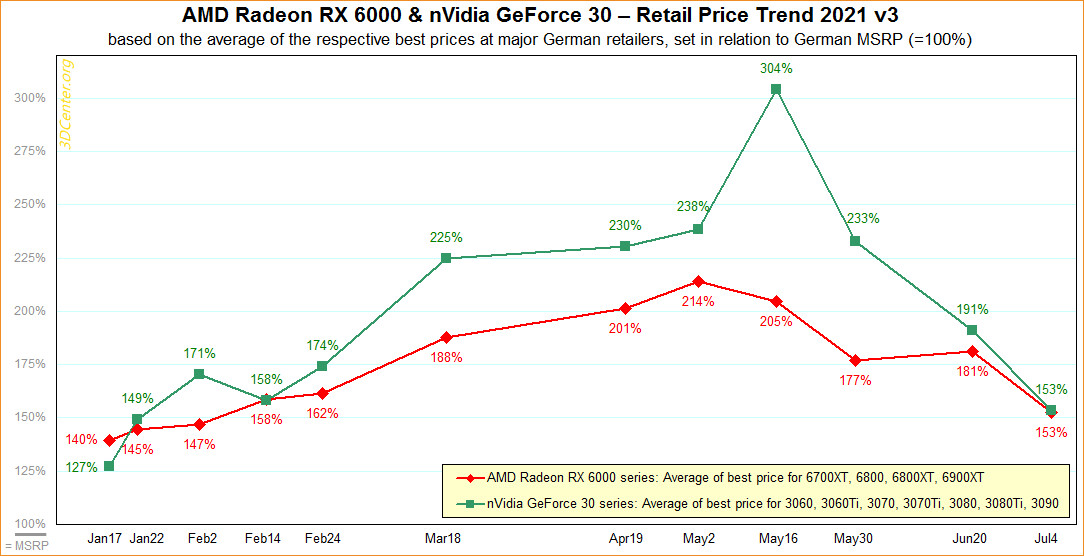

The German media outlet, 3D Center, has today published an updated report for July, measuring graphics card pricing in Germany and Austria, showing some pretty interesting results. The report is only measuring the pricing index of these two countries and their retailers, so it does not apply to other regions. An interesting discovery is that GPU prices have now hit the lowest point since February of this year when the sharp price incline started. At the time of reporting, GPU prices are exaggerated by around 53% over the MSRP listed prices. Not only did the prices drop, but the supply of GPUs like AMD Radeon RX 6800, Radeon RX 6800 XT, and the NVIDIA GeForce RTX 3060 Ti became much better, as consumers can get their hands on these now.

When looking at the graph below, note that MSRP is listed as 100%, and the percentage shown is the increase over that MSRP. When it comes to complete price reduction to the MSRP, 3D Center expects it to happen in 3-4 weeks possibly. If current data is to be believed, MSRP is slowly decreasing and supply is increasing rapidly. For more details and per-card pricing situation, head over to 3D Center website

here. Here is an important statement from 3D Center about the current situation:

3D Center (translated from German)Of course, this means that current street prices for graphics cards are (mostly) still exaggerated - and above all that this is the worst possible time to buy a graphics card. Because the (now clearly verifiable) tendency points to clearly lower graphics card prices in the next few weeks, with a similar pace, street prices at list price level could be in sight in 3-4 weeks. It is possible that there will be a certain braking effect in the downward price movement beforehand - but at least the way up to that point should definitely be taken with you. Apparently the delivery quantities are currently sufficient, maybe the need is a bit lower because of the summer times (and no longer available on the part of the crypto miners)so that retailers receive more cards than they sell. Since the retailers usually bought their cards from the distributors at an exaggerated price, the big game is now about who can get rid of the expensive stock goods in time to make a profit at all in the face of constantly falling sales prices.