The Molasses Flood Absorbed into CD Projekt Group, Studio Co-founder Confirms His Departure

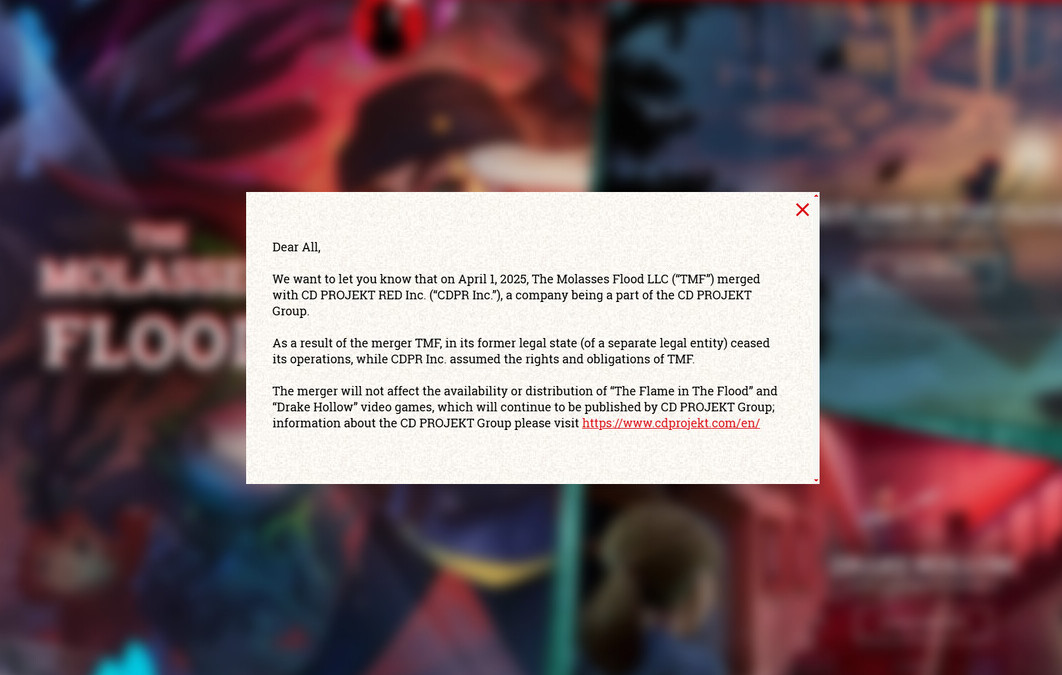

CD Projekt acquired The Molasses Flood—a Boston, Massachusetts-based video game developer—back in 2021. The New England studio was best known for making two indie titles: Drake Hollow (2020) and Flame in the Flood (2016). Under Polish ownership, the team embarked on a new "Project Sirius" adventure—several veteran members had spent time pumping out Bioshock, Halo, Guitar Hero and Rock Band franchise entries at previous workplaces. Earlier in the week, an official statement popped up on the company's official site: "dear all, we want to let you know that on April 1, 2025, The Molasses Flood LLC ("TMF") merged with CD PROJEKT RED Inc. ("CDPR Inc."), a company being a part of the CD PROJEKT Group. As a result of the merger TMF, in its former legal state (of a separate legal entity) ceased its operations, while CDPR Inc. assumed the rights and obligations of TMF. The merger will not affect the availability or distribution of 'The Flame in The Flood' and 'Drake Hollow' video games, which will continue to be published by CD PROJEKT Group."

In a LinkedIn post, Damian Isla provided an extra couple of tidbits and confirmed his exit from operations. The Molasses Flood (TMF) co-founder commented on recent reshuffles: "the studio I co-founded with some of my ex-Irrational friends, was to be absorbed into CDPR proper. To be ultra clear: this is a GOOD AND HEALTHY thing for the studio, and it was long-expected. It breaks down some organizational barriers, and better integrates the TMF team with the rest of the amazing CDPR org. Overall, it shows a very bright future for Project Sirius (aka "the multiplayer Witcher game," of which I was the Design Director for three years). It's going to be an amazing game, one for the books, and I cannot wait until the rest of the world learns about what we've been working on...On the sadder side—not to bury the lede—I've decided not to follow TMF on this transition. So last Monday—the last day of TMF's legal existence!—was also my last day at the studio."

In a LinkedIn post, Damian Isla provided an extra couple of tidbits and confirmed his exit from operations. The Molasses Flood (TMF) co-founder commented on recent reshuffles: "the studio I co-founded with some of my ex-Irrational friends, was to be absorbed into CDPR proper. To be ultra clear: this is a GOOD AND HEALTHY thing for the studio, and it was long-expected. It breaks down some organizational barriers, and better integrates the TMF team with the rest of the amazing CDPR org. Overall, it shows a very bright future for Project Sirius (aka "the multiplayer Witcher game," of which I was the Design Director for three years). It's going to be an amazing game, one for the books, and I cannot wait until the rest of the world learns about what we've been working on...On the sadder side—not to bury the lede—I've decided not to follow TMF on this transition. So last Monday—the last day of TMF's legal existence!—was also my last day at the studio."