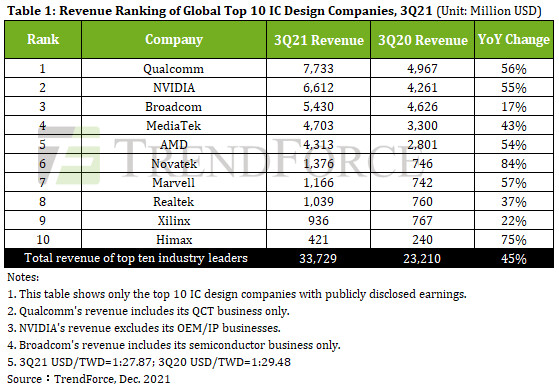

3Q21 Revenue of Global Top 10 IC Design (Fabless) Companies Reach US$33.7 billion, Four Taiwanese Companies Make List, Says TrendForce

The semicondustor market in 3Q21 is red hot with total revenue of the global top 10 IC design (fabless) companies reaching US$33.7 billion or 45% growth YoY, according to TrendForce's latest investigations. In addition to the Taiwanese companies MediaTek, Novatek, and Realtek already on the list, Himax comes in at number ten, bringing the total number of Taiwanese companies on the top 10 list to 4.

Qualcomm has been buoyed by continuing robust demand for 5G mobile phones form major mobile phone manufacturers with further revenue growth from its processor and radio frequency front end (RFFE) departments. Qualcomm's IoT department benefited from strong demand in the consumer electronics, edge networking, and industrial sectors, posting revenue growth of 66% YoY, highest among Qualcomm departments. In turn, this drove Qualcomm's total 3Q21 revenue to US$7.7 billion, 56% growth YoY, and ranking first in the world.

Qualcomm has been buoyed by continuing robust demand for 5G mobile phones form major mobile phone manufacturers with further revenue growth from its processor and radio frequency front end (RFFE) departments. Qualcomm's IoT department benefited from strong demand in the consumer electronics, edge networking, and industrial sectors, posting revenue growth of 66% YoY, highest among Qualcomm departments. In turn, this drove Qualcomm's total 3Q21 revenue to US$7.7 billion, 56% growth YoY, and ranking first in the world.