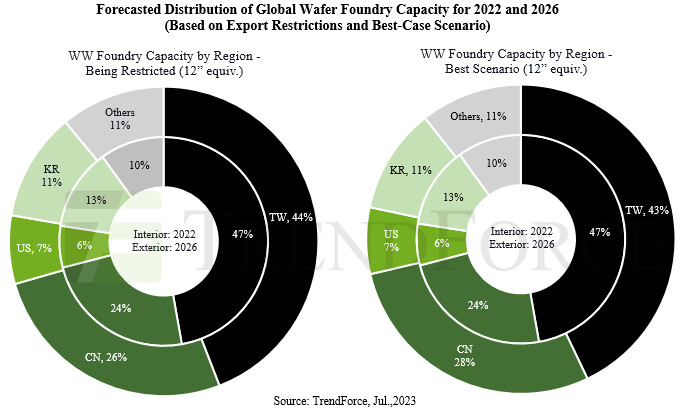

Despite Export Ban on Equipment, China's Semiconductor Expansion in Mature Processes Remains Strong

On June 30th, the Netherlands introduced new export restrictions on advanced semiconductor manufacturing equipment. Despite facing export controls from the US, Japan, and the Netherlands, TrendForce anticipates the market share of Chinese foundries in terms of 12-inch wafer production capacity will likely increase from 24% in 2022 to an estimated 26% in 2026. Moreover, if the exports of 40/28 nm equipment eventually receive approval, there's a chance that this market share could expand even further, possibly reaching 28% by 2026. This growth potential should not be dismissed.

Several manufacturing processes including photolithography, deposition, and epitaxy will be subject to these recent export restrictions. Beginning September 1st, the export of all controlled items will require formal authorization. TrendForce reports that Chinese foundries have been primarily developing mature processes like 55 nm, 40 nm, and 28 nm. Furthermore, demand for deposition equipment can be largely met by local Chinese vendors, meaning concerns regarding expansion and development are minimal. The main limiting factor, however, remains the equipment used in photolithography.

Several manufacturing processes including photolithography, deposition, and epitaxy will be subject to these recent export restrictions. Beginning September 1st, the export of all controlled items will require formal authorization. TrendForce reports that Chinese foundries have been primarily developing mature processes like 55 nm, 40 nm, and 28 nm. Furthermore, demand for deposition equipment can be largely met by local Chinese vendors, meaning concerns regarding expansion and development are minimal. The main limiting factor, however, remains the equipment used in photolithography.