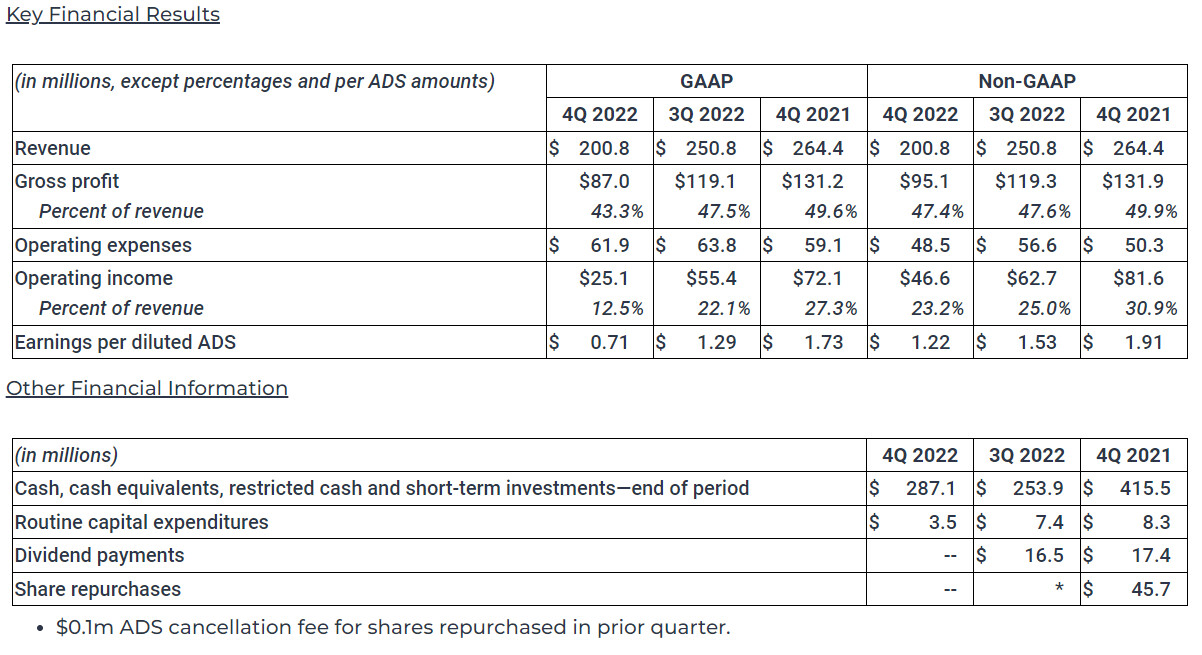

Silicon Motion Announces Q3'23 Results, Sales Up 23% Compared to Previous Quarter

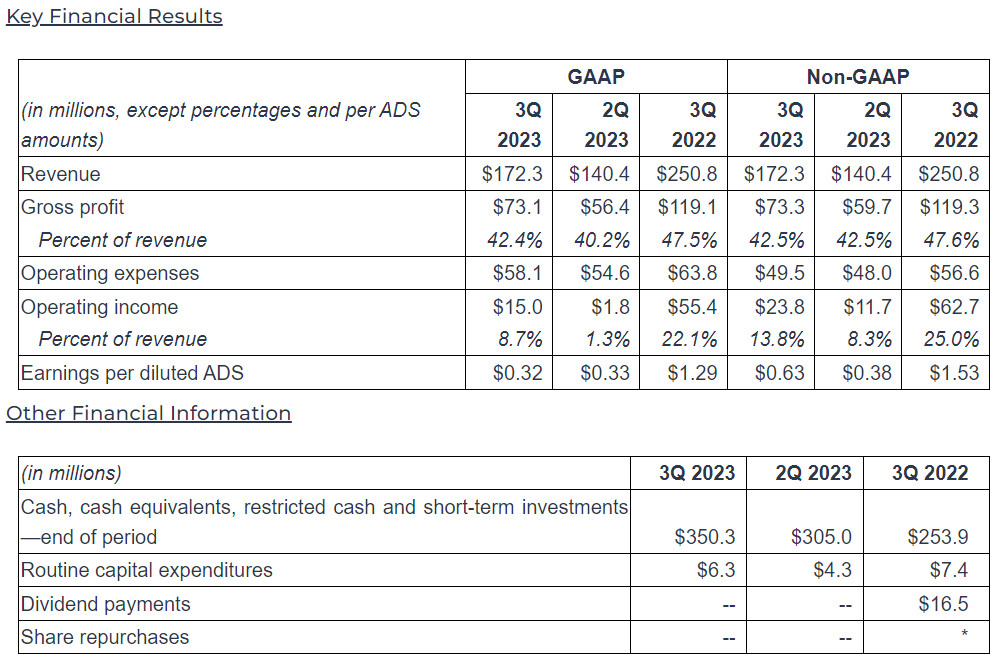

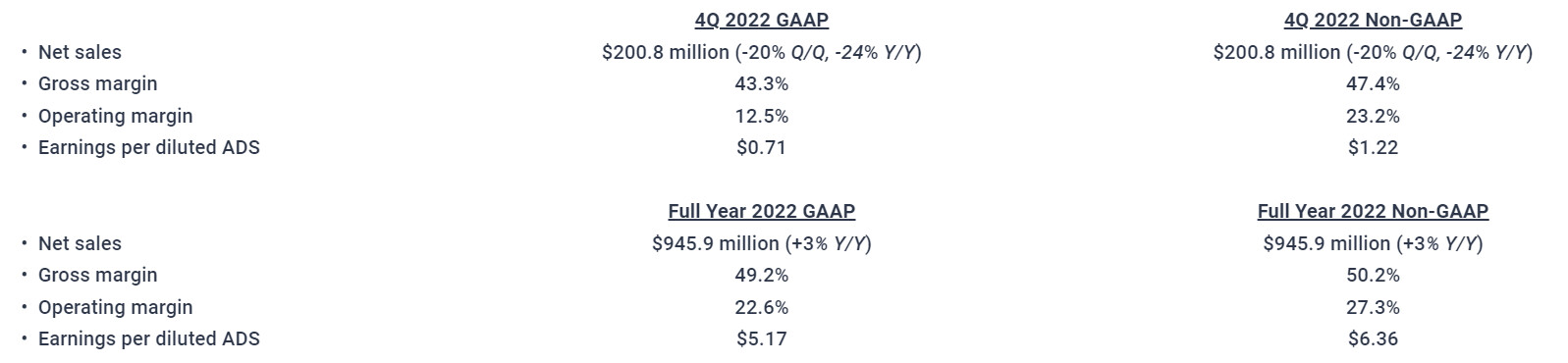

Silicon Motion Technology Corporation (NasdaqGS: SIMO) ("Silicon Motion", the "Company" or "we") today announced its financial results for the quarter ended September 30, 2023. For the third quarter of 2023, net sales (GAAP) increased sequentially to $172.3 million from $140.4 million in the second quarter of 2023. Net income (GAAP) decreased to $10.6 million, or $0.32 per diluted American Depositary Share of the Company ("ADS") (GAAP), from net income (GAAP) of $11.0 million, or $0.33 per diluted ADS (GAAP), in the second quarter of 2023.

For the third quarter of 2023, net income (non-GAAP) increased to $21.1 million, or $0.63 per diluted ADS (non-GAAP), from net income (non-GAAP) of $12.6 million, or $0.38 per diluted ADS (non-GAAP), in the second quarter of 2023.

For the third quarter of 2023, net income (non-GAAP) increased to $21.1 million, or $0.63 per diluted ADS (non-GAAP), from net income (non-GAAP) of $12.6 million, or $0.38 per diluted ADS (non-GAAP), in the second quarter of 2023.