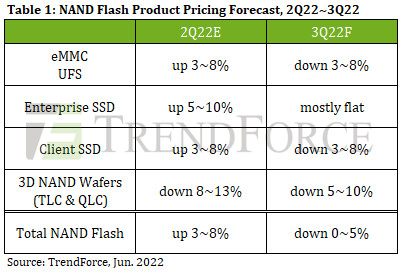

NAND Flash Market Oversupplied in 3Q22, Price Quotes to Drop by 0~5%, Says TrendForce

According to TrendForce research, as output from Kioxia and WDC grows month by month, it has become obvious that production capacity is sufficient to meet increased bit demand. However, post-pandemic demand for consumer electronics such as laptops will no longer lead to flagging orders. Coupled with slow destocking among Chinese smartphone brands due to the pandemic and rising inflation, these factors will lead to oversupply in the 3Q22 NAND Flash market, in turn affecting a price drop of 0~5% in 3Q22.

In terms of Client SSD, although a backstop for business notebook orders remains, demand for consumer notebook and Chromebook orders lags behind 2021, especially as PC brands stock more conservatively. Their intention to actively reduce inventory is obvious and the volume of orders in peak season may fall behind last year. However, as SSD production capacity gradually returns to normal, supply of client SSDs continues to increase. In addition, shipments of Kioxia and WDC products been delivered in succession. In order to avoid a sharp increase in inventory, the supply side is willing to let prices spike. Client SSD pricing is expected to reverse direction and move downwards approximately 3-8% in 3Q22.

In terms of Client SSD, although a backstop for business notebook orders remains, demand for consumer notebook and Chromebook orders lags behind 2021, especially as PC brands stock more conservatively. Their intention to actively reduce inventory is obvious and the volume of orders in peak season may fall behind last year. However, as SSD production capacity gradually returns to normal, supply of client SSDs continues to increase. In addition, shipments of Kioxia and WDC products been delivered in succession. In order to avoid a sharp increase in inventory, the supply side is willing to let prices spike. Client SSD pricing is expected to reverse direction and move downwards approximately 3-8% in 3Q22.