Tuesday, June 9th 2020

Notebook Computer Display Panel Shipment Grows by Nearly 18% YoY in 2Q20, with Demand Momentum Projected to Last Until 3Q20, Says TrendForce

According to the latest investigations from the WitsView research division of TrendForce, issues with the NB (notebook computer) panel supply chain, such as material shortage, labor shortage, and logistic disruptions, were gradually resolved starting in April. The resolution of these issues, combined with rising WFH and distance education demand brought about by the COVID-19 pandemic, resulted in a strong wave of panel demand in 2Q20. TrendForce projects 2Q20 NB panel shipment to reach 53.3 million units, a 17.7% increase YoY and 33.6% increase QoQ. TrendForce Research Manager Jeff Yang indicates that 1H20 NB panel shipment outperformed expectations set by the cyclical downturn of the period due to demand from WFH and distance education, while panel suppliers are now optimistic about the possibility for this demand to last until 3Q20. Given that the pandemic is expected to experience a slowdown in 2H20, the corresponding demand for notebook computers may also dissipate gradually. Even so, as end markets begin to open in various countries, NB brands will shift their sales focus from commercial and public applications to the consumer market instead. As well, the shipment momentum of NB panels is expected to last until 3Q20, driven by the restocking demand in NB brands' channel markets. However, with consumers in the post-COVID era projected to reduce their spending, the sell-through performance of end products will remain the key factor influencing the market for NB panels in 4Q20.

TrendForce Research Manager Jeff Yang indicates that 1H20 NB panel shipment outperformed expectations set by the cyclical downturn of the period due to demand from WFH and distance education, while panel suppliers are now optimistic about the possibility for this demand to last until 3Q20. Given that the pandemic is expected to experience a slowdown in 2H20, the corresponding demand for notebook computers may also dissipate gradually. Even so, as end markets begin to open in various countries, NB brands will shift their sales focus from commercial and public applications to the consumer market instead. As well, the shipment momentum of NB panels is expected to last until 3Q20, driven by the restocking demand in NB brands' channel markets. However, with consumers in the post-COVID era projected to reduce their spending, the sell-through performance of end products will remain the key factor influencing the market for NB panels in 4Q20.

On the whole, NB panel shipment saw subpar performance in 1Q20 due to the impact of COVID-19, but taking into account the surging demand in 2Q20 and improved market visibility in 3Q20, TrendForce projects NB panel shipment to reach 188.1 million units this year, a 0.2% increase YoY.

While the Rise of TN Panel Prices Is Clear, the Future of IPS Depends on LGD's Development Going Forward

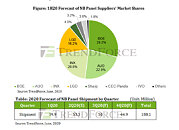

The status of NB panel supply this year is not too different from last year's, with the top four suppliers, ranked by shipment volume, still being BOE, AUO, Innolux, and LGD, respectively. These four companies together account for almost 90% market share in 1H20. TrendForce indicates that the supply of NB panels is much more oligopolistic relative to other types of panel applications, meaning the entrance of new suppliers does not significantly disrupt the market. In addition to the concentrated nature of the NB panel market, the NB demand generated by the pandemic drove NB panel prices to an uptrend in 2Q20. However, due to cost considerations, notebook computers for educational and WFH purposes are mostly equipped with relatively low-end TN panels rather than IPS panels, which are more common in the consumer market. As such, major suppliers of TN panels, including BOE, AUO, and Innolux, have increased the prices of their TN-based products in order to raise their products' gross margins.

Nevertheless, the long-term trend of NB panel development favors IPS technology. LGD, a major supplier of IPS panels, will terminate the production of TV panels in its Korean fab by the end of this year and transition to the production of IT products in the future. Therefore, LGD's most important priority at the moment is to maintain the market share of its IPS panels, whereas raising its panel prices remains a secondary concern. However, as the demand for consumer notebooks begins to recover, panel suppliers other than LGD will make a proactive effort to raise the price of IPS panels. Whether LGD will follow this market trend or whether it will instead focus on maintaining its market share is a development that remains to be seen.

On the whole, NB panel shipment saw subpar performance in 1Q20 due to the impact of COVID-19, but taking into account the surging demand in 2Q20 and improved market visibility in 3Q20, TrendForce projects NB panel shipment to reach 188.1 million units this year, a 0.2% increase YoY.

While the Rise of TN Panel Prices Is Clear, the Future of IPS Depends on LGD's Development Going Forward

The status of NB panel supply this year is not too different from last year's, with the top four suppliers, ranked by shipment volume, still being BOE, AUO, Innolux, and LGD, respectively. These four companies together account for almost 90% market share in 1H20. TrendForce indicates that the supply of NB panels is much more oligopolistic relative to other types of panel applications, meaning the entrance of new suppliers does not significantly disrupt the market. In addition to the concentrated nature of the NB panel market, the NB demand generated by the pandemic drove NB panel prices to an uptrend in 2Q20. However, due to cost considerations, notebook computers for educational and WFH purposes are mostly equipped with relatively low-end TN panels rather than IPS panels, which are more common in the consumer market. As such, major suppliers of TN panels, including BOE, AUO, and Innolux, have increased the prices of their TN-based products in order to raise their products' gross margins.

Nevertheless, the long-term trend of NB panel development favors IPS technology. LGD, a major supplier of IPS panels, will terminate the production of TV panels in its Korean fab by the end of this year and transition to the production of IT products in the future. Therefore, LGD's most important priority at the moment is to maintain the market share of its IPS panels, whereas raising its panel prices remains a secondary concern. However, as the demand for consumer notebooks begins to recover, panel suppliers other than LGD will make a proactive effort to raise the price of IPS panels. Whether LGD will follow this market trend or whether it will instead focus on maintaining its market share is a development that remains to be seen.

1 Comment on Notebook Computer Display Panel Shipment Grows by Nearly 18% YoY in 2Q20, with Demand Momentum Projected to Last Until 3Q20, Says TrendForce