Friday, March 31st 2023

Compute and Storage Cloud Infrastructure Spending Stays Strong as Macroeconomic Headwinds Strengthen in the Fourth Quarter of 2022, According to IDC

According to the International Data Corporation (IDC) Worldwide Quarterly Enterprise Infrastructure Tracker: Buyer and Cloud Deployment, spending on compute and storage infrastructure products for cloud deployments, including dedicated and shared IT environments, increased 16.3% year over year in the fourth quarter of 2022 (4Q22) to $24.1 billion. Spending on cloud infrastructure continues to outgrow the non-cloud segment although the latter had strong growth in 4Q22 as well, increasing 9.4% year over year to $18.7 billion. For the full year, cloud infrastructure grew 19.4% to $87.7 billion, while non-cloud grew 13.6% to $66.7 billion. The market continues to benefit from high demand, large backlogs, rising prices, and an improving infrastructure supply chain. Spending on shared cloud infrastructure reached $16.8 billion in the quarter, increasing 18.5% compared to a year ago. For the full year in 2022, spending on shared cloud infrastructure totaled $61.5 billion, growing 20.1% year over year. IDC expects to see continuous strong demand for shared cloud infrastructure, which is expected to surpass non-cloud infrastructure in spending in 2023. The dedicated cloud infrastructure segment grew 11.5% year over year in 4Q22 to $7.2 billion, and 18.0% in 2022 to $26.2 billion. Of the total dedicated cloud infrastructure, 45.5% was deployed on customer premises during the quarter, and 45.2% for the full year.

Spending on shared cloud infrastructure reached $16.8 billion in the quarter, increasing 18.5% compared to a year ago. For the full year in 2022, spending on shared cloud infrastructure totaled $61.5 billion, growing 20.1% year over year. IDC expects to see continuous strong demand for shared cloud infrastructure, which is expected to surpass non-cloud infrastructure in spending in 2023. The dedicated cloud infrastructure segment grew 11.5% year over year in 4Q22 to $7.2 billion, and 18.0% in 2022 to $26.2 billion. Of the total dedicated cloud infrastructure, 45.5% was deployed on customer premises during the quarter, and 45.2% for the full year.

For 2023, IDC is forecasting cloud infrastructure spending to grow 6.9% compared to 2022 to $93.7 billion - a significant decrease from the 19.4% annual growth in 2022. Non-cloud infrastructure is expected to decline 10.3% to $59.8 billion. Shared cloud infrastructure is expected to grow 7.5% year over year to $66.1 billion for the full year, while spending on dedicated cloud infrastructure is expected to grow 5.4% to $27.6 billion for the full year. The subdued growth forecast reflects the expectation that the market will face significant macroeconomic headwinds and curbed demand, with cloud staying positive due to the drive for modernization, opex focus, and continued growth in digital consumer services demand, while non-cloud spending contracts as enterprise customers shift towards capital preservation.

IDC tracks various categories of service providers and how much compute and storage infrastructure these service providers purchase, including both cloud and non-cloud infrastructure. The service provider category includes cloud service providers, digital service providers, communications service providers, and managed service providers. In 4Q22, service providers as a group spent $24.1 billion on compute and storage infrastructure, up 16.0% from the prior year. This spending accounted for 56.3% of the total market. Non-service providers (e.g., enterprises, government, etc.) increased their spending at a lower rate, 9.7% year over year. For 2022, service providers spent $87.9 billion, up 18.0% year over year, and accounting for 56.9% of total compute and storage spending for the year. Meanwhile, non-service providers grew 15.4% to $66.4 billion. IDC expects compute and storage spending by service providers to reach $92.3 billion in 2023, growing at 5.1% year over year.

On a geographic basis, year-over-year spending on cloud infrastructure in 4Q22 increased in all regions except Central & Eastern Europe (CEE), which is impacted by the Russia-Ukraine war. Spending in CEE declined 54.0% year over year. Latin America, Middle East & Africa (MEA), Western Europe, and USA grew the most at 38.6%, 38.0%, 25.5%, and 21.8% year over year, respectively. All other regions demonstrated growth in the teens and single digit percentages. For 2022, CEE declined 39.7%, MEA grew the most at 41.0%, and all other regions grew in the 10-30% range. For 2023, cloud infrastructure spending is expected to grow in all regions except CEE and MEA, with China (PRC) expected to grow 19.8%. All other regions (Asia/Pacific (excluding Japan and China), Canada, Japan, Latin America, USA, and Western Europe) are expected to post annual growth in the 0-10% range.

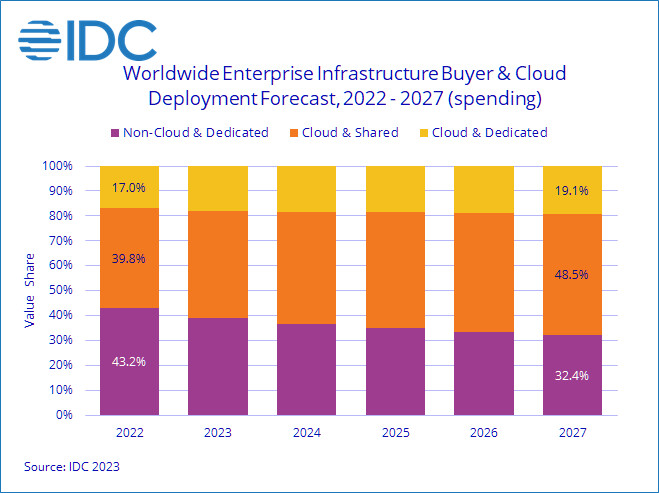

Long term, IDC predicts spending on cloud infrastructure to have a compound annual growth rate (CAGR) of 10.5% over the 2022-2027 forecast period, reaching $144.3 billion in 2027 and accounting for 67.6% of total compute and storage infrastructure spend. Shared cloud infrastructure will account for 71.7% of the total cloud amount, growing at a 11.0% CAGR and reaching $103.5 billion in 2027. Spending on dedicated cloud infrastructure will grow at a CAGR of 9.3% to $40.7 billion. Spending on non-cloud infrastructure will grow at a CAGR of 0.7%, reaching $69.0 billion in 2027. Spending by service providers on compute and storage infrastructure is expected to grow at a 10.0% CAGR, reaching $141.3 billion in 2027.

For 2023, IDC is forecasting cloud infrastructure spending to grow 6.9% compared to 2022 to $93.7 billion - a significant decrease from the 19.4% annual growth in 2022. Non-cloud infrastructure is expected to decline 10.3% to $59.8 billion. Shared cloud infrastructure is expected to grow 7.5% year over year to $66.1 billion for the full year, while spending on dedicated cloud infrastructure is expected to grow 5.4% to $27.6 billion for the full year. The subdued growth forecast reflects the expectation that the market will face significant macroeconomic headwinds and curbed demand, with cloud staying positive due to the drive for modernization, opex focus, and continued growth in digital consumer services demand, while non-cloud spending contracts as enterprise customers shift towards capital preservation.

IDC tracks various categories of service providers and how much compute and storage infrastructure these service providers purchase, including both cloud and non-cloud infrastructure. The service provider category includes cloud service providers, digital service providers, communications service providers, and managed service providers. In 4Q22, service providers as a group spent $24.1 billion on compute and storage infrastructure, up 16.0% from the prior year. This spending accounted for 56.3% of the total market. Non-service providers (e.g., enterprises, government, etc.) increased their spending at a lower rate, 9.7% year over year. For 2022, service providers spent $87.9 billion, up 18.0% year over year, and accounting for 56.9% of total compute and storage spending for the year. Meanwhile, non-service providers grew 15.4% to $66.4 billion. IDC expects compute and storage spending by service providers to reach $92.3 billion in 2023, growing at 5.1% year over year.

On a geographic basis, year-over-year spending on cloud infrastructure in 4Q22 increased in all regions except Central & Eastern Europe (CEE), which is impacted by the Russia-Ukraine war. Spending in CEE declined 54.0% year over year. Latin America, Middle East & Africa (MEA), Western Europe, and USA grew the most at 38.6%, 38.0%, 25.5%, and 21.8% year over year, respectively. All other regions demonstrated growth in the teens and single digit percentages. For 2022, CEE declined 39.7%, MEA grew the most at 41.0%, and all other regions grew in the 10-30% range. For 2023, cloud infrastructure spending is expected to grow in all regions except CEE and MEA, with China (PRC) expected to grow 19.8%. All other regions (Asia/Pacific (excluding Japan and China), Canada, Japan, Latin America, USA, and Western Europe) are expected to post annual growth in the 0-10% range.

Long term, IDC predicts spending on cloud infrastructure to have a compound annual growth rate (CAGR) of 10.5% over the 2022-2027 forecast period, reaching $144.3 billion in 2027 and accounting for 67.6% of total compute and storage infrastructure spend. Shared cloud infrastructure will account for 71.7% of the total cloud amount, growing at a 11.0% CAGR and reaching $103.5 billion in 2027. Spending on dedicated cloud infrastructure will grow at a CAGR of 9.3% to $40.7 billion. Spending on non-cloud infrastructure will grow at a CAGR of 0.7%, reaching $69.0 billion in 2027. Spending by service providers on compute and storage infrastructure is expected to grow at a 10.0% CAGR, reaching $141.3 billion in 2027.

Comments on Compute and Storage Cloud Infrastructure Spending Stays Strong as Macroeconomic Headwinds Strengthen in the Fourth Quarter of 2022, According to IDC

There are no comments yet.