Mar 13th, 2025 15:05 EDT

change timezone

Latest GPU Drivers

New Forum Posts

- TPU's F@H Team (20411)

- And so... I bought Arrow Lake (13700k to 265k), my thoughts. (29)

- What motherboard with spdif should I get? PC to 5.1 blu-ray player via optical (16)

- Dell Precision 5820 H950EF-00 Power Supply output (8)

- Tiktok channel cheating people into running powershell and unknowingly downloading malware. (7)

- Forums feature request: Markdown support (2)

- RX 9000 series GPU Owners Club (53)

- Help me find thumbscrews for SilentiumPC Regnum RG6V TG (0)

- What's your latest tech purchase? (23296)

- Free Games Thread (4558)

Popular Reviews

- AMD Ryzen 9 9950X3D Review - Great for Gaming and Productivity

- Sapphire Radeon RX 9070 XT Nitro+ Review - Beating NVIDIA

- XFX Radeon RX 9070 XT Mercury OC Magnetic Air Review

- FSP MP7 Black Review

- Dough Spectrum Black 32 Review

- ASUS Radeon RX 9070 TUF OC Review

- ASUS GeForce RTX 5090 TUF Review

- Gigabyte X870E Aorus Pro Review

- AMD Ryzen 7 9800X3D Review - The Best Gaming Processor

- NVIDIA GeForce RTX 5070 Founders Edition Review

Controversial News Posts

- NVIDIA GeForce RTX 50 Cards Spotted with Missing ROPs, NVIDIA Confirms the Issue, Multiple Vendors Affected (513)

- AMD Radeon RX 9070 and 9070 XT Listed On Amazon - One Buyer Snags a Unit (261)

- AMD RDNA 4 and Radeon RX 9070 Series Unveiled: $549 & $599 (260)

- AMD Mentions Sub-$700 Pricing for Radeon RX 9070 GPU Series, Looks Like NV Minus $50 Again (249)

- NVIDIA Investigates GeForce RTX 50 Series "Blackwell" Black Screen and BSOD Issues (244)

- AMD Radeon RX 9070 and 9070 XT Official Performance Metrics Leaked, +42% 4K Performance Over Radeon RX 7900 GRE (195)

- AMD Radeon RX 9070-series Pricing Leaks Courtesy of MicroCenter (158)

- AMD Radeon RX 9070 XT Reportedly Outperforms RTX 5080 Through Undervolting (103)

Thursday, October 31st 2024

Intel Reports Third-Quarter 2024 Financial Results

Intel Corporation today reported third-quarter 2024 financial results.

"Our Q3 results underscore the solid progress we are making against the plan we outlined last quarter to reduce costs, simplify our portfolio and improve organizational efficiency. We delivered revenue above the midpoint of our guidance, and are acting with urgency to position the business for sustainable value creation moving forward," said Pat Gelsinger, Intel CEO. "The momentum we are building across our product portfolio to maximize the value of our x86 franchise, combined with the strong interest Intel 18A is attracting from foundry customers, reflects the impact of our actions and the opportunities ahead."

"Restructuring charges meaningfully impacted Q3 profitability as we took important steps toward our cost reduction goal," said David Zinsner, Intel CFO. "The actions we took this quarter position us for improved profitability and enhanced liquidity as we continue to execute our strategy. We are encouraged by improved underlying trends, reflected in our Q4 guidance."

"Restructuring charges meaningfully impacted Q3 profitability as we took important steps toward our cost reduction goal," said David Zinsner, Intel CFO. "The actions we took this quarter position us for improved profitability and enhanced liquidity as we continue to execute our strategy. We are encouraged by improved underlying trends, reflected in our Q4 guidance."

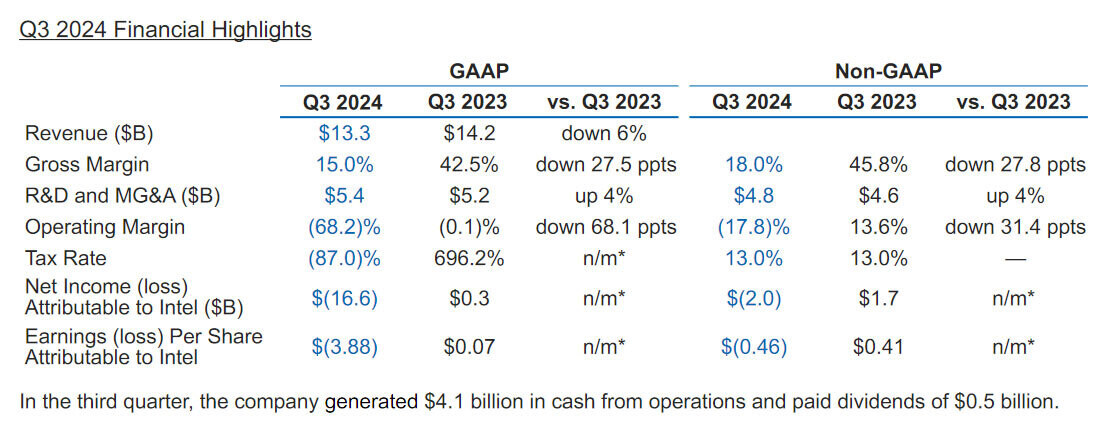

Q3 2024 Financial Highlights

In the third quarter, the company generated $4.1 billion in cash from operations and paid dividends of $0.5 billion.

Q3 2024 Restructuring and Impairment Charges

In the third quarter, the company made significant progress on its $10 billion cost reduction plan. The plan aims to drive operational efficiency and agility, accelerate profitable growth and create capacity for ongoing strategic investment in technology and manufacturing leadership. These initiatives include structural and operating realignment across the company, alongside reductions in headcount, operating expenses and capital expenditures. As a result of these actions, the company recognized $2.8 billion in restructuring charges in Q3 2024, $528 million of which are non-cash charges and $2.2 billion of which will be cash settled in the future.

Intel's third quarter results were also materially impacted by the following charges:

Business Unit Summary

In October 2022, Intel announced an internal foundry operating model, which took effect in the first quarter of 2024 and created a foundry relationship between its Intel Products business (collectively CCG, DCAI and NEX) and its Intel Foundry business (including Foundry Technology Development, Foundry Manufacturing and Supply Chain and Foundry Services, formerly IFS). The foundry operating model is designed to reshape operational dynamics and drive greater transparency, accountability, and focus on costs and efficiency. In furtherance of Intel's internal foundry operating model, Intel announced in the third quarter of 2024 its intent to establish Intel Foundry as an independent subsidiary. The company also previously announced its intent to operate Altera as a standalone business beginning in the first quarter of 2024. Altera was previously included in DCAI's segment results. As a result of these changes, the company modified its segment reporting in the first quarter of 2024 to align to this new operating model. All prior-period segment data has been retrospectively adjusted to reflect the way the company internally receives information and manages and monitors its operating segment performance starting in fiscal year 2024. There are no changes to Intel's consolidated financial statements for any prior periods.

Intel Products Highlights

Intel Foundry Highlights

Intel Foundry Highlights

Intel's guidance for the fourth quarter of 2024 includes both GAAP and non-GAAP estimates as follows:

Q4 2024 / GAAP / Non-GAAP

Revenue $13.3-14.3 billion

Gross Margin 36.5% / 39.5%

Tax Rate (50)% / 13%

Earnings (Loss) Per Share Attributable to Intel—Diluted $(0.24) $0.12

Reconciliations between GAAP and non-GAAP financial measures are included below. Actual results may differ materially from Intel's business outlook as a result of, among other things, the factors described under "Forward-Looking Statements" below. The gross margin and EPS outlook are based on the mid-point of the revenue range.

Source:

Intel

"Our Q3 results underscore the solid progress we are making against the plan we outlined last quarter to reduce costs, simplify our portfolio and improve organizational efficiency. We delivered revenue above the midpoint of our guidance, and are acting with urgency to position the business for sustainable value creation moving forward," said Pat Gelsinger, Intel CEO. "The momentum we are building across our product portfolio to maximize the value of our x86 franchise, combined with the strong interest Intel 18A is attracting from foundry customers, reflects the impact of our actions and the opportunities ahead."

Q3 2024 Financial Highlights

In the third quarter, the company generated $4.1 billion in cash from operations and paid dividends of $0.5 billion.

Q3 2024 Restructuring and Impairment Charges

In the third quarter, the company made significant progress on its $10 billion cost reduction plan. The plan aims to drive operational efficiency and agility, accelerate profitable growth and create capacity for ongoing strategic investment in technology and manufacturing leadership. These initiatives include structural and operating realignment across the company, alongside reductions in headcount, operating expenses and capital expenditures. As a result of these actions, the company recognized $2.8 billion in restructuring charges in Q3 2024, $528 million of which are non-cash charges and $2.2 billion of which will be cash settled in the future.

Intel's third quarter results were also materially impacted by the following charges:

- $3.1 billion of charges, substantially all of which were recognized in cost of sales, related to non-cash impairments and the acceleration of depreciation for certain manufacturing assets, a substantial majority of which related to the Intel 7 process node, based upon an evaluation of current process technology node capacities relative to projected market demand for Intel products and services;

- $2.9 billion of non-cash charges associated with the impairment of goodwill for certain reporting units - primarily the Mobileye reporting unit - as well as certain acquired intangible assets; and

- $9.9 billion of non-cash charges related to the establishment of a valuation allowance against U.S. deferred tax assets.

Business Unit Summary

In October 2022, Intel announced an internal foundry operating model, which took effect in the first quarter of 2024 and created a foundry relationship between its Intel Products business (collectively CCG, DCAI and NEX) and its Intel Foundry business (including Foundry Technology Development, Foundry Manufacturing and Supply Chain and Foundry Services, formerly IFS). The foundry operating model is designed to reshape operational dynamics and drive greater transparency, accountability, and focus on costs and efficiency. In furtherance of Intel's internal foundry operating model, Intel announced in the third quarter of 2024 its intent to establish Intel Foundry as an independent subsidiary. The company also previously announced its intent to operate Altera as a standalone business beginning in the first quarter of 2024. Altera was previously included in DCAI's segment results. As a result of these changes, the company modified its segment reporting in the first quarter of 2024 to align to this new operating model. All prior-period segment data has been retrospectively adjusted to reflect the way the company internally receives information and manages and monitors its operating segment performance starting in fiscal year 2024. There are no changes to Intel's consolidated financial statements for any prior periods.

Intel Products Highlights

- Intel announced plans with AMD to create the x86 Ecosystem Advisory Group, bringing together leaders from across the industry to help shape the future of x86. The Ecosystem Advisory Group is focused on simplifying software development, ensuring interoperability and interface consistency across vendors and providing developers with standard architectural tools and instructions. Broadcom, Dell, Google, HPE, HP Inc., Lenovo, Meta, Microsoft, Oracle, Red Hat have signed on as founding members.

- CCG: Intel continues to lead the AI PC category and is on track to ship more than 100 million AI PCs by the end of 2025. In September, Intel launched its Intel Core Ultra 200V series processors, code-named Lunar Lake, delivering several more hours of battery life and gains in performance, graphics and AI. This month, Intel launched the new Intel Core Ultra 200S processors, code-named Arrow Lake, that will scale AI PC capabilities to desktop platforms and usher in the first enthusiast desktop AI PCs.

- DCAI: Intel launched Intel Xeon, doubling the performance of the prior generation with increased core counts, memory bandwidth, and embedded AI acceleration. Intel also launched its Intel Gaudi 3 AI accelerators, delivering twice the networking bandwidth and 1.5x the memory bandwidth of its predecessor for large language model efficiency. IBM and Intel announced a global collaboration to deploy Intel Gaudi 3 AI accelerators as a service on IBM Cloud, aiming to help more cost-effectively scale enterprise AI and drive innovation underpinned with security and resiliency.

- NEX: Intel achieved a significant design win earlier this month with KDDI, a major global telecom, announcing its selection of Samsung's vRAN 3.0 solution powered by 4th Gen Intel Xeon Scalable processors with Intel vRAN Boost.

- Intel's fifth node in four years, Intel 18A, will complete a historic pace of design and process innovation, returning Intel to process leadership. Intel 18A is healthy and continues to progress well, and the company's two lead products, Panther Lake for client and Clearwater Forest for servers, have met early Intel 18A milestones ahead of next year's launches.

- Intel and Amazon Web Services (AWS) are finalizing a multi-year, multi-billion-dollar commitment to expand the companies' existing partnership to include a new custom Xeon 6 chip for AWS on Intel 3 and a new AI fabric chip for AWS on Intel 18A.

- The Biden-Harris Administration announced that Intel was awarded up to $3 billion in direct funding under the CHIPS and Science Act for the Secure Enclave program. The program is designed to expand the trusted manufacturing of leading-edge semiconductors for the U.S. government and fortify the domestic semiconductor supply chain.

- Intel announced its intention to establish Intel Foundry as an independent subsidiary. This structure provides clearer separation for external foundry customers and suppliers between Intel Foundry and Intel Products. It also gives Intel future flexibility to evaluate independent sources of funding and optimize the capital structure of Intel Foundry and Intel Products.

Intel's guidance for the fourth quarter of 2024 includes both GAAP and non-GAAP estimates as follows:

Q4 2024 / GAAP / Non-GAAP

Revenue $13.3-14.3 billion

Gross Margin 36.5% / 39.5%

Tax Rate (50)% / 13%

Earnings (Loss) Per Share Attributable to Intel—Diluted $(0.24) $0.12

Reconciliations between GAAP and non-GAAP financial measures are included below. Actual results may differ materially from Intel's business outlook as a result of, among other things, the factors described under "Forward-Looking Statements" below. The gross margin and EPS outlook are based on the mid-point of the revenue range.

Mar 13th, 2025 15:05 EDT

change timezone

Latest GPU Drivers

New Forum Posts

- TPU's F@H Team (20411)

- And so... I bought Arrow Lake (13700k to 265k), my thoughts. (29)

- What motherboard with spdif should I get? PC to 5.1 blu-ray player via optical (16)

- Dell Precision 5820 H950EF-00 Power Supply output (8)

- Tiktok channel cheating people into running powershell and unknowingly downloading malware. (7)

- Forums feature request: Markdown support (2)

- RX 9000 series GPU Owners Club (53)

- Help me find thumbscrews for SilentiumPC Regnum RG6V TG (0)

- What's your latest tech purchase? (23296)

- Free Games Thread (4558)

Popular Reviews

- AMD Ryzen 9 9950X3D Review - Great for Gaming and Productivity

- Sapphire Radeon RX 9070 XT Nitro+ Review - Beating NVIDIA

- XFX Radeon RX 9070 XT Mercury OC Magnetic Air Review

- FSP MP7 Black Review

- Dough Spectrum Black 32 Review

- ASUS Radeon RX 9070 TUF OC Review

- ASUS GeForce RTX 5090 TUF Review

- Gigabyte X870E Aorus Pro Review

- AMD Ryzen 7 9800X3D Review - The Best Gaming Processor

- NVIDIA GeForce RTX 5070 Founders Edition Review

Controversial News Posts

- NVIDIA GeForce RTX 50 Cards Spotted with Missing ROPs, NVIDIA Confirms the Issue, Multiple Vendors Affected (513)

- AMD Radeon RX 9070 and 9070 XT Listed On Amazon - One Buyer Snags a Unit (261)

- AMD RDNA 4 and Radeon RX 9070 Series Unveiled: $549 & $599 (260)

- AMD Mentions Sub-$700 Pricing for Radeon RX 9070 GPU Series, Looks Like NV Minus $50 Again (249)

- NVIDIA Investigates GeForce RTX 50 Series "Blackwell" Black Screen and BSOD Issues (244)

- AMD Radeon RX 9070 and 9070 XT Official Performance Metrics Leaked, +42% 4K Performance Over Radeon RX 7900 GRE (195)

- AMD Radeon RX 9070-series Pricing Leaks Courtesy of MicroCenter (158)

- AMD Radeon RX 9070 XT Reportedly Outperforms RTX 5080 Through Undervolting (103)

32 Comments on Intel Reports Third-Quarter 2024 Financial Results

I f’ing hate the stock market.

Oh and the earnings per share is negative. WTAF!!!

Let's see what pat's guidance is.

AMD is overvalued, If i had any I'd have gotten out.

The stock market strongly skews to be forward looking. The market already knew Intel's quarter was a loss and this has been priced into the stock (before earnings were announced).

These are all investing basics that apparently many people here don't understand. It's worth knowing even if you only have a retirement account or pension plan and don't actively trade individual stocks. It's worth knowing how the stock market operates because your retirement relies heavily on it.

You don't have to love the stock market but it's better to understand the basics of how it works. Because at some point you might be asked to make a particular decision (like mutual fund allocation). Knowing where your money is going and what to expect of it is more helpful than just random selection.

I would say they all are.

All I see is speculation. Intel big, therefore 'the worst is over' sentiment, despite their currently subpar-to-terrible product stack compared to the competition in just about every sector they have a product in, especially the high-margin sectors of Server CPU's & AI GPU's.

Intc isn't though considering their revenue, trajectory and NAV. But investors today are too focused on future guidance (mainly much how many AI accelerators they are going to sell) and that primarily determines market value.

Compared to a year ago when their server products were abysmal, desktop products were failing and laptop products were meh, at least they have competitive products on all three lines now. They just need to sell a load of them.

We must also realize that the incompetent Pat Gelsinger took control of Intel when the company had already been destroyed by two terrible CEOs before him: Bob Swan and, especially, Brian Krzanich. They undoubtedly had information about the development of AMD's Ryzen and EPYC CPUs and did not give orders for Intel engineers to develop equivalent CPUs in time.

I still don't know why Intel gave up on Optane (A.K.A. 3DXPoint) memories, which could have been bestsellers in the server sector. All I know is that Intel wanted to sell Optane SSDs with a few gigabytes at very high prices, much higher than SSDs with SLC and MLC flash memories, as if there was no competition... Something impractical.

Intel had a large fall in value at last quarter when they reported zero increase compared to last year. Now the investors have had some news about Intel taking drastic measures, laying off up to 20% of their workforce, other plans, so investors are perhaps feeling it won't get worse than this, it's the rock bottom, and the next quarter should bring in the uptake from the new CPU generation.

They don't follow for instance that for all the talk about how people don't mind a bit lower gaming performance of Arrow Lake CPUs, that they are actually impressed by the performance in applications combined with lower power draw - that this just doesn't translate into sales (might also be just that Intel hasn't had any stock at all in Europe).

Mindfactory Reports Zero Sales for Intel Arrow Lake Core Ultra 200S CPUs

On the other hand a destroyed Intel brings double digit, almost twice as much income and without income from AI hardware (they failed to even meet their low targets) and a GPU only company, Nvidia, is going from one record income to the next record income with record growth every quarter thanks to AI. AMD is a "wait for the next quarter" disappointment from an investor's perspective. A couple years ago Nvidia's share price was like 1.5-2.0 higher than AMD's and today it's close to 10 times AMD's share price compare to back then(Nvidia has done a 10 for 1 split). People hope and wait for AMD to become the next Nvidia, but this isn't happening. Time passes and if Intel starts fixing it's manufacturing and ARM starts becoming a real alternative to x86 in laptops and desktops (Nvidia is in the news of bringing it's own ARM for Windows solutions in late 25 or 26), if AMD keeps falling behind in gaming GPUs, maybe this is as far as AMD could go. It will be downhill from here and on if they don't decide to take a risk and try to become a REALLY BIG company.

they have insane revenue millions of customers sending them their monthly subscription fees and there is little indicating this will stop anytime soon As the customer is making money using those services or it’s in their life style (apple)

Nvidia is a gold pan seller during the gold rush, they are safe as long as gold fever lasts.

but people will find out they arent striking it rich as no one is finding those big nuggets promised.

as for amd best it can do is take over intels position entirely as in intel sells noting anymore everything x86 is now amd and they are already way over that in valuation.

This is all capital investments in US, not just into tech. We're basically still in the aftermath:

but there are 2 bubbles right now.

one is a tiny bubble and thats the one we are currently talking about when it pops people will be out of money and there will be a load of useless low precision gpgpu compute power sitting in racks doing jack.

the mega bubble is commercial real estate and when that happens starting WW3 will look like a better option to ‘our leaders’ than dealing with the pops fallout.

Also quite well explains why stock trading is nothing more than manipulation that sooner or later leads to huge crashes and economic shockwaves...

The only way to win is to play without bias. Stock picking is biased play.

But like I explained above but in reverse, seems that their future earnings have a the effect on their current capitulation.

But no, I am not an expert in finances, stocks or whatever, so everything I said could and might be just wrong.