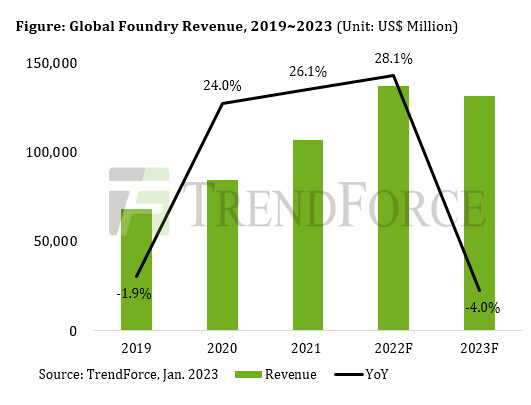

Global NAND Flash Revenue Reports a QoQ Decline of 25% in 4Q22 as ASP Drops Further

TrendForce's latest investigations reveal that the global NAND Flash market has been facing a demand headwind since 2H22. In response, the supply chain has been scrambling to clear out inventory, driving down NAND Flash contract prices by 20-25%. Enterprise SSD took the brunt of the fall with prices plummeting 23-28%. Despite manufacturers lowering prices in an attempt to drive up demand, clients are hesitant to purchase more components for fear of overstock. As a result, NAND Flash bit shipments rose by a mere 5.3% as ASP fell 22.8%. Global NAND Flash revenue was reported to be US$10.29 billion in 4Q22—down 25% QoQ.

TrendForce reports that Kioxia and Micron saw both a reduction in production and price in 4Q22. Kioxia's revenue plunged 30.5% due to weak demand from PC and smartphone clients and data centers readjusting their inventory. Micron generated a quarterly revenue of US$1.1 billion—a staggering 34.7% QoQ drop—that has led them to drastically decrease their capacity utilization rate for fabs. Luckily, Micron was able to ship their 232-layer client SSDs in 4Q22 as scheduled, and with the 176-layer QLC enterprise SSD hot on its heels, Micron's bit shipments are predicted to steadily improve in 2023 with their revenue climbing gradually quarter by quarter.

TrendForce reports that Kioxia and Micron saw both a reduction in production and price in 4Q22. Kioxia's revenue plunged 30.5% due to weak demand from PC and smartphone clients and data centers readjusting their inventory. Micron generated a quarterly revenue of US$1.1 billion—a staggering 34.7% QoQ drop—that has led them to drastically decrease their capacity utilization rate for fabs. Luckily, Micron was able to ship their 232-layer client SSDs in 4Q22 as scheduled, and with the 176-layer QLC enterprise SSD hot on its heels, Micron's bit shipments are predicted to steadily improve in 2023 with their revenue climbing gradually quarter by quarter.