Thursday, July 25th 2019

SK Hynix Reports Second Quarter 2019 Results

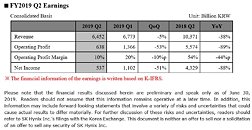

SK hynix Inc. today announced financial results for its second quarter 2019 ended on June 30, 2019. The consolidated second quarter revenue was 6.45 trillion won while the operating profit amounted to 638 billion won and the net income 537 billion won. Operating margin for the quarter was 10% and net margin was 8%.

As demand recovery did not meet expectations and price declines were steeper than expected, the revenue and the operating profit in the second quarter fell by 5% and 53%, respectively, quarter-over-quarter (QoQ). DRAM bit shipments increased by 13% QoQ as the Company actively responded to the mobile and PC DRAM markets, where demand growth was relatively high. However, DRAM prices remained weak and the average selling price dropped by 24%. For NAND Flash, the bit shipments increased by 40% QoQ because of demand recovery due to price declines, while the average selling price decreased by 25%. SK hynix plans to adjust production and investment flexibly to respond to the market conditions.

SK hynix plans to adjust production and investment flexibly to respond to the market conditions.

The Company will cut its DRAM production capacity from the fourth quarter and will convert part of the DRAM production lines of its M10 FAB in Icheon, Korea, to CMOS image sensor (CIS) mass production lines from the second half. This is to reduce DRAM wafer capacity considering the DRAM demand environment and to strengthen the competitiveness of its CIS business. In addition, with the capacity decrease due to DRAM tech migration, DRAM capacity is likely to continue to decrease until next year.

SK hynix added that it will also increase the NAND wafer input reduction this year to more than 15%. The Company announced last semester that it would decrease the NAND wafer input this year by more than 10% compared to last year.

In addition, SK hynix plans to review, assessing the demand situation, the timing of securing additional clean room space at its M15 FAB in Cheongju, Korea, and installing equipment at the M16 FAB in Icheon, which is expected to be completed in the second half of next year. As a result, the amount of investment next year is expected to be significantly lower than this year.

SK hynix will continue to focus on technology migration and high-density, high-value-added products.

The Company intends to increase the proportion of 1Xnm and 1Y nm DRAM to 80% by the end of this year and start selling 1Y nm computing products from the second half of this year.

For NAND Flash, SK hynix will focus on its 72-layer NAND but also plans to target the high-end smartphones and SSD market by increasing the proportion of 96-layer 4D NAND from the second half. The Company will prepare for mass production and sales of the 128-layer 1 Tb (Terabit) TLC (Triple Level Cell) 4D NAND Flash.

SK hynix will continue to strengthen its competitiveness in preparation for mid- to long-term memory growth.

As demand recovery did not meet expectations and price declines were steeper than expected, the revenue and the operating profit in the second quarter fell by 5% and 53%, respectively, quarter-over-quarter (QoQ). DRAM bit shipments increased by 13% QoQ as the Company actively responded to the mobile and PC DRAM markets, where demand growth was relatively high. However, DRAM prices remained weak and the average selling price dropped by 24%. For NAND Flash, the bit shipments increased by 40% QoQ because of demand recovery due to price declines, while the average selling price decreased by 25%.

The Company will cut its DRAM production capacity from the fourth quarter and will convert part of the DRAM production lines of its M10 FAB in Icheon, Korea, to CMOS image sensor (CIS) mass production lines from the second half. This is to reduce DRAM wafer capacity considering the DRAM demand environment and to strengthen the competitiveness of its CIS business. In addition, with the capacity decrease due to DRAM tech migration, DRAM capacity is likely to continue to decrease until next year.

SK hynix added that it will also increase the NAND wafer input reduction this year to more than 15%. The Company announced last semester that it would decrease the NAND wafer input this year by more than 10% compared to last year.

In addition, SK hynix plans to review, assessing the demand situation, the timing of securing additional clean room space at its M15 FAB in Cheongju, Korea, and installing equipment at the M16 FAB in Icheon, which is expected to be completed in the second half of next year. As a result, the amount of investment next year is expected to be significantly lower than this year.

SK hynix will continue to focus on technology migration and high-density, high-value-added products.

The Company intends to increase the proportion of 1Xnm and 1Y nm DRAM to 80% by the end of this year and start selling 1Y nm computing products from the second half of this year.

For NAND Flash, SK hynix will focus on its 72-layer NAND but also plans to target the high-end smartphones and SSD market by increasing the proportion of 96-layer 4D NAND from the second half. The Company will prepare for mass production and sales of the 128-layer 1 Tb (Terabit) TLC (Triple Level Cell) 4D NAND Flash.

SK hynix will continue to strengthen its competitiveness in preparation for mid- to long-term memory growth.

3 Comments on SK Hynix Reports Second Quarter 2019 Results

Frankly, kind of useless topic as nowadays those corps only care about fisting consumers back to stone age and pretend they're innocent with the standard non-RGB 16 GBs 3000mhz CL16 kit for 200$.

You really can't expect them to invest billions of dollars ( that's with a B ) and sell product at a low enough price that they almost lose money and more importantly, don't make enough money to pay for R&D to research faster, better, and cheaper products...