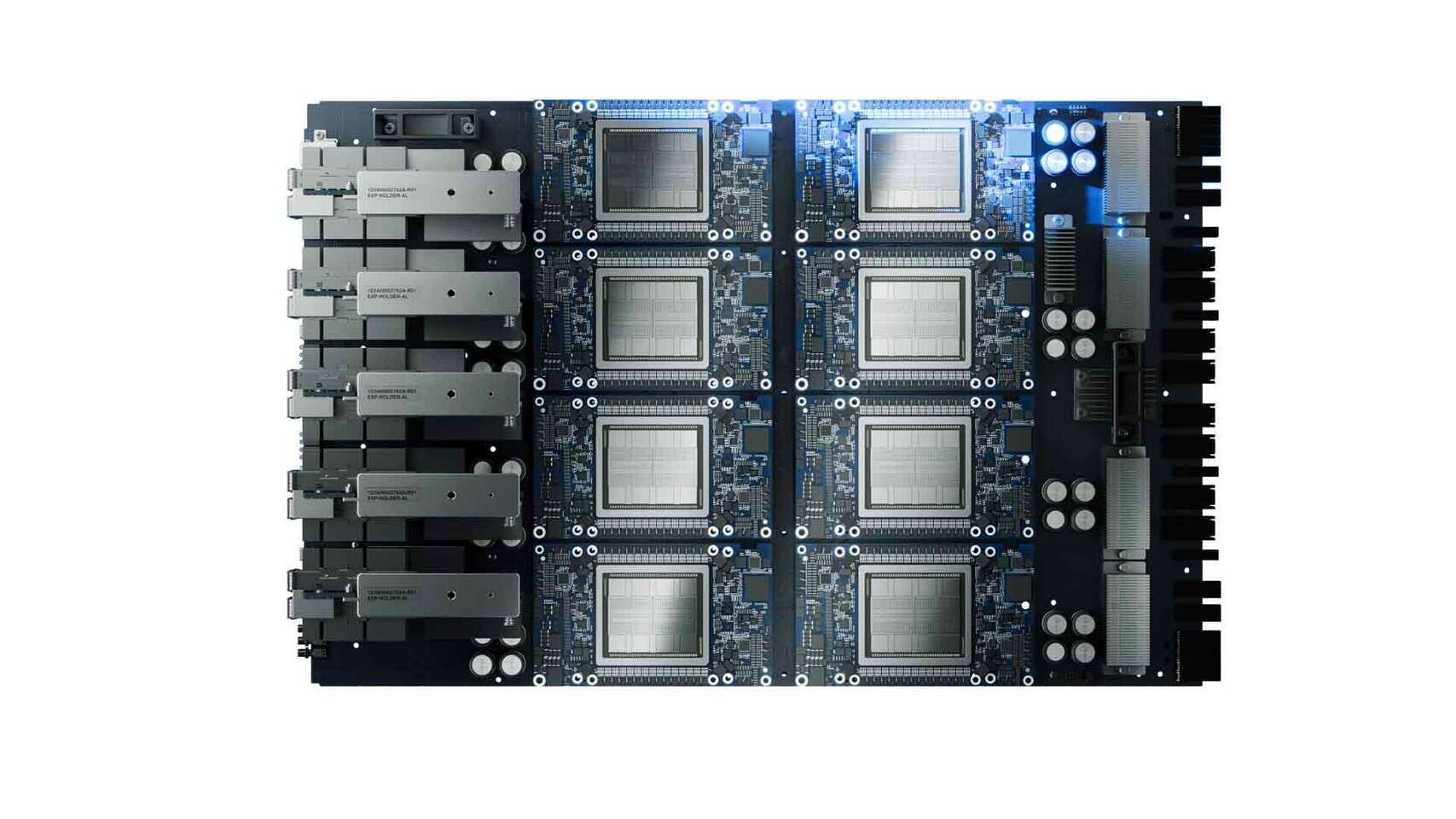

NVIDIA CEO Jensen Huang Asks SK hynix to Speed Up HBM4 Delivery by Six Months

SK hynix announced the first 48 GB 16-high HBM3E in the industry at the SK AI Summit in Seoul today. During the event, news came out about newer plans to develop their next-gen memory tech. Reuters and ZDNet Korea reported that NVIDIA CEO Jensen Huang asked SK hynix to speed up their HBM4 delivery by six months. SK Group Chairman Chey Tae-won shared this info at the Summit. The company had earlier said they would give HBM4 chips to customers in the second half of 2025.

When ZDNet asked about this sped-up plan, SK hynix President Kwak Noh-Jung gave a careful answer saying "We will give it a try." A company spokesperson told Reuters that this new schedule would be quicker than first planned, but they didn't share more details. In a video interview shown at the Summit, NVIDIA's Jensen Huang pointed out the strong team-up between the companies. He said working with SK hynix has helped NVIDIA go beyond Moore's Law performance gains. He stressed that NVIDIA will keep needing SK hynix's HBM tech for future products. SK hynix plans to supply the latest 12-layer HBM3E to an undisclosed customer this year, and will start sampling of the 16-layer HBM3E early next year.

When ZDNet asked about this sped-up plan, SK hynix President Kwak Noh-Jung gave a careful answer saying "We will give it a try." A company spokesperson told Reuters that this new schedule would be quicker than first planned, but they didn't share more details. In a video interview shown at the Summit, NVIDIA's Jensen Huang pointed out the strong team-up between the companies. He said working with SK hynix has helped NVIDIA go beyond Moore's Law performance gains. He stressed that NVIDIA will keep needing SK hynix's HBM tech for future products. SK hynix plans to supply the latest 12-layer HBM3E to an undisclosed customer this year, and will start sampling of the 16-layer HBM3E early next year.