Friday, September 24th 2021

Samsung Working on Attracting more Foundry Customers by Improving Customer Structure and Process Node Breakthroughs

Samsung is by far Samsung's largest foundry customers and this is no secret, but now it seems like the company wants to gain more customers to help pay for the costs of operating a cutting edge foundry. A little over a decade ago, Samsung was part of the Common Platform technology alliance together with GlobalFoundries and IBM, which allowed companies to almost pick either foundry based on a common design kit and common process technologies. It made Samsung an attractive foundry option, but the alliance didn't last.

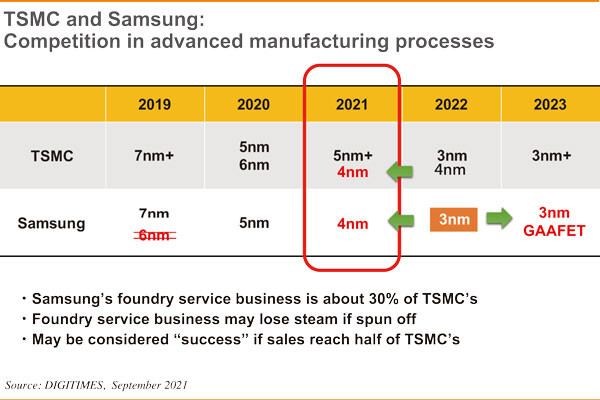

As we know, Nvidia gave Samsung a try with Ampere and there were a lot of reports of yield issues and what not early on. This seems to have persuaded Nvidia to move back to TSMC for Lovelace and Hopper, which is a big loss for Samsung. However, it seems this was also something of a wakeup call for Samsung, as the company is apparently looking at making some internal changes to its customer structure so it can handle third party customers in a better way. Samsung is ready to start producing chips on its 4 nm node this year, with its 3 nm GAAFET node expected to live in 2023, something that was revealed earlier this year. This is at least six months to a year behind TSMC's 3 nm node which is expected to go into production in the second half of 2022. According to DigiTimes, TSMC already has 60 EUV tools for its 3 nm node in its possession, whereas Samsung in comparison is only expected to have 20 at the most and isn't expected to have more than 30 by the end of this year.

Samsung is ready to start producing chips on its 4 nm node this year, with its 3 nm GAAFET node expected to live in 2023, something that was revealed earlier this year. This is at least six months to a year behind TSMC's 3 nm node which is expected to go into production in the second half of 2022. According to DigiTimes, TSMC already has 60 EUV tools for its 3 nm node in its possession, whereas Samsung in comparison is only expected to have 20 at the most and isn't expected to have more than 30 by the end of this year.

Maybe the biggest issue for Samsung is that its foundry business isn't making money, as the second quarter profits were only US$268 million, with TSMC raking in over US$13 billion at the same time. Even SMIC and UMC are more profitable than Samsung and it's likely that some of this is down to the fact that third parties are wary about using Samsung's foundries due to a wide range of reasons, least not that Samsung is often a direct competitor. Samsung has considered spinning off its foundry business in the past and this might still come to pass, but it's apparently not something the company is considering at the moment.

Samsung has a lot of work ahead of itself to not only stay competitive with TSMC, but also to convince potential customers to choose them over its competitors, even more so now maybe, as Intel is also vying for a slice of the foundry business cake. With TSMC having announced that it'll be investing US$100 billion between 2021 and 2023, in capacity expansion, or roughly twice that of Samsung's sales from its foundry business, it's going to be tough for Samsung to stay competitive without more business. Rumours are that Tesla might be moving from TSMC to Samsung and we also know that Google is working with Samsung on its Tensor SoC. However these are still fairly small business opportunities and Samsung needs some high-volume customers to be able to keep up with TSMC long term.

Source:

DigiTimes

As we know, Nvidia gave Samsung a try with Ampere and there were a lot of reports of yield issues and what not early on. This seems to have persuaded Nvidia to move back to TSMC for Lovelace and Hopper, which is a big loss for Samsung. However, it seems this was also something of a wakeup call for Samsung, as the company is apparently looking at making some internal changes to its customer structure so it can handle third party customers in a better way.

Maybe the biggest issue for Samsung is that its foundry business isn't making money, as the second quarter profits were only US$268 million, with TSMC raking in over US$13 billion at the same time. Even SMIC and UMC are more profitable than Samsung and it's likely that some of this is down to the fact that third parties are wary about using Samsung's foundries due to a wide range of reasons, least not that Samsung is often a direct competitor. Samsung has considered spinning off its foundry business in the past and this might still come to pass, but it's apparently not something the company is considering at the moment.

Samsung has a lot of work ahead of itself to not only stay competitive with TSMC, but also to convince potential customers to choose them over its competitors, even more so now maybe, as Intel is also vying for a slice of the foundry business cake. With TSMC having announced that it'll be investing US$100 billion between 2021 and 2023, in capacity expansion, or roughly twice that of Samsung's sales from its foundry business, it's going to be tough for Samsung to stay competitive without more business. Rumours are that Tesla might be moving from TSMC to Samsung and we also know that Google is working with Samsung on its Tensor SoC. However these are still fairly small business opportunities and Samsung needs some high-volume customers to be able to keep up with TSMC long term.

23 Comments on Samsung Working on Attracting more Foundry Customers by Improving Customer Structure and Process Node Breakthroughs

There were some benchmark leaks already, if I ain't wrong.

Samsung's node names aren't really the concern here, bur rather how they are going to be able to attract customers that brings in extra revenue. Samsung manufacturing for Samsung isn't going to bring in sufficient funds for the foundry to keep developing new nodes, which long term means that Samsung's foundry business is either going to take a bigger and bigger chunk of Samsung's profits to stay competitive, or they're going to have to slow down and might even end up in a similar situation as GloFo where they simply stop developing new nodes due to the costs involved.

As for revenue etc. those are public figures that Samsung has to publish, so it's not like DigiTimes published some secret insider info in the article.

Considering that there's only one company that makes the machines that are used at these types of nodes, i.e. ASML and the fact that they can only produce so many machines, it's not strange that they've prioritised their best customer. It's also no secret that each node shrink is getting more and more expensive to develop.

So please, enlighten me, what exactly is fud here?

I'm not saying you have to agree with this point of view, but you have to provide a compelling argument to go with your comment.

I'm not sure what you read, but what I wrote about was Samsung's struggle with attracting big bucks customers for their foundry business, which again isn't a secret.

How you went from that to fud is a bit strange...

I have no inside knowledge.

www.hardwaretimes.com/tsmc-and-samsungs-4nm-nodes-to-power-top-end-processors-in-2022-a-closer-look-at-the-two/

www.hpcwire.com/off-the-wire/samsung-foundry-certifies-synopsys-primelib/

1) Keep releasing RTX 3000 series (and maybe soon, 3000 SUPER series) from Samsung 8nm

2) Maybe re-introduce Turing at 12nm TSMC (RTX 2060 with 12GB rumour + other SKUs. Because everything sells right now. GTX 1660 Super sells for 400+ dollars where I live)

3) Use TSMC 5-6nm for RTX 4000 series in Q3 2022

Nvidia already gained 3% marketshare in 3 months, they now sit at 83% dGPU marketshare.

Intel dGPUs in Q1 2022 targetting AMDs primary segment; Low to Mid-end. If they go with aggressive pricing, AMD will have a hard time on the dGPU market going forward. Intel will want to gain marketshare fast, and they have to sell GPUs at low margins to do this.

AMD used to have a few good value cards every generation - cards that sold well - think RX580,570,480,470 - AMDs best selling GPUs in the last 5 years .. yet 6600 and 6700 series have horrible pricing and availability because AMD downplays GPU output at TSMC and this is one of the reasons why Nvidia gained marketshare fast. AMD 6000 series mostly exists on paper, insanely low output.

All this is the reason why Nvidia went Samsung in the first place. Good decision looking back. If Ampere had been on TSMC 7nm GPU availablity would be hell instead of just poor.