Friday, June 28th 2024

Q3 Contract Prices of NAND Flash Products Constrained by Increased Production and Lower End-User Demand; Estimated to Rise by 5-10%

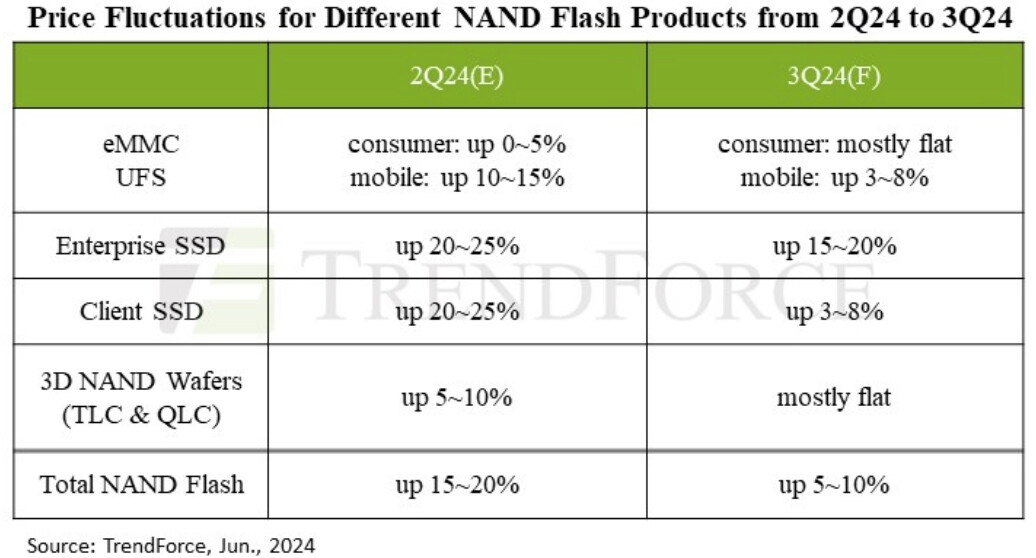

TrendForce reports that while the enterprise sector continues to invest in server infrastructure—especially with the rising adoption of AI driving demand for enterprise SSDs—the consumer electronics market remains lackluster. This, combined with NAND suppliers aggressively ramping up production in the second half of the year, is expected to push the NAND Flash sufficiency ratio up to 2.3% in the third quarter, curbing the blended price hike to a modest 5-10%.

This year, NAND Flash prices saw a robust rebound as manufacturers kept production in check during the first half, helping them regain profitability. However, with a noticeable ramp-up in production and sluggish retail demand, wafer spot prices have dropped significantly. Some wafer prices are now over 20% below contract prices, casting doubts on the sustainability of future price hikes. For client SSDs, even though notebook sales are entering the traditional peak season, customer stocking behavior remains conservative. The prices of PC end products have yet to fully absorb the price hikes from last year, and procurement volumes haven't shown significant growth in the second half. As suppliers upgrade PC client SSD processes to 2XX layers, production capacity is climbing, but weak demand continues to suppress price increases. Additionally, the considerable price gap between QLC and TLC products has led more PC buyers to opt for QLC solutions, heightening price competition. Consequently, the price increase for PC client SSDs in Q3 is expected to be a restrained 3-8%.

For client SSDs, even though notebook sales are entering the traditional peak season, customer stocking behavior remains conservative. The prices of PC end products have yet to fully absorb the price hikes from last year, and procurement volumes haven't shown significant growth in the second half. As suppliers upgrade PC client SSD processes to 2XX layers, production capacity is climbing, but weak demand continues to suppress price increases. Additionally, the considerable price gap between QLC and TLC products has led more PC buyers to opt for QLC solutions, heightening price competition. Consequently, the price increase for PC client SSDs in Q3 is expected to be a restrained 3-8%.

On the enterprise front, the expansion of AI server deployments is driving significant investments in IT infrastructure, with server OEM orders rising sharply in Q3. Despite conservative orders from smartphones and notebooks, the NAND Flash market is becoming more balanced. High-capacity QLC Enterprise SSDs are mainly supplied by two dominant module makers, while others are fiercely competing for enterprise SSD orders to optimize their capacity utilization in the latter half of the year. As a result, the price increase for enterprise SSDs in Q3 is expected to be a substantial 15-20%.

For eMMC, the third quarter lacks significant demand drivers, but module makers are determined to push for higher prices. This determination is expected to result in minimal price increases, with contract prices remaining roughly flat.

In the UFS segment, ample inventory levels and slow depletion by smartphone OEMs, along with increased supply options from module makers, are creating more choice for buyers. As module makers aim for significant price hikes in Q3, resistance is expected. Given ample buyer inventories and weak market demand, suppliers might need to compromise, with Q3 UFS contract prices expected to rise by only 3-8%.

Source:

TrendForce

This year, NAND Flash prices saw a robust rebound as manufacturers kept production in check during the first half, helping them regain profitability. However, with a noticeable ramp-up in production and sluggish retail demand, wafer spot prices have dropped significantly. Some wafer prices are now over 20% below contract prices, casting doubts on the sustainability of future price hikes.

On the enterprise front, the expansion of AI server deployments is driving significant investments in IT infrastructure, with server OEM orders rising sharply in Q3. Despite conservative orders from smartphones and notebooks, the NAND Flash market is becoming more balanced. High-capacity QLC Enterprise SSDs are mainly supplied by two dominant module makers, while others are fiercely competing for enterprise SSD orders to optimize their capacity utilization in the latter half of the year. As a result, the price increase for enterprise SSDs in Q3 is expected to be a substantial 15-20%.

For eMMC, the third quarter lacks significant demand drivers, but module makers are determined to push for higher prices. This determination is expected to result in minimal price increases, with contract prices remaining roughly flat.

In the UFS segment, ample inventory levels and slow depletion by smartphone OEMs, along with increased supply options from module makers, are creating more choice for buyers. As module makers aim for significant price hikes in Q3, resistance is expected. Given ample buyer inventories and weak market demand, suppliers might need to compromise, with Q3 UFS contract prices expected to rise by only 3-8%.

11 Comments on Q3 Contract Prices of NAND Flash Products Constrained by Increased Production and Lower End-User Demand; Estimated to Rise by 5-10%

Meanwhile they're re-releasing basically the same SSDs with lower and lower durability, more heat output, and the only thing they have to show for it is performance in metrics that don't matter to everyday user!

Just remember... The MoAr you buy... The MoAr... you save!:D

Keep in mind that this is a forecast and an estimate by TrendForce and not a guarantee.

Last time I bought some extra storage, just in case, as prices were supposed to go up, they didn't.

Admittedly, they have been going up a fair bit since last summer, but we're still far from prices two years ago.

But no, it's not per TB.

That leaves us with:

Samsung

Western Digital / Kioxia

Solidigm / SK Hynix

Micron

I guarantee prices will not go down if we go from 4 to 3 NAND companies.

Ferengi Rule of Acquisition #10: GREED is Eternal.

It's hard to expect to price to go down, when whole market is moving toward one giant monopoly with all mergers and buyouts.

It's always hard to predict the future.