Friday, April 14th 2023

Strict Restrictions Imposed by US CHIPS Act Will Lower Willingness of Multinational Suppliers to Invest

TrendForce reports that the US Department of Commerce recently released details regarding its CHIPS and Science Act, which stipulates that beneficiaries of the act will be restricted in their investment activities—for more advanced and mature processes—in China, North Korea, Iran, and Russia for the next ten years. The scope of restrictions in this updated legislation will be far more extensive than the previous export ban, further reducing the willingness of multinational semiconductor companies to invest in China for the next decade.

CHIPS Act will mainly impact TSMC; and as the decoupling of the supply chain continues, VIS and PSMC capture orders rerouted from Chinese foundries

In recent years, the US has banned semiconductor exports and passed the CHIPS Act, all to ensure supply chains decoupling from China. Initially, bans on exports were primarily focused on non-planar transistor architecture (16/14 nm and more advanced processes). However, Japan and the Netherlands have also announced that they intend to join the sanctions, which means key DUV immersion systems, used for producing both sub-16 nm and 40/28 nm mature processes, are likely to be included within the scope of the ban as well. These developments, in conjunction with the CHIPS Act, mean that the expansion of both Chinese foundries and multinational foundries in China will be suppressed to varying degrees—regardless of whether they are advanced or mature processes.

TrendForce points out that since 1H23, there is a trend occurring where IC design companies are shifting existing and new orders to Taiwanese foundries under pressure from clients as well as their own need to minimize risks. Tier-2 and -3 companies such as VIS and PSMC, which mainly focus on mature processes, have benefited greatly. TrendForce believes that this shift in orders will undoubtedly ensure major recovery for foundries currently impacted by inventory adjustment and low capacity utilization rates, especially from 2H23 until 2024.

TrendForce points out that since 1H23, there is a trend occurring where IC design companies are shifting existing and new orders to Taiwanese foundries under pressure from clients as well as their own need to minimize risks. Tier-2 and -3 companies such as VIS and PSMC, which mainly focus on mature processes, have benefited greatly. TrendForce believes that this shift in orders will undoubtedly ensure major recovery for foundries currently impacted by inventory adjustment and low capacity utilization rates, especially from 2H23 until 2024.

TrendForce points that TSMC has been the most affected by this updated legislation, mostly due to their plans to expand into both China and the U.S. TSCM's current expansion into China, which began in 2022, has been focused on 28 nm processes at Fab 16. The company has been continuously moving expansion-related equipment into China, and in October 2022, it obtained a one-year import permit. The expansion is scheduled to be completed by mid-2023. However, based on the new CHIPS Act, TSMC's further expansions for 16/12 nm and 28/22 nm processes at Fab 16 are limited for the next decade upon receiving the US subsidies. Furthermore, 85% of the output must meet local market demand in China. US export regulations require multinational foundries to apply for equipment import permits, which will reduce TSMC's willingness to continue investing in China.

Plans to expand memory production will focus on South Korea and the US, and China's share of global DRAM capacity will decline YoY

The new CHIPS Act mainly applies to processes more advanced than 18 nm, which is equivalent to 1Xnm for major suppliers. However, mainstream DRAM processes have already been upgraded to above 1Znm, and customers are gradually transitioning under encouragement from suppliers; only a small portion of consumer DRAM products continue to remain below 1Xnm. However, consumer DRAM products only account for 8% of total capacity. SK hynix is the only major supplier to have a fab in Wuxi, China, but factors such as oversupply and geopolitics have caused DRAM output at the Wuxi fab to drop four percentage points from 48% to 44%, and their new fab is set to be located in South Korea. Meanwhile, Samsung and Micron have no DRAM capacity in China and their plans for future expansion will focus on South Korea and the US, respectively. TrendForce estimates, based on the plans of these three suppliers, that South Korea's share of global DRAM capacity will continue to rise while China's will decline YoY, dropping from 14% to 12% by 2025.

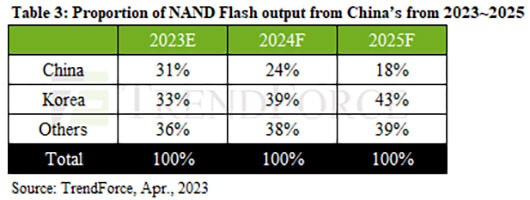

When it comes to the supply of NAND Flash, the US has stated that restrictions on expansion mainly apply to processes with fewer than 128 layers. Samsung's Xi'an fab continues to focus on 128-layer processes and accounts for approximately 17% of global NAND Flash capacity; the Intel fab in Dalian, which was acquired by SK hynix, accounts for 9% of global NAND Flash capacity. However, Samsung and SK Hynix are unlikely to expand their old production lines as 128-layer products will clearly be unable to compete with more advanced ones. The plans involving upgrading process technology and raising production capacity at manufacturing operations in China will be severely limited. All in all, China's share of global NAND Flash capacity is expected to drop from 31% to 18% by 2025.

Demand for DRAM and NAND Flash are in the same boat; many US companies have begun restricting production regions for memory and storage products or are requiring foundries to move their production facilities out of China to avoid geopolitical conflicts. TrendForce predicts the formation of two distinctive production regions: Chinese factories that primarily focus on meeting domestic demand, and factories outside China that will serve other markets.

Source:

TrendForce

CHIPS Act will mainly impact TSMC; and as the decoupling of the supply chain continues, VIS and PSMC capture orders rerouted from Chinese foundries

In recent years, the US has banned semiconductor exports and passed the CHIPS Act, all to ensure supply chains decoupling from China. Initially, bans on exports were primarily focused on non-planar transistor architecture (16/14 nm and more advanced processes). However, Japan and the Netherlands have also announced that they intend to join the sanctions, which means key DUV immersion systems, used for producing both sub-16 nm and 40/28 nm mature processes, are likely to be included within the scope of the ban as well. These developments, in conjunction with the CHIPS Act, mean that the expansion of both Chinese foundries and multinational foundries in China will be suppressed to varying degrees—regardless of whether they are advanced or mature processes.

TrendForce points that TSMC has been the most affected by this updated legislation, mostly due to their plans to expand into both China and the U.S. TSCM's current expansion into China, which began in 2022, has been focused on 28 nm processes at Fab 16. The company has been continuously moving expansion-related equipment into China, and in October 2022, it obtained a one-year import permit. The expansion is scheduled to be completed by mid-2023. However, based on the new CHIPS Act, TSMC's further expansions for 16/12 nm and 28/22 nm processes at Fab 16 are limited for the next decade upon receiving the US subsidies. Furthermore, 85% of the output must meet local market demand in China. US export regulations require multinational foundries to apply for equipment import permits, which will reduce TSMC's willingness to continue investing in China.

Plans to expand memory production will focus on South Korea and the US, and China's share of global DRAM capacity will decline YoY

The new CHIPS Act mainly applies to processes more advanced than 18 nm, which is equivalent to 1Xnm for major suppliers. However, mainstream DRAM processes have already been upgraded to above 1Znm, and customers are gradually transitioning under encouragement from suppliers; only a small portion of consumer DRAM products continue to remain below 1Xnm. However, consumer DRAM products only account for 8% of total capacity. SK hynix is the only major supplier to have a fab in Wuxi, China, but factors such as oversupply and geopolitics have caused DRAM output at the Wuxi fab to drop four percentage points from 48% to 44%, and their new fab is set to be located in South Korea. Meanwhile, Samsung and Micron have no DRAM capacity in China and their plans for future expansion will focus on South Korea and the US, respectively. TrendForce estimates, based on the plans of these three suppliers, that South Korea's share of global DRAM capacity will continue to rise while China's will decline YoY, dropping from 14% to 12% by 2025.

When it comes to the supply of NAND Flash, the US has stated that restrictions on expansion mainly apply to processes with fewer than 128 layers. Samsung's Xi'an fab continues to focus on 128-layer processes and accounts for approximately 17% of global NAND Flash capacity; the Intel fab in Dalian, which was acquired by SK hynix, accounts for 9% of global NAND Flash capacity. However, Samsung and SK Hynix are unlikely to expand their old production lines as 128-layer products will clearly be unable to compete with more advanced ones. The plans involving upgrading process technology and raising production capacity at manufacturing operations in China will be severely limited. All in all, China's share of global NAND Flash capacity is expected to drop from 31% to 18% by 2025.

Demand for DRAM and NAND Flash are in the same boat; many US companies have begun restricting production regions for memory and storage products or are requiring foundries to move their production facilities out of China to avoid geopolitical conflicts. TrendForce predicts the formation of two distinctive production regions: Chinese factories that primarily focus on meeting domestic demand, and factories outside China that will serve other markets.

10 Comments on Strict Restrictions Imposed by US CHIPS Act Will Lower Willingness of Multinational Suppliers to Invest

An CHIPS act itself violating WTO rules.

Yeah China has already cornered the materials market so not surprising the US gov doesn't know this

Places where mining isn't as or regulated at all China is already there

US is way to restrictive to mine much of anything and if they could it would be a long long process to get around protesters/ EPA red tape that would find a rare bug to protect.

Symbolic handouts.

www.forbes.com/sites/douglasbulloch/2016/10/12/protectionism-may-be-rising-around-the-world-but-in-china-it-never-went-away/#5dc3f5df73da

From Forbes,

Title: Protectionism May Be Rising Around The World, But In China It Never Went Away

Year Date: 2016

Promises unkept?

Since joining the WTO in 2001, China has repeatedly insisted that it will live up to those undertakings made on entry. In particular, the use of currency manipulation has been identified by the US as a breech of the commitment to end price controls for the purposes of protecting domestic industries. This became a major political issue from 2005 onwards, and has only recently subsided because it is assumed that the RMB is slightly overvalued on the market. Nevertheless, for years it was deliberate policy for the PBoC to accumulate US Dollars and suppress the exchange rate for the RMB, resulting in exactly the price distortions China had committed to eliminate in 2001, and fuelling an enormous trade surplus with the US, which persists and expands to this day.

Furthermore TRIPS implementation has been given some effect on paper, but has made little progress when it comes to 'enforcement.' This is (according to the WTO) as recently as February 2015, fully 14 years after TRIPS was supposed to be already in effect. The US Trade Representative produces an annual report to Congress on China's WTO compliance which leaves little room to conclude they have so far lived up to their accession commitments. The most recent several-hundred-page document - produced in December 2015 - recites a long list of small measures, committees established, announcements made and new administrative complications faced, all continuing disputes over an agreement theoretically in effect since 2001.

Although, therefore, protectionism is rising around the world, it is also true to say that existing practices of protectionism have not fallen in the way that they should have since China's accession to the WTO in 2001. Because of this lack of progress in easing trade, the extended period of currency manipulation, the lack of observance of TRIPS and the sheer administrative resistance exporters face when trying to get their products into China, we now face of world of highly unbalanced trade, and rising mistrust. And it is this that is leading to rising protectionism; the simple fact that it never went away.China has a "Negative List of Market Access Restricted: Sector-wise items" which is known as CCP's protectionist list. Read www.china-briefing.com/news/china-2020-negative-list-market-access/

Category 2: Mining

5. Investment in rare earth, radioactive minerals, tungsten exploration, mining, and mineral processing is prohibited.

Category 3: Manufacturing

6. Chinese companies must have a controlling stake in the publishing & printing industry.

7. It is prohibited to invest in the application of traditional Chinese medicinal decoction pieces, such as steaming, frying, roasting and calcining, etc. It is prohibited to invest in the production of traditional Chinese medicine confidential prescription products.

8. The Chinese share of vehicle manufacturing companies should not be less not than 50%, except for the special and new energy vehicles, commercial vehicles. (In 2022 the restriction of foreign share ratio in passenger car manufacturing and the restriction of the same foreign company can establish two or fewer joint ventures in China to produce similar vehicle products will be removed.)

9. It is prohibited to invest in satellite TV broadcast ground receiving facilities and key parts production.

Category 4: Electricity, heat, gas and water production and supply

10. Chinese companies must have a controlling stake in the construction and operation of nuclear power plants.

Category 5: Wholesale and retail

11. It is prohibited to invest in the wholesale and retail of tobacco leaves, cigarettes, re-baked tobacco leaves, and other tobacco products.

Category 6: Transport, warehousing, and postal services

12. It is required that Chinese companies have a controlling stake in domestic water transport.

13. Chinese public air transport enterprises shall be controlled by the Chinese side and if the proportion of investment by a foreign investor and its affiliated enterprises shall not exceed 25%, the legal representative shall be a Chinese citizen. The legal representative of General airlines must be a Chinese citizen, of which agriculture, forestry, and fisheries airlines shall be limited to joint ventures and other general-purpose airlines shall be limited to Chinese holdings.

14. Chinese companies must have a controlling stake in the construction and operation of civil airports.

15. It is prohibited to invest in the domestic express services provided by postal companies (and to operate postal services) and letters.

--------------

Foreigners are not allowed in China's mining sector.

web.archive.org/web/20140203202228/https://graphitepublications.com/will-chinas-outrageous-rare-earth-monopoly-persist

China's rare earth near-monopoly was built on SOE (State-Owned Enterprise) which drove private competitors from the market. Rare earth is important for the electronics component production logistics chain.

From Graphite Publications article from 2010.

Title: Will chinas Outrageous Rare Earth Monopoly Persist

Year Date: 2010.

Heavy importers of these REEs such as the U.S., Germany, and Japan believe these rationales disguise China’s true exploitative motive: to force foreign factories to move to China to keep their costs low and their supply high.

www.wsj.com/articles/SB10001424052748703321004575427050544485366

From WSJ

Date: Aug. 15, 2010

Title: After securing Rare-Earth monopoly, China Dangles Rare-Earth Resources to Lure Investment

Reciprocal trade policy is a simple concept to understand. Protectionist CPC's China couldn't handle another protectionist neo-China (USA). LOLAround Y2022, the Australian federal government intervened in the Australian rare earth mining sector with cheap state loans. This is in response to China's many decades of state support for its rare earth ming sector.Feelings are useless without firepower.